How Lending Agreements Accelerate Settlement Speed and Improve Capital Efficiency

Stable pool, debt warehouse transfer, recovery mode if achieving more efficient clearing.

Stable pool, debt warehouse transfer, recovery mode if achieving more efficient clearing.This article was published on February 23 on Liquity's official medium by Robert Lauko. Chain Catcher has translated this article and made edits that do not affect the original meaning.

On February 23, mainstream currencies like Bitcoin and Ethereum experienced significant corrections, and the liquidation amounts of various DeFi lending protocols also hit a historical high. According to DeBank data, the liquidation volume of lending protocols on Ethereum reached $131 million in the past 24 hours, surpassing last November's record of $93.3 million. Robert Lauko, a former Dfinity researcher and the current founder of the Liquity protocol, wrote an article discussing how lending protocols should accelerate liquidation speeds to improve capital efficiency.

Situation Analysis

One of the fundamental tasks of DeFi lending protocols is to liquidate positions that fall below the minimum collateralization ratio. The design of this ratio should ensure that even the proceeds from forced liquidation of collateral can cover the outstanding debt.

Under normal circumstances, borrowers are willing to repay automatically, but if they do not repay, the system must enforce liquidation. From the user's perspective, a lower collateralization ratio can achieve higher capital utilization, so some lending protocols choose to enhance their attractiveness by lowering collateral requirements.

For example, if the liquidation ratio is set at 150%, a risk-averse borrower maintains a collateralization ratio of 300%, meaning they will not be liquidated even if the price of the collateral drops by 50%. If the liquidation ratio is set at 110%, only a collateralization ratio of 220% needs to be maintained. With a difference of 40% in the minimum collateralization ratio, the amount of collateral can be reduced by 80%. Sounds good, right?

So why do some lending protocols set collateral requirements as high as 130%, 150%, 200%, or even 750%?

Because, under the same conditions, a lower liquidation threshold often means higher systemic risk, as loans may not be fully recoverable. So what other factors determine risk?

Related to Liquidation Speed

The longer it takes to liquidate collateral, the greater the risk that the collateral will further depreciate before the actual debt is settled.

Typically, the steps from determining that a collateral's collateralization ratio is below the minimum requirement to completing the liquidation are as follows:

First, decentralized lending platforms rely on oracle services to provide pricing for the collateral, and the system will also accept multiple sources of information to calculate a more accurate price. To prevent the pricing process from being attacked, the MakerDAO Oracle Security Module (OSM) delays the release of new reference prices by one hour.

Once it is confirmed that the current price of the collateral is below the minimum collateralization ratio, specific participants will call a function to liquidate, and then the system will auction off the collateral, which may involve multiple rounds of bidding. In MakerDAO, such auctions can last for 6 hours or longer.

Alternatively, the collateral can be sold at a certain discount based on the price provided by the oracle. The early MakerDAO, which only supported collateralized ETH, also adopted this mechanism, and currently, Equilibrium, Kava, and Reflexer are still using it.

In any case, determining that a loan's collateral is insufficient to cover its debt takes a non-negligible amount of time, during which the collateral may continue to depreciate. The more frequently price feedback is updated, the shorter the actual liquidation time, which is better.

Therefore, for lending platforms, the more timely the price feedback after determining that a collateral is insufficient to cover its debt, the more efficient the liquidation rate will be, which is beneficial for risk management.

The following chart shows the collateralization ratios of CDPs in the first year of MakerDAO that were liquidated at various ratios.

Volatility of Collateral Prices

Although the depicted chart shows the liquidation situation of ETH-backed positions, most other types of collateral and tokens may be more volatile than Ethereum. For these types of collateral, we can expect a larger portion of liquidations to occur at lower collateralization ratios. On the other hand, if a lending platform uses stablecoins or other low-volatility assets as collateral, a lower margin can provide the same level of security.

While the depicted chart shows only ETH-supported liquidations, the prices of most other collateral types may be more unstable, and for these types of collateral, a larger portion of liquidations can be expected to occur at lower collateralization ratios. Conversely, if a lending platform uses stablecoins or other low-volatility assets as collateral, a lower collateralization ratio can be set.

Comparison of Liquidated Collateral Amounts with Market Liquidity

Finally, the amount of collateral has an impact on the potential price drop relative to the available liquidity in the market. If a large amount of collateral needs to be sold all at once in a market with insufficient liquidity, prices may drop significantly. Interestingly, this situation can be improved by selling collateral slowly, but it will face longer liquidation times and additional external price risks.

English auctions also have a problem in that all bids need to be locked in throughout the auction period, which puts upward pressure on the tokens needed to repay the liquidation debt. Dutch auctions can alleviate this issue, but there are practical limitations to reducing the speed of bidding during the auction process.

Improving Margin Risk from a Systemic Perspective

The above factors are not entirely external and uncontrollable. What can be done to improve this situation through appropriate system design?

Faster Price Supply

First, oracles with higher update frequencies can be used. Instead of collecting and aggregating multiple price sources over a specific period, it may be better to calculate the median price after each update. It may also be worth considering fetching pricing data from decentralized exchanges and liquidity pools like Uniswap and KyberSwap, or having managers provide price feedback and prove its accuracy when liquidation is required. These measures are not without challenges, as is well known currently.

Clearing Process Based on Stable Pools

Another measure targets the liquidation process itself. Existing platforms are based on some form of active liquidation, requiring buyers or bidders to purchase collateral during liquidation, but this is not the only possibility!

We can approach it differently, allowing interested parties to express their intent to acquire liquidated collateral before liquidation occurs. For example, users could deposit the tokens needed to repay debts into a stable pool. Of course, this means that the pricing mechanism must be adjusted, but this is easier than people might think. If people can reasonably expect to receive collateral worth more than what they paid during liquidation, they should have the incentive to participate in the transaction early.

Setting the collateralization ratio slightly above 100%, such as at 110%, provides a natural way to implement this mechanism. If a loan's collateral value drops below the minimum collateralization ratio, the collateral can be directly handed over to the acquirer, allowing the system to use their funds in the stable pool to recover the debt from the borrower. In this way, the surplus collateral or excess collateral becomes the profit for the acquirer or the loss for the borrower, making the concept of "liquidation penalties" used separately in other protocols outdated.

The box on the left shows a loan in good standing, which becomes under-collateralized after the dollar value of the collateral decreases, falling below the liquidation rate (on the right). The dark blue area indicates the surplus collateral and the net gains realized by the stable pool.

This way, holders of stablecoins have the incentive to deposit some of their tokens into the stable pool, expecting to gain from future collateral liquidations.

Deposits into the pool have no lock-up period, so depositors can withdraw their tokens at any time, unless there are liquidatable positions in the system (in which case, under-collateralized positions need to be liquidated first). However, in the case of liquidation, the system will use the required amount of pooled stablecoins to offset the debt of the liquidated position. In return, the collateral associated with the position will also be transferred to the stablecoin pool. This is the liquidation processing method used by Liquity:

Deposits in the stability pool and offsets for under-collateralized positions (also known as Troves).

Depositors maintain a proportional share of the remaining stablecoins and the collateral tokens obtained in the pool based on their initial deposit. Depositors can also redeem their collateral gains along with the remaining stablecoins deposited.

Exiting from Liquity's stability pool.

Why is this mechanism superior to collateral auctions or fixed-price sales?

Tokens in the stable funding pool can be immediately used to offset under-collateralized debt. Since there are no collateral auctions or discounted sales, there is no need to find buyers to take over the collateral, nor will there be price pressure on the collateral.

It is not difficult to see that depositing stablecoins into the stability pool is economically attractive. As long as the surplus collateral returns are positive (at least on average), over the long term, regardless of the size of the pool or how many loans are liquidated, depositors can expect to receive nearly risk-free net gains. However, individual returns are positively correlated with the amount of collateral liquidated and the surplus portion, while decreasing as the number of stablecoins in the pool increases.

So can we expect every holder to put their tokens into the pool? Certainly not. Many stablecoin holders prefer stability and are reluctant to choose the potential economic returns of volatile tokens. However, we can assume that a considerable number of investors or speculators will provide liquidity to the stable pool, and the portion of tokens entering the stable pool will reach economic equilibrium. Liquity will also distribute secondary tokens LQTY to stable pool depositors, further incentivizing participation in the stable pool. At any given point, the amount of stablecoins in the stability pool will ensure the liquidation of the corresponding amount of debt.

But what if the debt needing liquidation exceeds the stablecoins in the pool?

Backup Loan Redistribution Mechanism

If the stable funding pool is insufficient to offset all under-collateralized debt, the system will resort to a second mechanism.

The idea is to redistribute the liquidated positions (including debt and collateral) to still-active positions. This redistribution can be done according to the proportion of collateral of the loans accepted. This means that the debt and collateral of all active borrowers will increase, but since liquidations occur when the collateralization ratio exceeds 100%, the relative increase in collateral is usually higher. Like the stable funding pool, the surplus collateral will allow the loan recipients to gain net returns:

These two charts show loans A, B, C, and D along with their debt and collateral amounts (in dollar value), with loan D being under-collateralized and redistributed to A, B, and C.

On the other hand, the collateralization ratios of the receiving positions deteriorate, but according to the current ratios, this impact is minimal.

These two charts show the changes in individual collateral ratios of loans and the net returns from redistribution (as well as the losses of position D).

Let's look at some data for another example. If a position with a collateralization ratio of 108% accounts for 10% of the total collateral in the system (after deducting a 0.5% gas fee compensation) undergoes redistribution, then each position's collateral will rise by 11.11 (10/9) percentage points, and their liabilities will also increase by 10.34 (=11.11/1.075) percentage points.

A loan with a collateralization ratio of 250% will see its ratio drop to 236.65 ((250%+11.11%)/(100%+10.34%)). The lower the collateralization ratio of the loan recipient, the smaller the impact. Therefore, the probability of a loan being drawn down below the liquidation ratio is very low. Even a loan with a collateralization ratio of only 111% will remain above the critical point, and after redistribution, the collateralization ratio will reach 110.57%.

Collective Guarantee and Collateral Enhancement Effect

Due to this redistribution, loans are ultimately guaranteed by the total available collateral. That is, as long as the total collateralization ratio of all loans remains above 100%, the protocol can cover all debts.

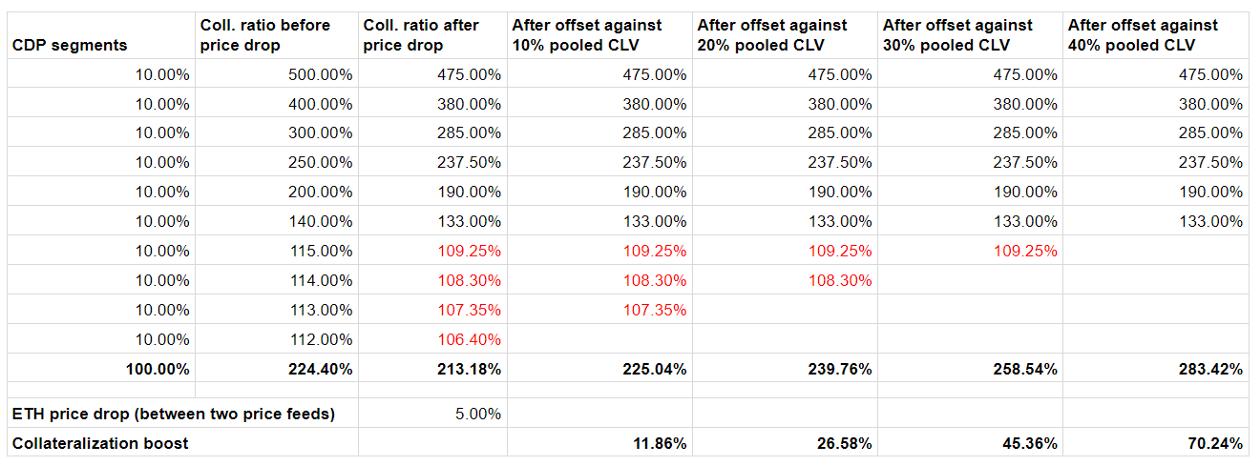

However, in most cases, under-collateralized loans do not need to be redistributed because they can be fully offset by the stable funding pool. In fact, before the redistribution mechanism is activated, the pool can absorb a certain proportion of defaults, providing the system with collateral backing. The absorbed positions are those with the lowest collateralization ratios. This means that the effective collateralization ratio of the total loan amount is higher than the total collateral divided by the total debt. The following table illustrates this effect:

Final Thoughts

As we have seen, new liquidation mechanisms, such as offsetting loans with stable funding pools and redistributing remaining loans to other positions, are effective ways to ensure debt safety. Due to the direct effects of these mechanisms, and the absence of unnecessary side effects like price pressure or time loss, liquidation ratios can be significantly reduced.

By increasing the collateralization ratio, not only will capital efficiency improve, making it more attractive overall, but if the borrowed tokens are reinvested to purchase more crypto assets, the protocol can also achieve higher leverage.

Risk warning

Risk warning Risk warning

Risk warning