What are the challengers of GMX?

According to statistics, there are nearly 20 GMX fork protocols that have gone live, distributed across different chains. This article will review seven representative projects.

According to statistics, there are nearly 20 GMX fork protocols that have gone live, distributed across different chains. This article will review seven representative projects.Original Title: 《Challenges for GMX "

Author/DODO Research

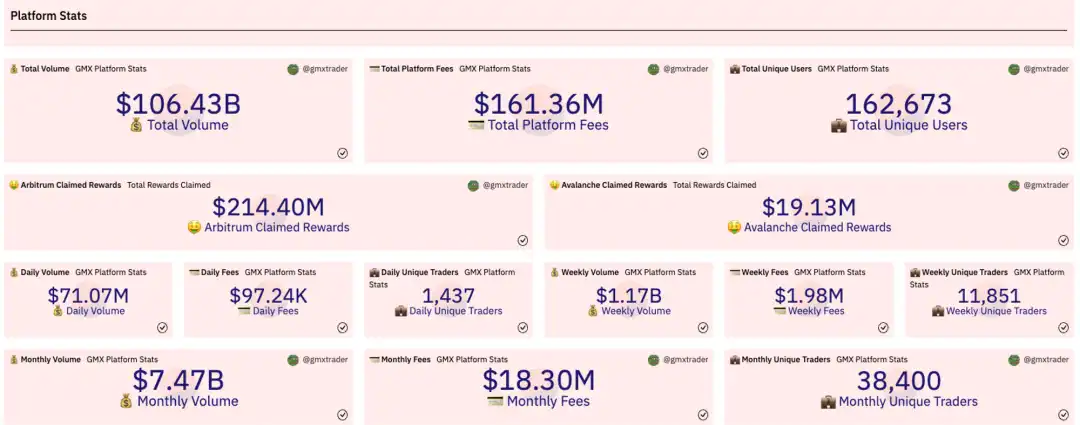

Since the GMX Token was launched on Binance in 2022, various metrics for GMX have continuously reached new highs. As of now, the total trading volume on the GMX platform has exceeded $10 billion, AUM has surpassed $1 billion, there are over 160,000 unique addresses, and the fees distributed to users have exceeded $100 million.

https://dune.com/gmxtrader/gmx-dashboard-insights

https://dune.com/gmxtrader/gmx-dashboard-insights

In the nearly one and a half years since its official launch, GMX has operated under scrutiny, but the "real yield" narrative has gradually led to acceptance of the GLP "betting" model.

As of now, there are nearly 20 GMX fork protocols that have been launched, according to Defillama, distributed across different chains. Below, we will highlight seven representative projects.

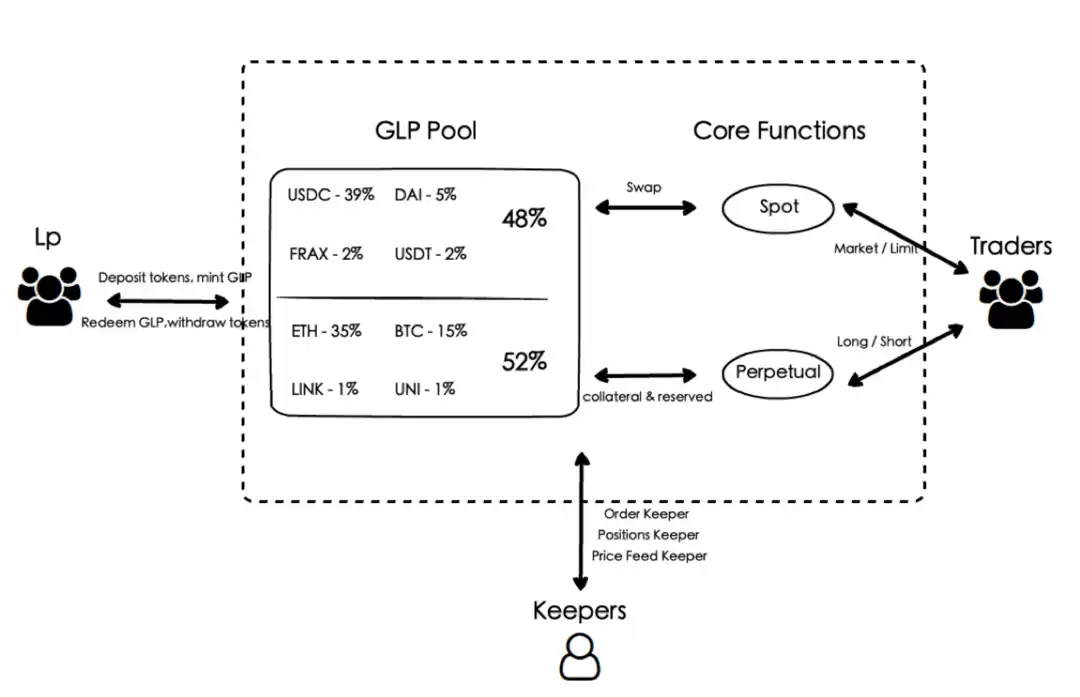

GMX Mechanism Diagram

Forks of GMX

Forks of GMX

1. Mummy Finance

Mummy Finance is a GMX fork supported by the Fantom Foundation. Mechanically, Mummy Finance has added the distribution of esMMY using NFTs in its cold start token distribution, granting NFT holders 80% of the treasury FTM dividends. In terms of fee distribution, the proportion of MLP has been reduced from 70% to 60%, with 5% allocated to the development team, and 5% used for buybacks and adding MMY-FTM LP to Equalizer (a Solidly fork). Additionally, apart from having FTM as part of the asset bundle in MLP, the rest of the mechanisms are the same as GMX.

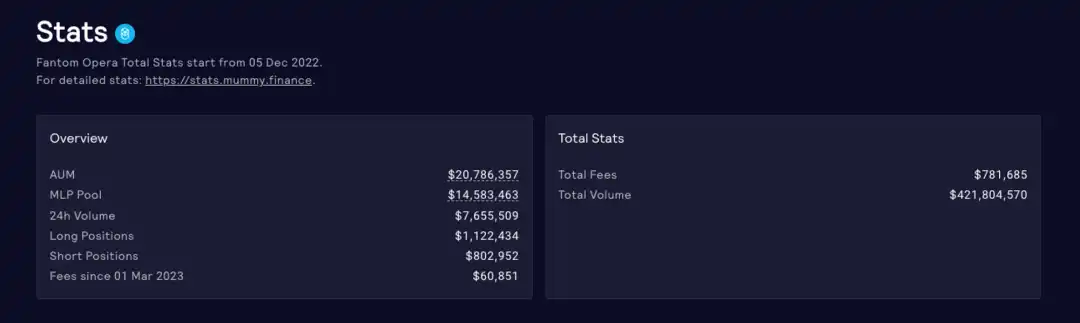

As of now (data as of March 5), Mummy Finance's platform trading volume has exceeded $400 million, with nearly $15 million in TVL for MLP, generating approximately $780,000 in fees, which is not impressive.

https://app.mummy.finance/#/dashboard

https://app.mummy.finance/#/dashboard

2. Vela Exchange

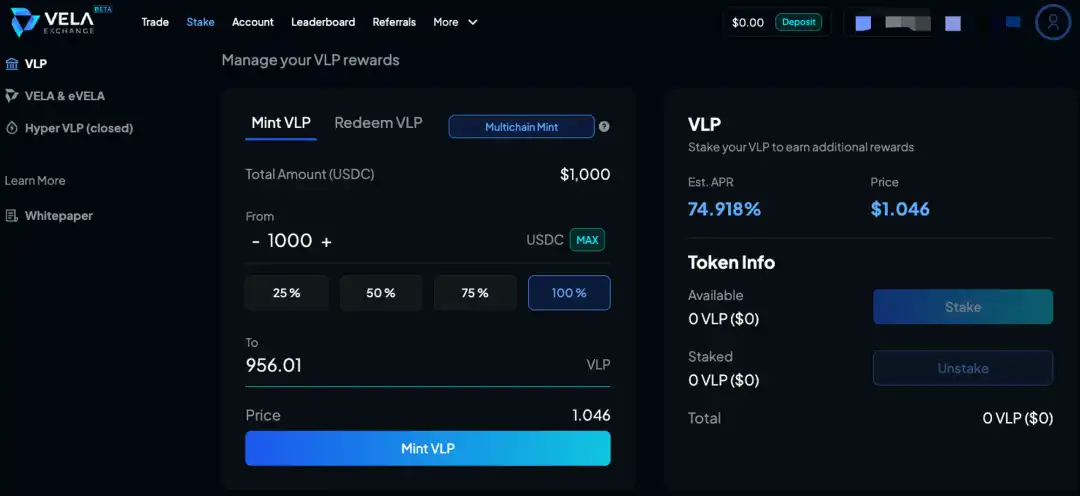

Vela Exchange was formerly known as Dexpool, an OTC market. Strictly speaking, Vela is not entirely a GMX fork, as it also incorporates mechanisms from the Gains Network. Vela mimics Gains' gDAI, using USDC to mint VLP and allowing further collateralization to obtain eVELA. Vela allows users to trade a variety of assets and supports more management functions for positions, such as taking profits multiple times on current positions, changing the amount of collateral in a position at any time, and increasing leverage on open positions at any time.

Unlike GMX, Vela's asset pricing is relatively decentralized, with only some contract addresses having administrator status, which reduces the risk of malicious actions. Prices refresh every minute or when price fluctuations exceed 0.1% (0.02% for forex). Vela also introduces a real-time funding rate that is calculated after users open positions and automatically deducted from the position.

Due to the absence of volatile assets, VLP holders only incur losses when traders profit. 50% of the protocol fees are distributed to VLP holders in USDC, 10% to VLP stakers in eVELA, 5% to VELA stakers in USDC, 10% to VELA stakers in eVELA, and the remaining 25% goes to the project.

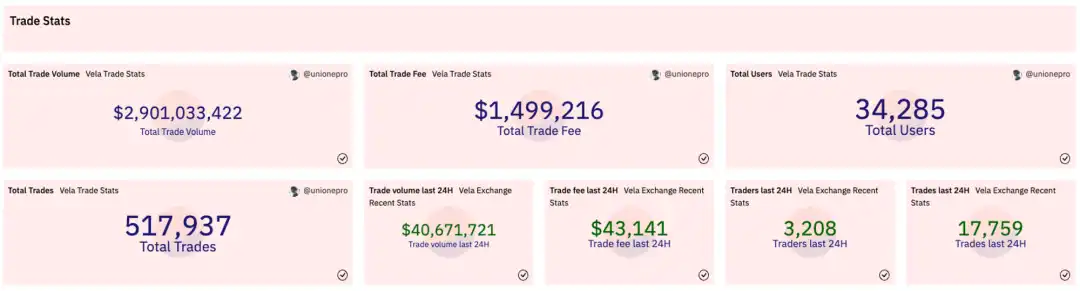

As of now, Vela, backed by VC support, has achieved nearly $3 billion in trading volume within just a few weeks of launch, generating only $1.5 million in trading fees. With recent trading incentive activities, Vela's data continues to show a significant upward trend.

https://dune.com/unionepro/vela-exchange-stats

https://dune.com/unionepro/vela-exchange-stats

3. Mycelium

Mycelium is a protocol supported by former BitMEX founder Arthur Hayes, merged from TracerDAO. Its GMX fork product is called Perpetual Swap. The economic model of MLP is almost identical to that of GLP, with trading fees of 0.4% for non-stablecoin assets and 0.03% for stablecoin assets. MYC staking rewards come from 10% of the platform fees, with a 14-day withdrawal period. For the LP portion of the esMYC rewards, there are no multiplier rewards for reinvestment; and the period for choosing linear redemption has been shortened to 6 months compared to GMX.

Additionally, the biggest difference from GMX is that Mycelium claims to offer a wider variety of tradable assets, including forex and commodity futures, but currently only supports WTI crude oil futures in addition to BTC and ETH. As of now, the TVL of Perpetual Swap is only about $6 million, but the total trading volume has reached $1.7 billion, generating over $1.6 million in protocol fees.

https://swaps.mycelium.xyz/dashboard

https://swaps.mycelium.xyz/dashboard

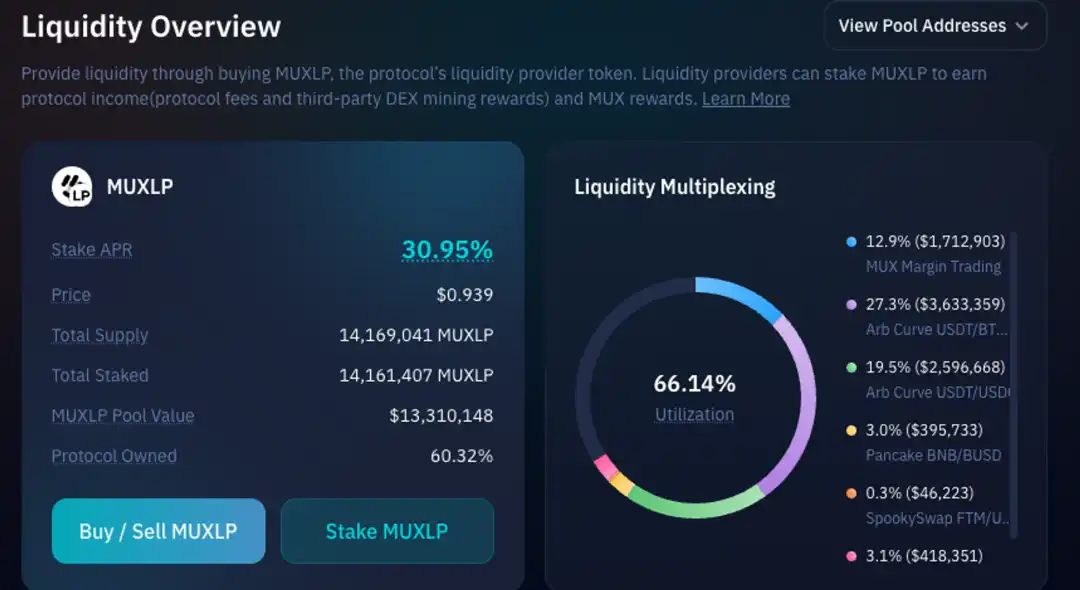

4. MUX Protocol

MUX was formerly known as MCDEX. During its complete transformation into a GMX fork, the team made a very notable change in its V2 version by creating a perpetual aggregator and building its own liquidity routing. This allows users to open positions with one click, reasonably distributing leveraged positions across different derivatives protocols. During the aggregation of trades, due to differences in maximum leverage supported by different platforms and varying liquidation thresholds, MUX provides additional margin to protect users from losses.

Moreover, MUX aggregates users' stablecoins and volatile assets, using part of them for liquidity in the derivatives market while placing the rest in other yield-generating protocols to earn additional income for users. In the upcoming V3 version, MUX will also support cross-chain aggregation, unifying derivatives liquidity across Arbitrum, Optimism, BNB Chain, Avalanche, and Fantom.

As of now, the trading volume of the MUX protocol has shown a healthier and more stable growth trend compared to other fork protocols, with a 7-day trading volume exceeding $60 million and the number of unique addresses surpassing 10,000.

https://stats.mux.network/public/dashboard/13f401da-31b4-4d35-8529-bb62ca408de8

https://stats.mux.network/public/dashboard/13f401da-31b4-4d35-8529-bb62ca408de8

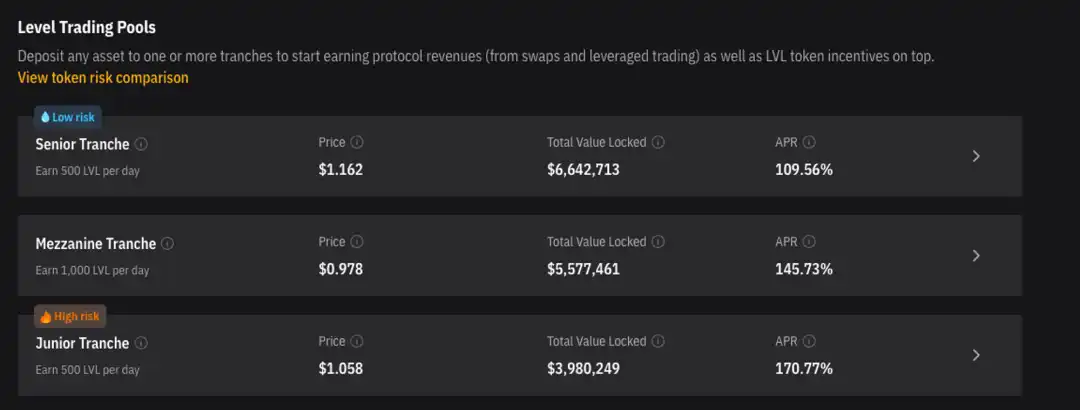

5. Level Finance

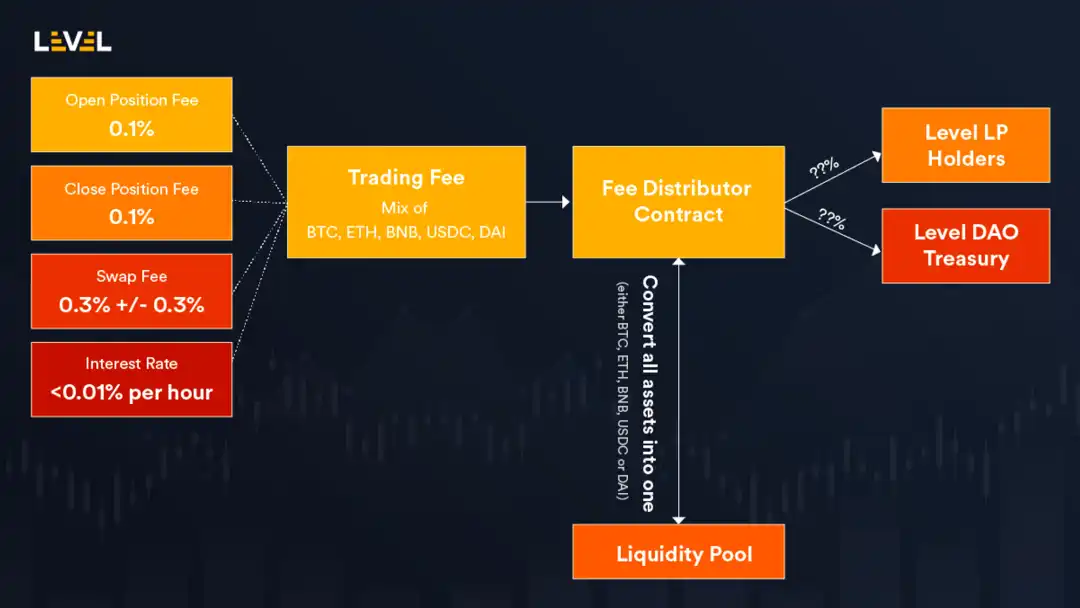

Level Finance on BNBChain is also a very distinctive GMX fork protocol. Level utilizes a tiered fund approach, providing different incentives and income distributions for different proportions of asset bundles, offering users a variety of ETF options.

Notably, Level adopts a dual-token model, with LVL as the incentive token subsidizing all tranches, and LGO as a pure governance token participating in the redistribution of 50% of protocol fees (the other 50% is distributed to all tranches via lyLVL). Additionally, the basic trading fee for non-stablecoin assets is 0.2%, while for stablecoin assets it is 0.01%, with a dynamic range of 0 - 0.6%.

As of now, traders have contributed over $3 billion in trading volume to Level Finance. Although the data is not as explosive as Vela's, it has been operating steadily for nearly 2 months, but the dual-token game design still needs to be tested.

6. El Dorado Exchange

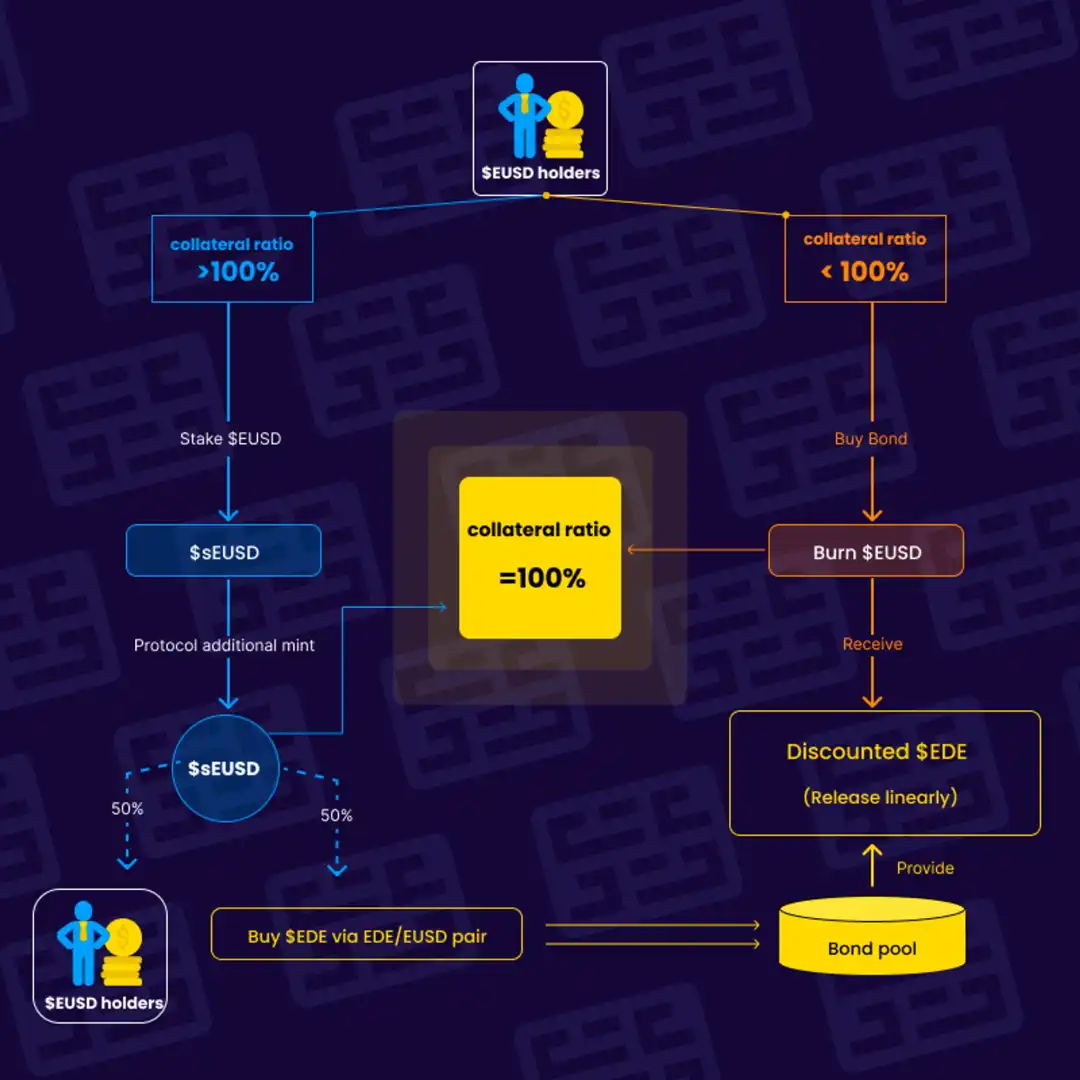

On BNBChain, in addition to Level Finance, there is another GMX fork with slight innovations—El Dorado Exchange. El Dorado adds a stablecoin EUSD supported by protocol fees to the tiered concept of Level, with 60% allocated to ELP and 40% to gEDE holders.

Since EUSD needs to maintain its peg, there is also a Stake & Bond mechanism to maintain the peg during collateral value fluctuations:

When the price rises and the collateral ratio exceeds 100%, the Stake mechanism is activated, allowing users to stake EUSD to earn interest rewards, increasing the total amount of EUSD and bringing the collateral ratio back to 100%; when the price falls and the collateral ratio is below 100%, the Bond mechanism is activated, allowing users to sell EUSD to the protocol in exchange for discounted EDE tokens. The protocol destroys the EUSD sold by users and gradually pulls the collateral ratio back to 100%.

In terms of data, due to excessive homogeneity with Level, El Dorado's data has been suppressed. El Dorado is also attempting to operate across multiple chains and is about to expand to Arbitrum.

In addition to the above protocols, there are others like Metavault (Polygon), Madmex (Polygon), Tethys Perpetual (Metis), Lif3 Trade (Fantom), and OPX (Optimism) that are essentially GMX clones operating within their respective ecosystems. It is evident that the vast majority of GMX forks are community projects, and the GLP and trader "betting" model has gained community recognition, accompanied by high LP incentives. Does this large number of forks remind you of the Uniswap V2 fork craze during the DeFi summer?

Currently, GMX still has several flaws: centralized oracle pricing, lack of bilateral funding rates, limitations on GLP's open contract volume, and potential liquidation risks during a bear market. There have also been instances of oracle price manipulation on Avalanche due to AVAX depth discrepancies, resulting in losses for GLP. The Uni V2 of 2020 also faced criticism: LPs could only rely on the protocol's token distribution to compensate for significant impermanent losses, lacked sufficient moats (Sushiswap Vampire Attack), and had low capital utilization.

It is foreseeable that the aforementioned shortcomings of GMX will soon be iterated upon by the synthetic asset version of X4 or innovated more flexibly by new protocols. Currently, there are several capital-backed protocols that are still not widely noticed and are worth tracking:

Lighter, a derivatives protocol supported by a16z, with unclear mechanisms. Vest Exchange, a GMX-like fork supported by Jane Street. Perennial Labs, which has launched a synthetic asset-backed AMM derivatives market, with many mechanisms very similar to GMX's X4 version, but the underlying is Opyn.

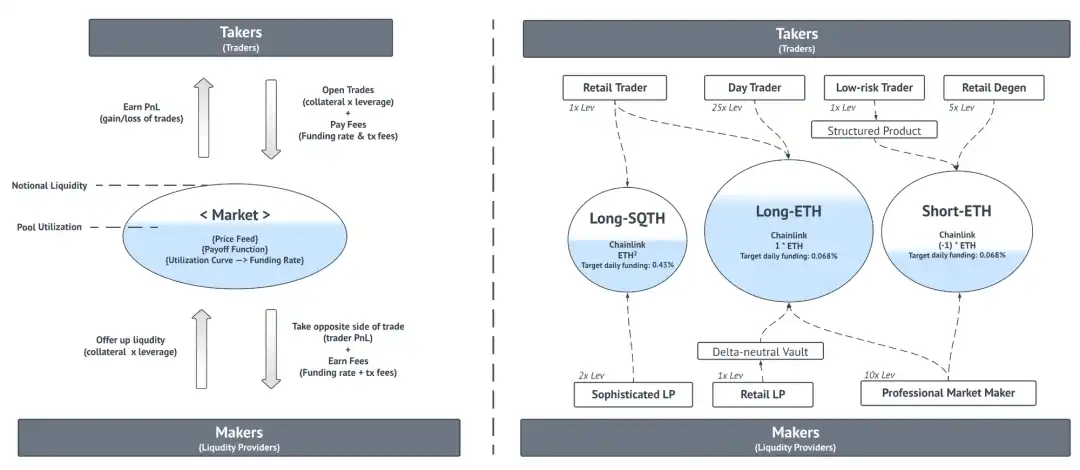

Among these, the most anticipated is undoubtedly Perennial. Specifically, Perennial provides a permissionless tool for building derivatives markets, rather than simply offering a trading market. It sets a set of trading rules for derivatives and allows anyone to set key parameters to establish their own market.

Perennial's trading model is based on a peer-to-pool approach, where each public market includes three roles: market builders, liquidity providers, and traders. Documentation shows that the current Long-SQTH pool is operated by Opyn's multi-signature address. The other two markets: the long and short markets on Ethereum, are managed by Perennial's multi-signature address.

Firstly, as market builders, they will only receive a portion of the fees from the derivatives market as income and are not required to provide liquidity. For market builders, the parameters they need to set include utilization curves, fee structures, leverage, and maximum liquidity. Among these, the fee structure (opening and closing fees) and maximum liquidity are relatively easy to understand, while the key parameters are the utilization curve and leverage.

The utilization curve refers to the functional relationship between market utilization and funding rates. Perennial indicates that this parameter references Aave and Compound's relationship between borrowing utilization and interest rates. In Perennial, traders need to pay funding fees to liquidity providers, and the level of these fees depends on the funding utilization (the ratio of the nominal value of the trader's open position to the nominal value of the liquidity provider's open position). The higher the utilization, the higher the funding fees, but it maintains a low growth rate before reaching 80%. Once it reaches 80%, to balance liquidity on both sides of the market, funding fees will increase significantly, and the market will be purely PvP between longs and shorts, aligning perfectly with the design concept of GMX X4.

Currently, Perennial is still in its early stages, and if GMX X4 emerges, the two will become direct competitors.

In summary, GMX was only fully accepted by the community after one and a half years since its launch, and the entire "value" discovery process is very similar to the emergence of Uniswap. Perhaps sometimes, it is not that a certain track cannot take off, but rather that the time has not yet come.

Risk warning

Risk warning Risk warning

Risk warning