Two Thought Experiments for Evaluating Automated Stablecoins

Author: Vitalik Buterin

Original Title: 《Two thought experiments to evaluate automated stablecoins》

Publication Date: May 25, 2022

Special thanks to Dan Robinson, Hayden Adams, and Dankrad Feist for their feedback and review.

The recent collapse of LUNA has led to losses of billions of dollars and sparked a storm of criticism against the category of "algorithmic stablecoins," with many considering them a "fundamentally flawed product." There is a strong push for increased scrutiny of DeFi financial mechanisms, especially those algorithmic stablecoin mechanisms that work very hard to optimize "capital efficiency." There is also a growing recognition that past performance does not guarantee future returns (and does not even guarantee that there won't be a complete collapse in the future). However, the market sentiment is very misguided in that it paints all decentralized crypto algorithmic stablecoins with the same brush, condemning all algorithmic stablecoin projects.

While many algorithmic stablecoin designs are fundamentally flawed and destined to fail, there are also many stablecoins that can theoretically survive, albeit with high risks, and there are many stablecoins that are theoretically very robust and have withstood extreme tests of market conditions in practice. Therefore, what we need is not stablecoin advocacy or stablecoin doomsaying, but a return to principle-based thinking. So, what good principles can be used to evaluate whether a specific algorithmic stablecoin is truly stable? For me, I start with two thought experiments to test stablecoins.

What is an algorithmic stablecoin?

For the purposes of this article, an algorithmic stablecoin is a system with the following attributes:

It issues a stablecoin that attempts to peg to a specific price index. Typically, the target is $1, but there are other options. There are some target mechanisms that continuously push the price back towards the stable index ($1) when the price deviates in either direction. This makes ETH and BTC not stablecoins.

The target mechanism is completely decentralized, and the protocol does not rely on any specific trusted participants. In particular, it must not rely on asset custodians, which makes USDT and USDC not stablecoins.

In practice, (2) means that the target mechanism must be some kind of smart contract managing a reserve of crypto assets, using these crypto assets to support the price when it falls.

How does Terra work?

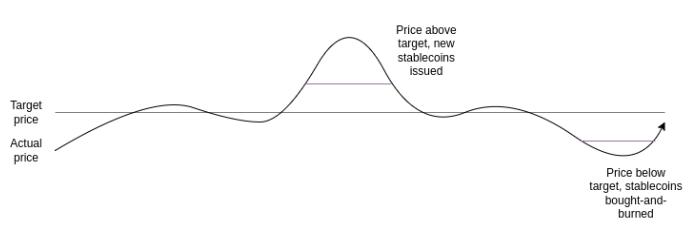

Terra-style stablecoins (roughly similar to minting Stake, although many implementation details differ) operate by having two currencies, which we call the stablecoin and the volatile coin (in Terra, UST is the stablecoin, and LUNA is the volatile coin). The stablecoin uses a simple mechanism to maintain stability:

- If the price of the stablecoin exceeds the target price, the system auctions new stablecoins (and uses the proceeds to burn LUNA) until the stablecoin price returns to the target price.

- If the price of the stablecoin falls below the target price, the system buys back and burns stablecoins (issuing new LUNA to fund the burn) until the stablecoin price returns to the target price.

What is the current price of the volatile coin (LUNA)? The value of LUNA may be purely speculative, based on the assumption that future demand for the stablecoin will increase (which would require burning volatile coins to issue UST). Alternatively, the value could come from fees: trading fees on stablecoin/LUNA exchanges, or holding fees charged to stablecoin holders annually, or both. But in all cases, the price of the volatile coin comes from expectations of future activity in the LUNA ecosystem.

How does RAI operate?

In this article, I focus on RAI rather than DAI because RAI better represents the pure (decentralized) "ideal type" of algorithmic stablecoin, supported solely by ETH. DAI is a hybrid system supported by both centralized and decentralized collateral, which is a reasonable choice for their product, but it does complicate the analysis.

In RAI, there are primarily two types of participants (there are also holders of FLX, a speculative token, but their role is less significant):

There are two main reasons to become a RAI lender:

Long on ETH: If you deposit 10 ETH in the above example and withdraw 500 RAI, your final position is worth 500 RAI, but you have an exposure of 10 ETH, so for every 1% change in the price of ETH, it will go up/down by 2%.

Arbitrage: If you find an investment priced in fiat that is rising faster than RAI, you can borrow RAI, invest the funds in that investment, and profit from the difference.

If the price of ETH falls and the vault no longer has enough collateral (meaning that RAI debt now exceeds two-thirds of the value of the stored ETH), a liquidation event occurs. The vault is auctioned off to others to purchase by providing more collateral.

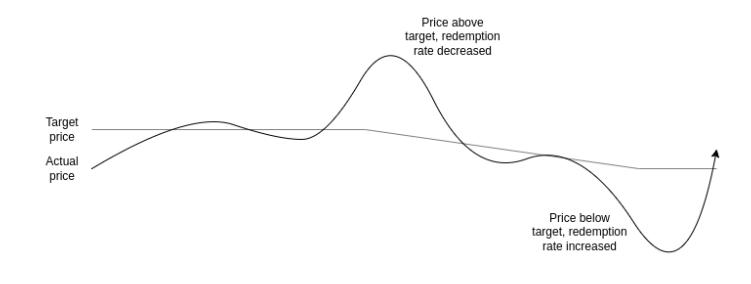

Another key mechanism to understand is the redemption rate adjustment. In RAI, the target is not a fixed amount of dollars; rather, it moves up or down, and the rate at which it moves up or down is adjusted based on market conditions:

If the price of RAI is above the target, the redemption rate decreases, reducing the incentive to hold RAI and increasing the incentive to hold negative RAI as a lender. This pulls the price down.

If the price of RAI is below the target, the redemption rate increases, increasing the incentive to hold RAI and reducing the incentive to hold negative RAI as a lender, which can push the price up.

Thought Experiment 1: Can a stablecoin theoretically safely reduce to "zero users"?

In the non-crypto real world, nothing is eternal. Companies always go out of business, either because they failed to find enough users from the start, because demand for their product that was once strong no longer exists, or because they are replaced by a stronger competitor. Sometimes, partial collapses occur, falling from mainstream status to niche status (like MySpace). Such things must happen to make room for new products. But in the non-crypto world, when a product shuts down or declines, users are usually not too badly hurt. Of course, there are some overlooked cases, but overall, government shutdowns are orderly, and the problems are manageable.

But what about algorithmic stablecoins? If we look at algorithmic stablecoins from a bold and radical perspective, the ability to avoid systemic collapse and loss of a large number of users and funds should not rely on a constant influx of new users.

Can Terra safely exit?

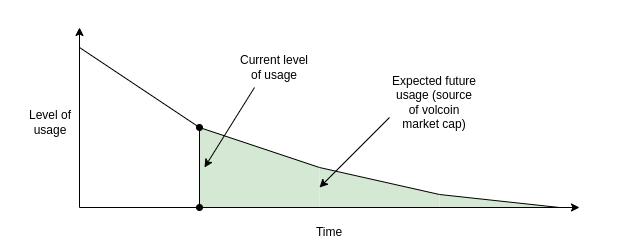

In Terra, the price of the volatile coin (LUNA) comes from expectations of future activity fees in the system. So, what happens if expected future activity drops to near zero? The market cap of LUNA declines until it becomes relatively small compared to the stablecoin. At this point, the system becomes very fragile: as long as the demand for the stablecoin is subjected to a small shock, it will lead to the target mechanism printing a large amount of volatile coin (LUNA), resulting in LUNA being over-inflated, at which point the stablecoin will also lose its value.

The collapse of this system can even become a self-fulfilling prophecy: if it seems likely to collapse, it will lower the expected future value of LUNA, leading to a decline in the market cap of the volatile coin (LUNA), making the system even more fragile, potentially triggering a very severe collapse, as we saw in May.

First, the price of LUNA falls. Then, the stablecoin starts to wobble. The system tries to support the demand for the stablecoin by issuing more LUNA. Due to a lack of market confidence and fewer buyers, the price of LUNA rapidly declines. Finally, once the price of LUNA approaches zero, the stablecoin will also collapse.

In principle, if the decline is very slow, people's expectations of future fees in the LUNA ecosystem and its market cap relative to the stablecoin are somewhat better. However, successfully managing it to ensure a slow decline is unlikely; it is more likely to drop suddenly and rapidly, followed by a loud crash.

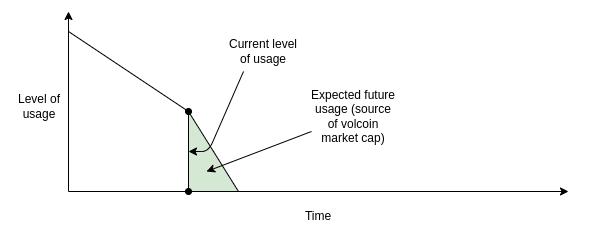

Safe gradual exit: Each step must ensure that the market cap of LUNA has enough expected future income to keep the stablecoin safe at its current level.

Unsafe gradual exit: At some point, there is not enough expected future income to justify having enough market cap of LUNA to ensure the safety of the stablecoin, which could lead to a collapse.

Can RAI safely exit?

The safety of RAI depends on assets external to the RAI system (ETH), so RAI is easier to exit safely. If a decline in demand leads to an imbalance (thus either holding demand declines faster or lending demand declines faster), the redemption rate will adjust to balance both. Lenders hold leveraged positions in ETH rather than FLX, so there is no risk of a positive feedback loop where a decline in confidence in RAI leads to a decrease in lending demand.

If, in extreme cases, all demand for RAI disappears simultaneously except for one holder, the redemption rate will skyrocket until ultimately every lender's safety is liquidated. The only remaining holder will be able to purchase the vault in the liquidation auction, use their RAI to immediately settle their debt, and withdraw ETH. This gives them the opportunity to obtain a fair price for their RAI, namely purchasing from the ETH in the vault.

Another extreme case worth studying is if RAI becomes a major application on Ethereum. In this case, a decrease in expected future demand for RAI will affect the price of ETH. In extreme cases, a series of liquidations could occur, leading to a chaotic collapse of the entire system. However, RAI's resistance to this possibility is much stronger than that of a Terra-style system.

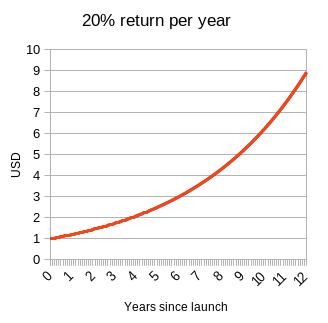

Thought Experiment 2: What happens if you try to peg a stablecoin to an index that rises 20% annually?

Currently, stablecoins tend to peg to the dollar. RAI is a small exception because its peg rate adjusts up and down with changes in the exchange rate, and the starting peg price is $3.14 instead of $1 (the exact starting value is friendly to the mathematically inclined, as a true math nerd would choose tau = $6.28). But they don't have to do this. You could peg a stablecoin to a basket of assets, a consumer price index, or any complex formula ("the value sufficient to purchase one hectare of land in the Yakut forest (i.e., global average CO2 concentration minus 375)"). As long as you can find an oracle to verify the index and there are market participants involved, you can make such a stablecoin work.

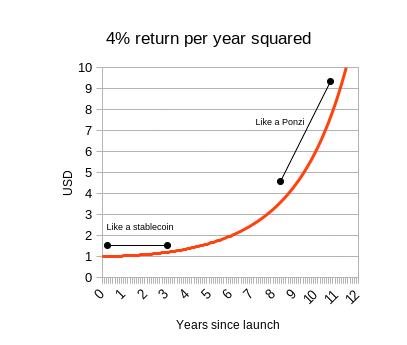

Clearly, there is no real investment that can achieve close to a 20% return annually, and absolutely no real investment can maintain a 4% return indefinitely. But what happens if you try?

What I want to say is that stablecoins essentially have two ways to track such an index:

It charges some form of negative interest rate to holders to essentially offset the growth rate in dollars of the index.

It turns into a Ponzi scheme, providing astonishing returns to stablecoin holders for a period until one day it suddenly collapses.

This should make it easy to understand why RAI (1) is better than LUNA (2). But it also highlights a deeper, more important fact about stablecoins: For a collateralized algorithmic stablecoin to persist, it must somehow include the possibility of implementing a negative interest rate. If RAI is programmatically prevented from implementing a negative interest rate (which was the fundamental practice of early single-collateral DAI), if pegged to a rapidly appreciating price index, it would also turn into a Ponzi scheme.

Even if you build a stablecoin to track a Ponzi index's crazy assumptions, stable currency must be able to respond in some way to situations where holding demand exceeds lending demand, even at zero interest rates. If you do not do this, the price will rise above the peg, and the stablecoin will become susceptible to bidirectional price fluctuations, which are quite unpredictable.

Negative interest rates can be implemented in two ways:

RAI dstyle, with a floating target that can decrease over time if the redemption rate is negative.

In reality, balances decrease over time.

Option (1) has user experience flaws, as the stablecoin no longer clearly tracks "1 dollar." Option (2) requires a developer experience flaw, as developers are not accustomed to handling receiving N tokens, which does not mean you can unconditionally send N coins later. But choosing one of these seems inevitable—unless you take the MakerDAO route, becoming a hybrid stablecoin that uses pure (decentralized) crypto assets and centralized assets (like USDC) as collateral.

What can we learn?

Overall, the crypto space needs to change its attitude of relying on endless growth to be safe. Saying "the world can operate in the same way" while maintaining this attitude is certainly unacceptable. Because the world is not trying to provide any returns, the economy does not rise rationally but rises pathologically, and of course, it deserves fierce criticism.

Instead, while we should expect growth, we should assess the safety of systems by observing their steady states, even their pessimistic states of how they would perform under extreme conditions, and whether they can ultimately exit safely. Just because a system passes this test does not mean it is safe; for other reasons, it may still be fragile. Insufficient collateral ratios or flaws or governance loopholes may exist, but extreme situations and robustness should be our primary focus.

Risk warning Risk warning

Risk warning Risk warning