Vader Research: How should we create value for the Token?

What different value accumulation mechanisms can we use? What are their respective advantages and disadvantages?

What different value accumulation mechanisms can we use? What are their respective advantages and disadvantages?Original source: Vader Research

Original compilation: Kxp, BlockBeats

The core business is in a growth phase and continues to generate revenue. The questions we need to consider now include—how can we create value for Token entities so that Token holders can share in the existing or future profits of related businesses? Additionally, what different value accumulation mechanisms can we use, and what are their respective advantages and disadvantages?

We will answer all these questions in this article. At Vader Research, we have a three-step approach to Token value accumulation:

Step 1: Clarify Token inflow channels

Step 2: Determine the payment currency for Token inflows

Step 3: Develop value accumulation mechanisms

The main content of this article includes:

Value and value creation

Step 1: Clarify Token inflow channels

Step 2: Determine the payment currency for Token inflows

Step 3: Develop value accumulation mechanisms

The right timing for value accumulation

1. Value and Value Creation

We have previously discussed value accumulation in our article on Token cap table allocation, which includes both existing value and future value.

In other words, value is created when assets flow into the ecosystem. These inflows can be in any currency (Stablecoin, L1 blockchain, native Token) and can accumulate 100% (mainly from NFT sales, upgrade fees, etc.) or after deducting a certain percentage of royalty fees into the protocol.

For example, Crypto Vnicorns sold 100 primary NFTs for $1 million. Assuming all proceeds from the transaction go to the Token entity, regardless of which currency was used in the sale (possibly USDC, ETH, or the native Crypto Vnicorns Token), the Token entity would generate a value inflow of $1 million.

For instance, Gambler A purchases a Gigidaiku NFT worth $100,000 from Gambler B, and the creator of Gigidaiku, Kimit Break, charges a 10% royalty fee on all secondary transactions. Assuming all proceeds from the transaction go to the equity entity, regardless of the currency used in the sale, Kimit Break would generate a value inflow of $10,000.

Whether these asset inflows should be recognized as revenue (influenced by the time period of value generation or payment currency) is a question for accountants to consider. What we should focus on is how to design a sustainable NFT economy, how to allocate resources effectively, and how to evaluate business decisions.

In practice, cash inflows and revenue recognition are often two different concepts. For example, if Adam pays Netflix $120 for an annual subscription, Netflix needs to recognize $10 of actual revenue each month, while that $120 is the cash inflow for the first month. Additionally, payments in the protocol's native currency may not be recognized as revenue.

For modeling purposes, we prefer to use inflow amounts rather than revenue, as inflow amounts are closer to traditional accounting cash inflows (cash flow statements) than revenue (income statements). However, we will also include non-Stablecoin cash flows, such as non-Stablecoin inflows and outflows of native or non-native currencies (NFTs, etc.), in the adjusted inflow statement.

The three traditional financial statements, valuation methods (DCF), and key performance indicators (retention rate, DAU, LTV, CAC) do not directly apply to web3. They only reflect the financial health and performance of web3 protocols more accurately after adjustments. At Vader Research, we have been studying proprietary statements and metrics to better illustrate value creation and accumulation.

Step 1: Clarify Token Inflow Channels

We have explained the inflow of Tokens above; now let's look at some common inflow channels and examples in web3. In gaming, the main inflow channels include:

One-time NFT sales of in-game characters, items/weapons, or land

Ongoing primary NFT sales (breeding/minting/crafting)

Upgrade/repair/energy fees

Battle passes

Staking/tournament entry fees

While games provide players with a sense of control by allowing them to "mint" or "breed" NFTs, the prices are still set by developers (or DAOs), and all funds flow directly to the protocol. Some of these NFTs are permanent, while others are consumable. Consumable NFTs may experience frequent sales, leading to more sustainable and recurring cash inflows.

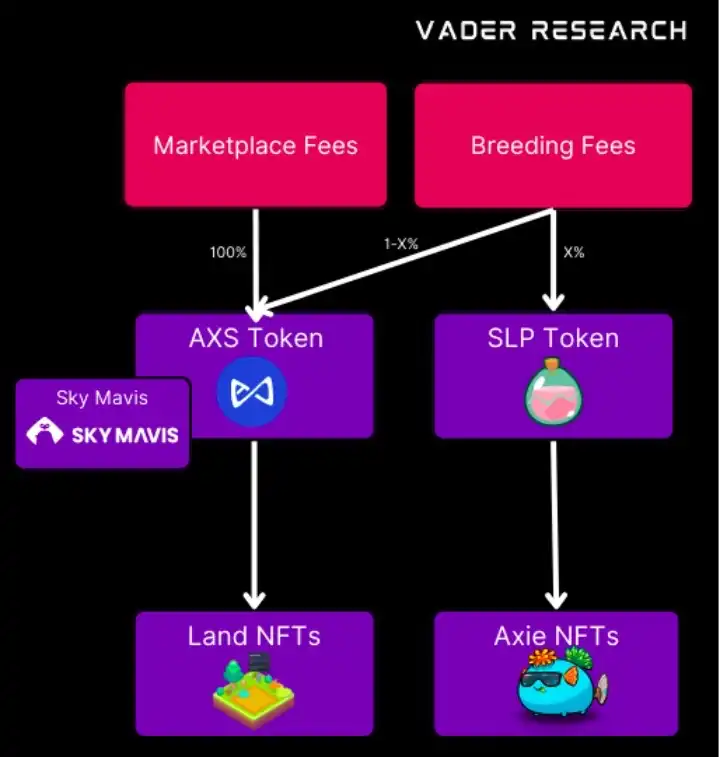

Axie Infinity:

Primary NFT sales

Primary land sales

Breeding fees, which count as ongoing primary NFT sales. The breeding fee is the price ceiling for NFTs, so as long as the secondary market NFT price is higher than the breeding fee, anyone has an arbitrage opportunity to breed/mint new NFTs.

Royalty fees—secondary market transaction fees

Skyweaver:

Challenge entry fees

Royalty fees

Primary non-card NFTs sales (hero skins, etc.)

Splinterlands:

Primary card NFT loot box sales

Card NFT upgrade fees

Royalty fees

Tournament organizer fees

STEPN:

Primary NFT sales

Minting fees

Repair/upgrade fees

Royalty fees

Ethereum:

- On-chain transaction gas fees

Step 2: Determine the Payment Currency for Token Inflows

We should determine one or more payment currencies for each inflow channel, meaning end users can choose one currency among all options or have only one choice. The decision-making process should consider the end user's experience, the diversification of cash inflows, value accumulation, and legal/regulatory matters.

Currently, there are three common payment currency options:

- Stablecoin (USDC, USDT, USD, EUR, etc.)

For end users, Stablecoins are the most convenient choice because when using Stablecoins, users do not have to deal with additional friction points, such as exchanging Stablecoins for another currency on decentralized or centralized exchanges.

Additionally, Moonpay's deposit tool allows end users to pay directly with credit cards without setting up or connecting a Metamask wallet. This is crucial because a significant proportion of users drop off due to additional friction points throughout the payment funnel. The fewer friction points there are, the lower the drop-off rate.

That said, Stablecoin payments may raise legal issues, as regulations in certain regions do not encourage players to use Stablecoins for payments.

2. Blockchain Currency (ETH, SOL, AVAX, MATIC, IMX, etc.)

For users, underlying blockchain Tokens are the second most convenient choice. Since users need to hold underlying blockchain Tokens to pay for on-chain transaction gas fees, they generally keep at least some Tokens. Moreover, most centralized exchanges support users depositing/withdrawing blockchain currencies to non-custodial wallets like Metamask.

3. Native Tokens (AXS, GMT, MANA, GALA, SLP, etc.)

Users can also choose to use the protocol's native currency, but they must deal with additional friction points, making it less convenient than other Tokens. Nevertheless, it gives the Token a specific utility and enhances users' perception of the Token purchase (this claim lacks scientific basis).

We can use one or two native Tokens for payments; for example, Axie's breeding fees can be paid with both AXS and SLP, so players must hold sufficient quantities of both Tokens to complete the transaction. Using native Tokens for protocol-related transactions allows the Token to truly possess "currency" attributes.

Step 3: Develop Value Accumulation Mechanisms

After completing the previous two steps, we can now select value accumulation mechanisms. Remember, not all cash inflows need to accumulate to the Token entity; some developers may prefer to accumulate value in equity entities, other Token entities, and various categories of NFTs.

Axie's breeding fees accumulate across multiple entities, with two main sources of funds: market fees and breeding fees. Market fees are entirely accumulated into the wallet address controlled by the AXS Token entity. X% of breeding fees are paid in SLP—accumulating value to the SLP Token entity; 1-X% of breeding fees are paid in AXS, accumulating to the wallet address controlled by the AXS Token entity.

Axie NFT owners can earn SLP through gameplay, while Land NFT owners can earn AXS through staking. In other words, the value of SLP indirectly accumulates to Axie NFTs, while the value of AXS indirectly accumulates to Land NFTs. Additionally, there are many other parameters, such as how much of the AXS staking rewards are allocated to Land NFTs, how much the breeding fee should be set, the respective proportions of SLP and AXS in breeding costs, and whether Axie NFTs are considered permanent assets.

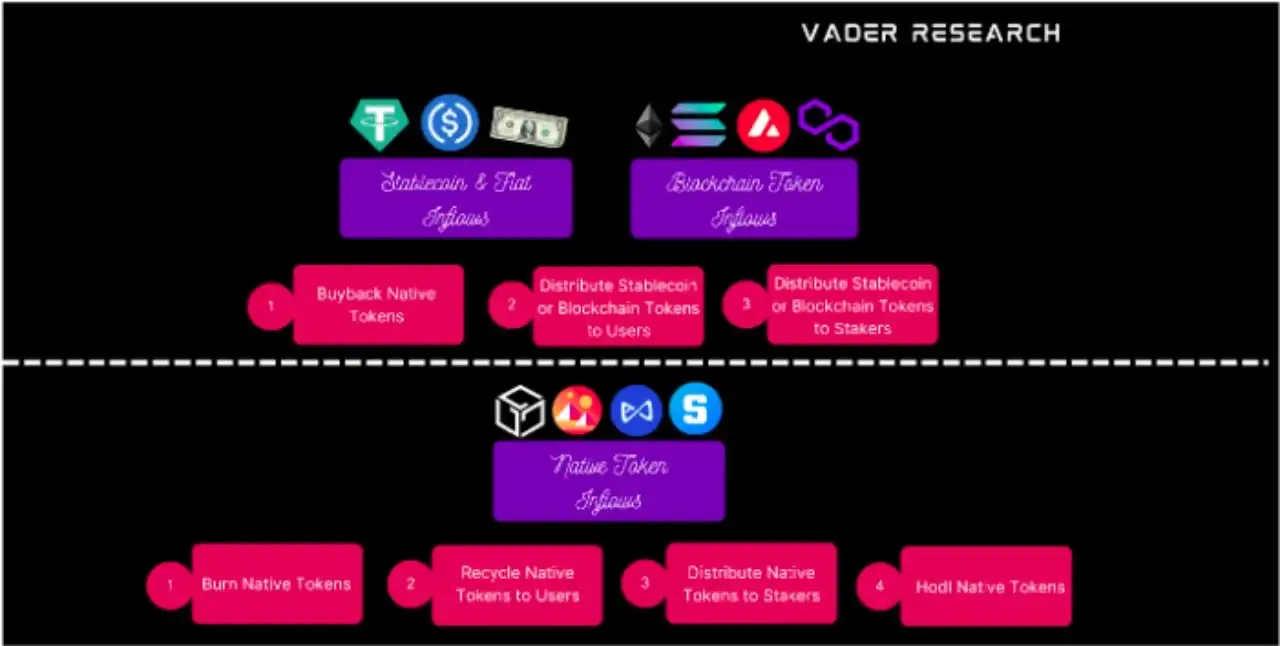

Here are the value accumulation options for each type of inflow currency:

- Stablecoin or blockchain Token inflows

A. Buy back native Tokens

Token buybacks are very similar to stock buybacks, where the Token entity purchases native Tokens from the open market through centralized or decentralized exchanges. As the circulating supply of Tokens decreases, value will proportionally accumulate to Token holders.

Buybacks can be executed at fixed intervals and proportions, such as using 70% of Stablecoin inflows each month to buy back native Tokens. Alternatively, we can also execute buybacks on an ad-hoc basis for more flexible asset management.

B. Distribute Stablecoin or blockchain Tokens to users

The inflowing funds will be used for marketing/participation expenses, which will then flow back into the economy through buybacks to incentivize specific behaviors, aiming to promote growth, improve retention, encourage monetization, and create long-term value. Unlike option 1, in the short term, value will accumulate to active protocol participants rather than Token holders, which will bring greater benefits to Token holders in the long term.

C. Allocate Stablecoin to stakers (similar to dividends)

Staking rewards are very similar to dividends, where the Token entity airdrops Stablecoin or blockchain Tokens to Token holders. Since Token holders will have more monetary assets after receiving staking rewards, value will proportionally accumulate to staked Token holders. This model can also be further optimized, such as allocating a higher proportion of Tokens to those who stake for longer periods.

We can combine the above methods: executing small-scale buybacks while distributing Stablecoin or blockchain Token rewards to users who qualify for rewards due to protocol activity and native Token ownership, which may be an effective way to allocate rewards.

2. Native Token inflows

A. Burn native Tokens

We can reduce the maximum supply of Tokens by permanently burning a portion of the circulating Tokens. This process can be automated during cash inflows, or conducted at fixed times monthly/weekly, or completed at any time based on the decisions of developers/DAOs. As the maximum supply of Tokens decreases, the value of all Token holders' Tokens accumulates.

B. Reclaim native Tokens for users

The inflowing funds will be used for marketing/participation expenses, which will then flow back into the economy through buybacks to incentivize specific behaviors, aiming to promote growth, improve retention, encourage monetization, and create long-term value. Unlike option 1, in the short term, value will accumulate to active protocol participants rather than Token holders, which will bring greater benefits to Token holders in the long term.

If cash incentives are provided in the form of native Tokens to highly loyal and engaged users, this may be a better reward currency compared to Stablecoin or blockchain Tokens. Because in this model, users willing to acquire native Tokens will not need to exchange native Tokens on centralized or decentralized exchanges, resulting in a higher yield of native Tokens than the yield of native Tokens after exchanging non-native Tokens.

Additional friction points when selling native Tokens will reduce users' willingness to sell native Tokens; similarly, additional friction points when purchasing native Tokens will also reduce users' willingness to buy native Tokens.

C. Distribute native Tokens as staking rewards

Staking rewards are very similar to dividends, where the Token entity airdrops Stablecoin or blockchain Tokens to Token holders. Since Token holders will have more monetary assets after receiving staking rewards, value will proportionally accumulate to staked Token holders.

D. Long-term holding of native Tokens

Rather than immediately burning Tokens or redistributing them to users/stakers, it may be better to store Tokens in a treasury and make value accumulation decisions later. Compared to merely holding native Tokens in a treasury, burning native Tokens can give retail investors more confidence, assuring them that there is a tangible and measurable Token burning mechanism in the system.

The Right Timing for Value Accumulation

After a public company generates profits and accumulates cash, it can use these funds in three ways:

Reinvest in growth/marketing/operations

Pay dividends to shareholders

Buy back stock

If management believes the business is mature enough and sees no attractive business investment opportunities, such as hiring new employees, establishing new service lines, or conducting brand marketing, then management may distribute excess cash as dividends to shareholders.

Typically, early-stage or rapidly growing startups do not pay dividends to their shareholders; they prefer to reinvest profits back into the business through user incentives, subsidies, or marketing expenses. Facebook was founded in 2004, became profitable in 2009, and went public in 2012, during which it never paid any dividends. The same goes for Amazon, which was founded in 1994, went public in 1997, became profitable in 2001, and also never paid dividends during those years.

Compared to mature companies in the oil, gas, or industrial sectors, these companies are still in a rapid growth phase. Executives at Facebook and Amazon prefer to use excess cash to expand into new business areas rather than return it to shareholders, as the former presents greater opportunities for value creation than the latter.

The timing of short-term Token value accumulation decisions, such as staking rewards, buying back native Tokens, or burning Tokens, is crucial. Token incentive rewards (whether native Tokens or other currencies) are one of the channels for user acquisition and participation. Other strategies include: performance marketing, influencer marketing, tournaments, etc. Web2 startups typically hire a growth/marketing officer to track the CAC and LTV metrics for each acquisition channel to determine the best marketing plan or reward distribution model.

For example:

The cost of acquiring users through Facebook ads is $20 per user, with a return of $5 LTV.

The cost of acquiring users through influencer marketing is $10 per user, with a return of $12 LTV.

Comparing these, influencer marketing is definitely the better choice. The same method applies to Token incentives, but the difference is that it can be used not only for user acquisition but also to encourage participation and improve retention, so more caution is needed when designing Token incentive programs.

Uber has designed a dynamic earnings incentive model for drivers—pickup earnings in designated areas are higher, and this earnings model changes based on traffic conditions in that area, different times of the day, the number of idle Uber cars, and existing/expected passenger demand. Uber aims to minimize wait times through this method, as long wait experiences often lead passengers to switch to other apps.

Therefore, for early-stage or even rapidly growing Crypto startups, burning Tokens or distributing staking rewards may not be effective resource allocation methods. In the previous article, we explored the reasons for extending Token lock-up periods.

If Token incentives cannot bring long-term benefits to the protocol, then we should reduce the scale of Token incentives and convert Tokens into fiat/Stablecoin for other marketing/participation/operational activities.

Conclusion

Whenever assets flow into the ecosystem, value is created, and the task of developers/DAOs is to determine the proportion of value accumulation for tradable assets. The selection of Token value accumulation mechanisms will depend on whether the inflowing funds belong to native Tokens or other currencies. Additionally, the timing of value accumulation is also very important.

Risk warning

Risk warning Risk warning

Risk warning