IOSG Founder Annual Summary: The Bull Market Has Started to Return, Ethereum Is Strong and Resilient

The combination of factors such as Bitcoin halving has led to ecological prosperity, which is an inevitability amidst the偶然.

The combination of factors such as Bitcoin halving has led to ecological prosperity, which is an inevitability amidst the偶然.Author: Jocy, Founder of IOSG

1. The Scale Effect Growth Brought by Effective Regulation

The regulatory measures from Binance have landed, and many view this as negative news for the industry, seeing it as the process of "Crypto's largest unicorn finally compromising with regulation." However, in my opinion, this signifies that the largest potential risk zones have been cleared, the overall risk in the industry is controllable, and it is moving towards a more regulated market direction, which will also accelerate the advancement and implementation of ETFs.

We can imagine: currently, CME's trading volume accounts for over 25% of the entire BTC Futures (validating the speculation of significant traditional institutional entry). As U.S. regulation weakens, BTC trading on compliant exchanges (such as Binance/Coinbase) will occupy a major market share, and we might even see Nasdaq directly listing BTC and ETH. In such a scenario, one can imagine how large the daily BTC trading market size could be. Amid the U.S. debt crisis, the Federal Reserve and the Democratic Party seem to have reached some consensus on crypto governance, and they are likely strategizing for a larger game. Regulation can shake hands with the crypto market, which is one of the favorable factors for the industry, pushing it towards a broader market.

2. Data Tells Us the Bull Market Has Started to Return

Currently, we can see three events aligning closer together in the coming months:

The first is the accelerated approval of ETFs mentioned above (this will become an inevitable event, and Wall Street's acquisition of Bitcoin pricing power will also become a certainty);

The second is the Federal Reserve beginning to take interest rate cuts as inflation peaks and recedes (given the current debt situation, rate cuts will also become a more certain event);

The third is the halving of Bitcoin production within our industry and the iteration of Layer 2 infrastructure and application innovations in the Ethereum ecosystem.

These three events will occur simultaneously within the next six months, indicating that the industry will start to correct from the current market and has the opportunity to challenge a stronger bull market.

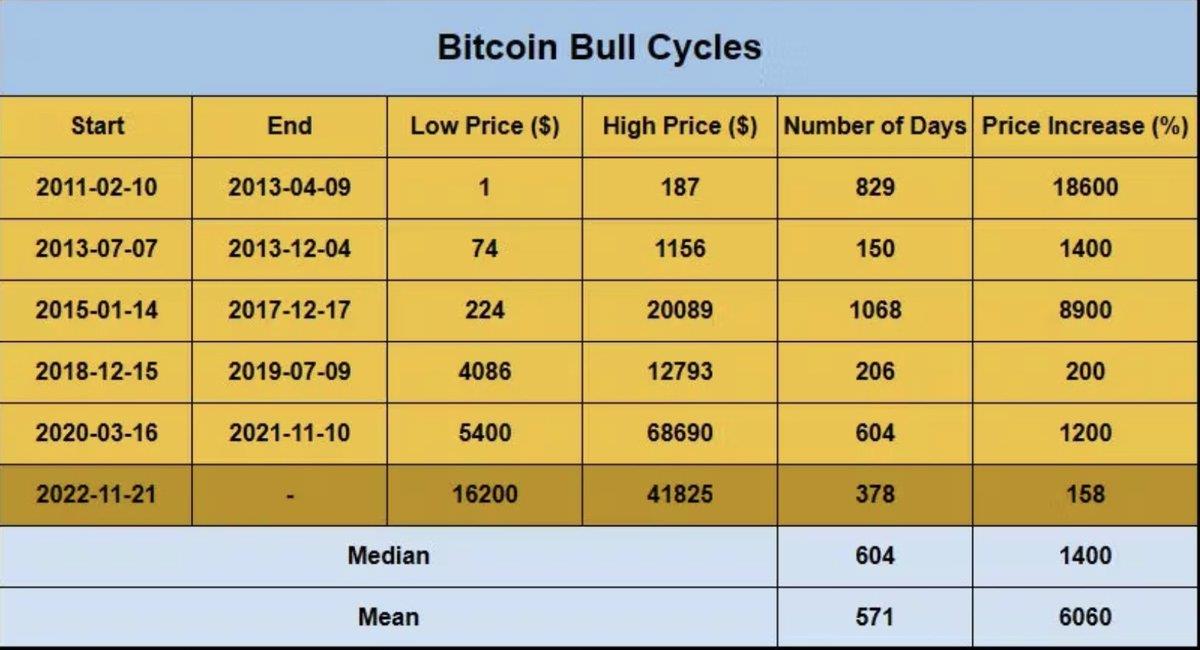

We can analyze historical bull and bear cycle data (cited from IOSG internal data analysts) to verify the current market situation. The median decline during historical bear market cycles is -77%, with an average decline of about -75% (recent bear market cycles have just dropped 77%). The median price increase during bull market cycles is 15 times, with an average increase of about 60 times.

As for the duration of the cycles, the median duration of bear market cycles is 354 days, with an average duration of 293 days (the recent bear market cycle also lasted close to 354 days). For bull market cycles, the median duration is 604 days, with an average duration of 571 days.

Analyzing historical information is valuable for understanding the cyclicality of the market. We are currently in the middle of a medium-length bull market cycle and are entering the climbing phase of this cryptocurrency bull market.

3. Continuous Ecological Innovation, Ethereum That Stands Tall

Regarding Ethereum's ecological innovation, we must mention the DevConnect conference in November, which gathered the most crypto developers this year and was also the event where Vitalik appeared the most. What happened at DevConnect?

Strengthening infrastructure: New technologies and niche markets have emerged. At L2Day, zkDay, and zk Accelerator, we saw numerous ZK and L2 protocols showcasing their strengths on different stages. Protocols based on zkRollup innovations, including Risc0/Nil Foundation, as well as Scroll/zkSync/Aztec, are beginning to compete for a diverse ecological landscape after launching on the mainnet.

1) ZK Coprocessor is a direction we find very promising. This direction includes Brevis, Axiom, Lagrange, and Herodotus. Brevis's application prospects are simple and easy to understand. The biggest difference between CEX and DEX is the Referral Program and loyalty programs. The more users you attract, the more trading volume, leading to more income and greater fee reductions. Brevis hopes that DEX can also have these plans to help Uniswap track all relevant on-chain interaction data, calculating each user's new user acquisition and trading situation in a trustless and secure manner, providing subsidies.

2) Different protocols in the Layer3 and Raas track are also starting to compete, including Conduit, Caldera, Gelato, etc., launching application chains based on gaming/social/DeFi. Due to the conflict between Israel and Palestine, many developers with Jewish backgrounds did not attend this conference. Nevertheless, you could still see countless developers and founders continuously promoting their Rollup as a Service solutions to the market, which is a rare early market! At one moment, I sat in a café surrounded by founders from different backgrounds in L2/L3, who were constantly pitching how their solutions could better help applications deploy on-chain and provide an experience equivalent to Web2 industry applications. This felt reminiscent of the early Web1.0 market around 2000 and the eve of the massive explosion of SaaS around 2012.

Many people say that Ethereum's network innovation is very slow, and many modules are subcontracted to different developer community tech teams. However, this precisely validates its strong network effects. The mainstream L2/L3/DA projects mentioned earlier are helping Ethereum better solve performance and use case issues. In the competitive wave of technological development, it seems that the entire crypto ecosystem, whether infra/dapps/vc, has become employees within the Ethereum network, contributing to the growth of this network without receiving salaries.

3) Recent new development directions are also closely related to hotly debated technologies, such as distributed GPUs and ZKML. The narrative and rise of Bittensor have shocked many, while Gensyn, which reached a seed round valuation of $500 million in the same field, has also attracted attention. They are both committed to bringing decentralized AI computing to users.

This hot field is not a castle in the air without application scenarios. A game developer once showed me how they combined Crypto with AI. Their demonstration surprised me with the natural close connection between Crypto and AI. They developed a fully on-chain football gaming platform for five-person autonomous battles based on ZKML technology, where every pass and goal is supported by ZKML, and the game results are automatically uploaded to the blockchain. Players can set different strategy models (ZKML) for battles (similar to the previous use of Bot/AI strategies in Dark Forest).

Although discussions around on-chain LLM and ZKML use cases and user acceptance still have differences, I believe we will soon witness more AI-centered crypto platforms. Recently, Vitalik also mentioned "d/acc" (decentralized acceleration), and we will see new projects from Unibot and former Flashbot founder Stephant, which will attract more new users to change their trading habits and start using bot-based trading methods.

The last direction returns to fully on-chain gaming, which I mentioned before. I want to share a young gaming genius developer, Small Brain—who designs intricate fully on-chain games like Word3, Drawtech, and Gaul. The designer behind these not only developed many outstanding gameplay features and created blockchain-characteristic games but also rallied a group of like-minded developers with unique viewpoints in the AW community, rapidly iterating on mud. They are progressing towards the goal of launching a new fully on-chain game every six weeks, conducting many interesting experiments.

I believe that Ethereum's skeptics overlook its compatibility and evolutionary capabilities, especially when new application products encounter bottlenecks. Ethereum can absorb new technologies the fastest to solve these bottlenecks (TPS, gas fees) and provide solutions to the problems most applications encounter. New alt L1s do not have a clear advantage in the segmentation of application scenarios.

In this cycle, Ethereum has two particularly typical and different network expansion models compared to the past.

The first is the output of currency and "security" through LSD assets, similar to the dollar's expansion, outputting to various Layer 2s, altchains, restaking protocols, and DA protocols; leveraging the spillover of Ethereum's LSD will greatly enhance Ethereum's network effects, making the characteristics of ETH as a medium of exchange and store of value more evident.

The second is technological absorption and mergers. In each cycle, Ethereum absorbs new technological paradigms based on the failures of past platforms, whether it is POS, which has been observed and summarized over four to five years before implementation, or scaling, from Plasma and sharding to various rollups, all of which learn lessons from many failed projects. In an open-source system, this ability is equivalent to the hundreds of billions of dollars in R&D sunk costs that most competitors have invested over past cycles, and this is all Ethereum's investment capital. I believe no platform (including Bitcoin) benefits as much from this as Ethereum does. Fortunately, throughout this cycle, Ethereum has not stopped continuing to absorb and merge.

What reason do we have to question Ethereum? Even in a bear market, countless projects and developers are still creating different products and protocols on the Ethereum network, and tens of thousands of developers and projects are selflessly creating new modular components in this network. All Web3 funds and investors cannot avoid investing in the Ethereum ecosystem, which means that with the current market cap of several hundred billion dollars in ETH, they will continue to bet hundreds of billions of dollars on Ethereum ecosystem projects, making Ethereum increasingly large and resilient!

4. The BTC Ordinals Ecosystem That Must Be Mentioned

With the rapid recovery of the market, Bitcoin, as the favored child, has many Bitcoin ecological projects starting to compete with various themes. It is extremely difficult to think about the value proposition of Ordi from the perspective of Bitcoin's fundamentalism. As the totem of the crypto world, Bitcoin's core function is value storage. With Bitcoin achieving broader social acceptance, consensus strengthening, value appreciation, institutional entry, ETF expectations, and factors like Bitcoin halving, ecological prosperity is an inevitable outcome; whether it is Bitcoin's second layer, Ordinals, or other protocol applications, we must first respect and protect Bitcoin's core, which is value storage.

The rise of Bitcoin meme and NFT-like assets is closely related to the retail movement against VC's "fair sale"; after all, under VC's dominance, retail investors can only eat the bones while the meat and soup go to the VCs. Compared to the ICO era, the valuation threshold for retail investors to enter is indeed too high (Ethereum's ICO in 2014 was only $23 million in valuation), and many projects are basically in the secondary market with FDVs of tens of billions of dollars, making the EV for retail investors too low.

It is in this market structure that retail investors initiated the current "Occupy Wall Street" movement in the crypto circle. However, this trend itself is also unhealthy. During DeFi Summer, there were also many "fair sale" projects, but in the end, "fair sales" turned out to be short-lived pump-and-dump projects, with various simple and crude forks, from "one-month tours" to "one-day tours," driving out good coins with bad ones.

In the end, after a cycle of sifting through the sands, there are few "fair sale" projects left, and those that remain for long-term development are still well-tested, with good financing structures. Long-term projects require long-term capital risk investment, while short-lived "fair sales" are difficult to support the development of a long-term ecosystem. The reason mainstream crypto institutions have not followed Bitcoin's technical ecosystem too closely is that there is indeed no substantial technical scalability, but more of a retail sentiment call under the "fair sale" label (of course, some institutions and exchanges may also operate such sentiments).

We do not support technological applications that threaten the robustness of Bitcoin's native network. Speculative trading based on sentiment cannot last long. The BRC20 protocol technology still has many shortcomings. As institutional investors, we do not encourage speculation but are willing to support more valuable and meaningful builders, bringing more ecologically valuable protocols.

Therefore, the crypto market is a melting pot. Current tokens like Ordi and other BRC20 tokens amplify speculation and price manipulation. I believe many people will earn considerable returns from this, but when we engage in more profit-driven trades without a thesis, we will gradually lose our way, and for similar reasons, we may also incur losses on some projects.

So if new friends preparing to enter the market see this tweet, or if there are family and friends around them who want to start buying under FOMO sentiment, I hope everyone can do a good job of mobilizing their thoughts and alerting them to risks, encouraging them to choose only between BTC and ETH, which is the simplest and least error-prone path. Adhering to principles in investing is very difficult; speculation and memes bring wealth effects, but how to see beyond these in the crypto market and step out of speculation and memes to support protocols with more valuable propositions and application prospects will also become an important responsibility and commitment for industry beneficiaries.

Thanks to Min Dao, Wendy, and Fiona for their editing suggestions.

【Disclaimer】The market has risks; investment requires caution. This article does not constitute investment advice. Users should consider whether any opinions, views, or conclusions in this article align with their specific circumstances; investing based on this is at their own risk.

Risk warning

Risk warning Risk warning

Risk warning