USDT: A peer-to-peer electronic cash system

USDT has taken on the business of cryptocurrency payments and has supported a significant part of the market.

USDT has taken on the business of cryptocurrency payments and has supported a significant part of the market.0x29 0x66/Article, published on May 20, 2020, by BlockBeats.

In 2008, a paper titled "Bitcoin: A Peer-to-Peer Electronic Cash System" emerged, and for the next 12 years, Bitcoin carried the hope of this new payment method, but unfortunately, it failed. Today, we have found its new successor—USDT. Various signs indicate that USDT is the new way of payment, and USDT is the true peer-to-peer electronic cash system.

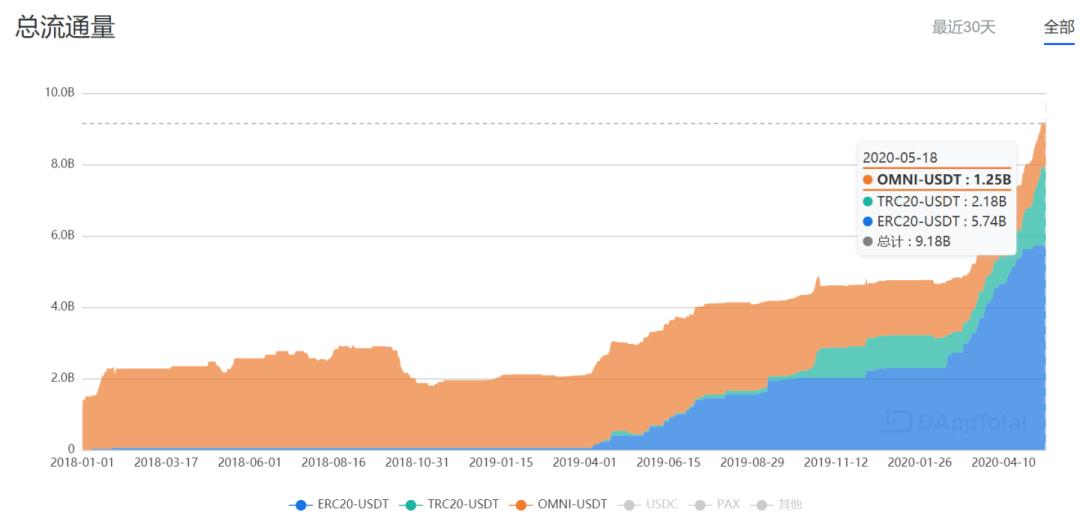

In two months, USDT has issued nearly 5 billion USD, with a market capitalization exceeding 9 billion USD.

At the same time, the market capitalization of stablecoins has surpassed 10 billion USD. CoinX has issued USDS, entering the stablecoin market; PayPal Financial plans to create a stablecoin; Sun Yuchen remained indifferent during the DeFi boom last year, but this year, in the context of the crazy issuance of TRC20-USDT, he still launched the USDJ stablecoin.

However, behind this, BTC has not broken new highs. Apart from the extreme market conditions on March 12 caused by the global environment, Bitcoin has been hovering around 10,000 USD since 2018, and industry investors have not increased visibly as they did in 2017. Since the amount of funds and audience has not increased, why has the stablecoin been issued so much out of thin air?

To explore the deeper reasons behind this, BlockBeats summarized the patterns of USDT issuance and interviewed several people related to the stablecoin field, arriving at a shocking conclusion: stablecoins can exist completely independent of the cryptocurrency industry, and in the near future, stablecoins will continue to rise, even surpassing Bitcoin.

More extremely, even if Bitcoin goes to zero, stablecoins led by USDT will still exist, inheriting Satoshi Nakamoto's "legacy" and becoming that peer-to-peer electronic cash system.

The future USDT market will be larger than the combined market capitalization of all cryptocurrencies today.

Phenomenon

From May 1 to 14, the macro-control hand of Tether made a significant move, minting another 1.36 billion USDT, worth 1.36 billion USD. In less than two months, Tether has minted nearly 40 times.

How fast is this speed? You can feel it by looking at these two data from CMC: the current total market capitalization of USDT exceeds 9 billion USD, but in 2017, this number was only about 100 million USD. In other words, Tether can issue the equivalent of three times the market capitalization of 2017 within 24 hours, achieving a 90-fold leap in market capitalization in just three years.

This is no longer news; the industry has already discussed it. The consensus conclusion is roughly: stablecoins are the biggest winners, and stablecoins represented by USDT have a trend of going beyond their original applications.

As Bitcoin prices slowly rise, coupled with negative oil prices, DeFi hacks, and other historical emergencies, people have become accustomed to the issuance of stablecoins, but stablecoins have not slowed down. Not only USDT, but also PAX, HUSD, USDC, and other stablecoins are being issued.

Our doubts are growing stronger: where is all this money going? BlockBeats, with great curiosity, seeks to validate this bold hypothesis: stablecoins have completely transcended Bitcoin and become the largest application of cryptocurrency.

First, let's look at the phenomena, which are also clues. We have noticed the following three phenomena:

First, USDT has frequently issued in the past three months, characterized by a high frequency of issuance and huge single issuance amounts, with an average single issuance of nearly 100 million USD. Throughout April, Tether issued a total of 24 times, with ERC20 USDT alone issuing 1.26 billion units. By May, Tether shifted its focus to Tron, issuing over 1.1 billion USDT. What does this mean? It means that Tether is "printing" money equivalent to a unicorn company every month.

Screenshot source: Dapptotal

Screenshot source: Dapptotal

If we extend the time dimension, this trend of issuance began to show signs as early as February. From the frequency perspective, after the market crash on March 12, Tether clearly accelerated its issuance speed; initially, Tether was relatively restrained, starting with an issuance of 60 million, and later simply changed to issuing 120 million or even 180 million at a time.

Next, let's look at the flow. An abnormal point is that the flow of USDT is overly concentrated on a few trading platforms.

Previously, the security company Beijing Chain Security tracked the USDT issued in March, where 2,206 "clear" receiving parties were identified as transfer operations of trading platforms. It was ultimately found that over 80% of these issued USDT flowed into Binance and Huobi.

For investors who have been immersed in the cryptocurrency circle for many years, the issuance of USDT is accompanied by the rise in Bitcoin prices. Previously, when news of USDT issuance came out, it was generally regarded as a signal to pump the market. However, now, the ratio of USDT market capitalization to Bitcoin market capitalization has reached a historical high.

Next, is it only USDT that is being issued? No. USDC, PAX, and other stablecoins are also being issued, and the overall market capitalization of stablecoins has reached 10 billion USD.

This is not all; new teams are also joining the stablecoin battlefield.

CoinX announced the launch of the USDS stablecoin, which is a dollar stablecoin based on BTC acceptance as its value foundation, officially entering the stablecoin field. One of the largest lending companies in the industry, PayPal Financial, also revealed plans to enter the stablecoin market, although the conditions are not yet ready.

Sun Yuchen's Tron suddenly increased the issuance of TRC20-USDT this year, with a market capitalization already exceeding Tron. This is not enough; Sun Yuchen suddenly entered the DeFi field, mimicking MakerDAO, and launched the USDJ stablecoin.

Finally, how much enthusiasm is there currently in the cryptocurrency secondary market? Let's first look at how many new coins there are now. New coins like MASS, Solana, HIVE, etc., seem to be few and far between, far from the glamorous initial financing period of trading platform tokens last year.

What about contract trading volume and open interest? Compared to February of this year, it is far from the exciting and surprising scene of February. Therefore, the densely explosive issuance of USDT, along with the issuance of USDC and PAX, new players entering the stablecoin race, and those planning to enter the stablecoin battlefield, who are using this newly printed money?

Or to clarify the question further: are these issued stablecoins all used for asset transfer? With this question in mind, we spoke to some participants.

Huobi seems to act as a general distributor; Chinese users are the main ones.

"80% of stablecoin trading volume is on Huobi." As someone who interacts with institutional traders and also connects with Tether's OTC merchants, Bai Xiao can directly perceive the significant changes brought by USDT issuance.

In March of this year, his trading volume unusually reached the tens of millions level. With a fee of 5 cents per USDT, his daily income could reach five figures. Similarly, another OTC merchant, Lin Fan, has had a similar experience: "Huobi's OTC trading volume has increased by at least 30%."

Bai Xiao told BlockBeats that the process of issued stablecoins flowing into the market generally follows this path: OTC merchants receive or assess the market demand for USDT, connect with one of the few Tether issuing agents globally, obtain first-hand USDT, deposit it into trading platforms or other wallet addresses, and then sell it to institutions or individuals through various means, ultimately flowing into the market.

"Huobi's role is somewhat like a general distributor; many people buy from Huobi and then sell on Binance and OKEx." It is understood that the fiat trading areas of trading platforms are generally divided into two categories.

One is outsourced to agents, where the platform only provides a display window. Due to the different usage habits of domestic and foreign users, the choice of payment partners also varies. For example, credit card transactions may choose Simlex, while large USD transactions may choose American financial trust company Prime Trust, etc.; the other category is self-operated by the platform, where the platform recruits OTC merchants to settle in.

According to qkl123's USDT OTC premium data, from early February to early May, USDT has been at a positive premium, especially in mid-March this year, reaching a historical high of nearly 15%.

"At that time, USDT was really in short supply." Bai Xiao recalled that Tether had just started to increase the speed of USDT issuance, but unexpectedly, after the huge market fluctuations, the market still experienced a situation where USDT was in short supply. Huobi's leverage rate could reach a daily rate of 0.1%, "which is extraordinarily high."

PayPal Financial CEO Yang Zhou also expressed a similar view, "There is a lack of fiat currency supply in the market." In Yang Zhou's view, Bitcoin has fallen too quickly, and there is not enough fiat currency supply to support it.

It cannot be denied that a portion of the newly issued USDT has entered the market. After all, from the USDT balance on trading platforms, the daily balance is increasing, and users may hold USDT waiting for buying opportunities; or contracts using USDT as collateral are starting to become a trend, all of which may indicate the demand flow for stablecoins.

However, this does not fully explain our biggest question: does the market really need so much money? Has this money really entered the cryptocurrency secondary market?

With each issuance, the USDT shipment volume increases.

Lin Fan mentioned an interesting phenomenon, "Since March, with each USDT issuance, the number of orders I receive has increased significantly, by about 50%."

Lin Fan's clients are generally repeat customers, with long-term cooperation and mutual WeChat contacts. When they need to trade, they contact each other on WeChat. However, since March, some of the orders Lin Fan has received are not from old clients. "My average daily trading volume is 1.6 million USDT, and since March, I clearly remember that after each issuance, the USDT orders surged, increasing by about 600,000 to 800,000, and these clients are occasional."

With each issuance, someone sells USDT and exchanges it for RMB. This is clearly not a normal phenomenon: a portion of USDT has not flowed into the secondary market but has other applications.

This is not the first time stablecoins have gone beyond their original scope; the applications of stablecoins represented by USDT have quietly begun since 2017.

Yujun, the founder of the cross-border payment platform Qbitpay, told us that in the fields of overseas e-commerce and overseas gaming, stablecoins have already been very mature for settlement. Recently, Qbit's trading volume has been increasing by 50% each month.

Moreover, the path of using stablecoins to transfer assets has long been established.

According to Lin Fu, a person in the stablecoin field, the issued USDT is not meant to buy BTC and will not push up coin prices; much of the USDT has flowed outside the circle. "USDT is a collection of gray industries."

Some online gambling platforms have already used USDT.

According to his understanding, online gambling, live streaming rewards, and other internet businesses, even underground banks he has come into contact with, have accepted USDT as an important payment method. We casually opened a gambling website he sent, and indeed found that it supports USDT and various stablecoin deposits. It is well-known that the world's largest adult website, Pornhub, also supports USDT.

Compared to PayPal and credit cards, the former has a poor user experience, and the latter is prone to fraud, making USDT's "advantages" more apparent: there are no geographical restrictions, and it is not within the scope of regulatory control.

These external use cases are becoming a broader application of USDT beyond just trading cryptocurrencies.

"The consensus in the gray industry is very strong; this year, the stock of USDT is expected to exceed 20 billion USD." Lin Fu said that with the current market capitalization of USDT at 7 billion USD, according to this estimate, it could at least double * (Note from BlockBeats: The interview was conducted in early May, and as USDT's total market capitalization soared to 9 billion, Lin Fu has updated his estimate of the stablecoin scale to 50 billion USD, "previously underestimated").*

A bold hypothesis

"A Peer-to-Peer Electronic Cash System," is the title of Bitcoin's white paper. Bitcoin's original goal was to be a payment tool, but now, Bitcoin has not upheld this domain of payment. The attributes of Bitcoin have evolved from digital gold into a commodity, a commodity that speculators view similarly to oil and gold. Would you use oil to buy things? Certainly not.

On the other hand, stablecoins represented by USDT have taken on the business of cryptocurrency payments, holding up a domain.

The global liquidity crisis in various asset secondary markets triggered by the pandemic has made everyone eager for cash. During this period, China's secondary market was almost the best-performing globally. The model of unlimited dollar printing may have raised concerns for many about the U.S. sovereign credit currency system. Meanwhile, China, which has controlled the pandemic most effectively, seems to be a good landing point, with the future of the RMB appearing more promising than the USD.

In this historically significant issuance, a large portion of the new currency may be used for asset transfer, converting foreign assets into USD, then exchanging USD for USDT, and finally converting it into RMB on trading platforms.

Some believe that USDT will crash because it is not 100% pegged to the USD. In fact, whether it is 100% pegged to the USD is no longer important; it once faced a crash but survived. The 9 billion USD market capitalization clearly indicates one thing: it has achieved what Bitcoin cannot. Now, the largest application that has transcended the blockchain industry is not Bitcoin, but stablecoins. Bitcoin wants to be a payment method; it is no longer possible; it is just a commodity. USDT is now recognized as the peer-to-peer electronic cash system.

The story of stablecoins is far from over.

For the protection of the interviewees, the names Bai Xiao, Lin Fan, and Lin Fu in the text are pseudonyms.

Risk warning

Risk warning Risk warning

Risk warning