Arthur Hayes Blog: Why is the U.S. Approving Bitcoin Spot ETFs Now?

I wrote this lengthy preface to explain "Why now?" Why, at this crucial moment for the empire and its financial system, has the spot Bitcoin ETF finally been approved? I hope you can appreciate the significance of this development.

I wrote this lengthy preface to explain "Why now?" Why, at this crucial moment for the empire and its financial system, has the spot Bitcoin ETF finally been approved? I hope you can appreciate the significance of this development.^Author | Arthur Hayes^

^Compiler | Joyce, BlockBeats^

Note: This article is an excerpt and compilation based on the aforementioned Chinese version, and some details or information may have been omitted. We recommend that readers refer to the original text for a more comprehensive understanding.

Why Approve Bitcoin ETF Now

Medical expenses at the end of life are the highest, and we invest heavily to delay the inevitable death. Similarly, the elites of the United States and its vassal states, who strive to maintain the current world order, spare no effort because they benefit the most from it. However, since 2008, the United States has been experiencing a state akin to a deathbed, stemming from a global economic crisis triggered by improper mortgages to broke Americans, comparable in severity to the Great Depression of the 1930s. For this crisis, those blindly following the medieval new Keynesian barber's prescriptions are issuing the same prescriptions as a dying empire—"turn on the money printer."

The United States, Europe, and other vassal states, competitors, and allies have all adopted money printing as a means to alleviate the symptoms of imbalance in the global economic and political system. The U.S. is led by the Federal Reserve (Fed), printing money to purchase U.S. government bonds and mortgages. Europe is led by the European Central Bank (ECB), printing money to buy government bonds from Eurozone member states to sustain a flawed monetary (but not fiscal) union. Japan is led by the Bank of Japan (BOJ), continuing to print money in pursuit of the elusive inflation that disappeared after the 1989 real estate crash.

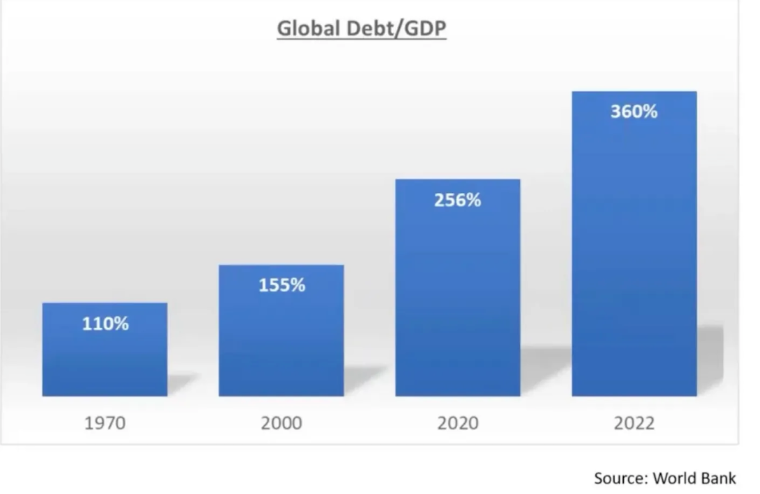

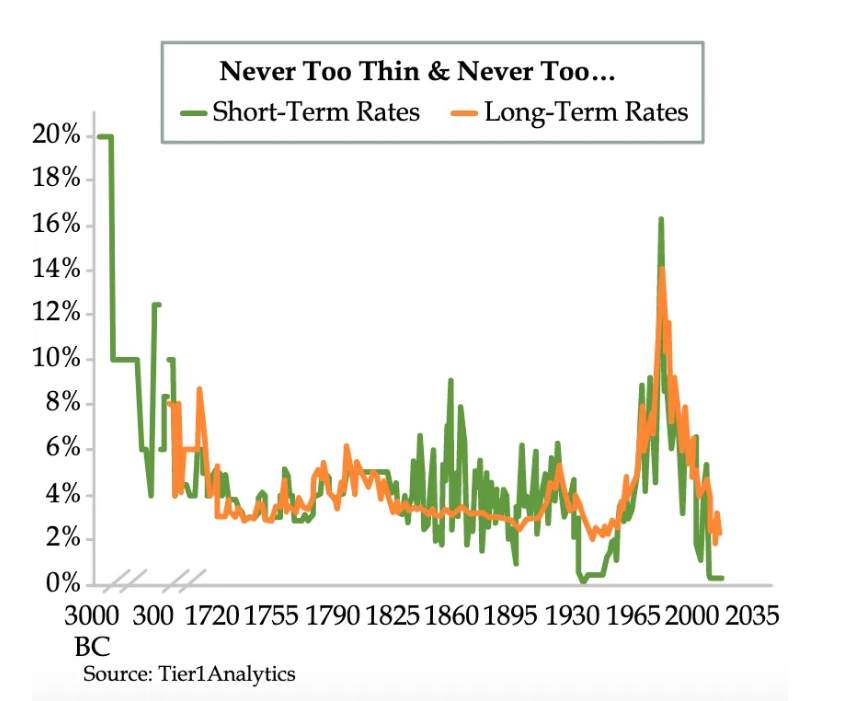

This reckless money printing has resulted in a rapid increase in the global debt-to-GDP ratio, with global interest rates reaching the lowest levels in 5,000 years. At its peak, nearly $20 trillion of corporate and government bonds had negative yields. Since interest is compensation for the time value of money, if interest is negative, are we indicating that time is no longer valuable?

As you can see, in response to the 2008 global financial crisis (GFC), interest rates were pushed to the lowest levels in 5,000 years.

This is the Bloomberg index of the total amount of global negative-yielding debt. From being nonexistent before the 2008 global financial crisis, it reached a peak of $17.76 trillion in 2020. This is the result of global central banks lowering interest rates to 0% and below.

Most of the world's population does not have enough financial assets to benefit from the global devaluation of fiat currencies. Commodity inflation has surged globally; in 2011 during the Arab Spring, avocado toast was less than $20. The era when middle-income households could afford median home prices without "parental banking" is long gone.

The only barely feasible way is to own some gold, but actual possession is impractical. Gold is heavy and hard to hide, making it susceptible to government regulation. Thus, ordinary people can only silently endure while the elites continue to revel in Davos as if time has stopped in 2007.

However, Satoshi Nakamoto released the Bitcoin white paper in an empire that was morally, politically, and economically bankrupt. The white paper outlined a system through which people could separate money from the state in a globally scalable way via machines connected to the internet and cryptographic proof, for the first time in human history. Bitcoin provides everyone with a complete financial system, no longer constrained by the old regime, requiring only a device connected to the internet.

People finally had a way to escape the frenzy of global fiat currency devaluation. However, after 2008, Bitcoin was not mature enough to provide a credible escape route for believers. In 2022, the Federal Reserve tightened financial conditions at the fastest pace since the 1980s, and the U.S. banking system was hit hard, with three banks collapsing in just two weeks. U.S. Treasury Secretary Yellen initiated the Bank Term Funding Program, secretly rescuing the entire U.S. banking system.

Cryptocurrencies were also affected by high interest rates, with centralized lending platforms going bankrupt, Terra Luna collapsing due to the drop in the price of its governance token Luna, resulting in the disappearance of $40 billion in illusory value. Then, centralized exchanges began to fail, with FTX being the largest, as operator Sam Bankman-Fried misappropriated $10 billion of customer funds, and as cryptocurrency asset prices plummeted, the scam was exposed.

Bitcoin, Ethereum, and DeFi projects did not fail; they experienced position liquidations and price drops without bailouts. In the ashes of 2023, U.S. hegemony and its vassal states could not continue to implement tight monetary policies, or the entire system would collapse. Interestingly, as U.S. long-term Treasury yields rose, Bitcoin and cryptocurrencies rebounded, while bond prices fell.

Bitcoin (white) vs. U.S. 10-Year Treasury Yield (yellow)

As interest rates rose, Bitcoin, like other long-term assets, showed a downward trend.

After the Bank Term Funding Program (BTFP), Bitcoin rose in sync with yields. Investors dissatisfied with the "system" began to sell U.S. Treasuries, with funds primarily flowing into the "magnificent seven" AI tech stocks (Apple, Alphabet, Microsoft, Amazon, Meta, Tesla, Nvidia) and to some extent into cryptocurrencies. Bitcoin became "the people's currency," no longer just a derivative of imperial risk assets, challenging traditional finance.

Bitcoin exhibited zero to slight negative correlation with bonds, and to avoid systemic collapse, the elite class needed to financialize Bitcoin by creating a Bitcoin Exchange-Traded Fund (ETF). This is similar to past practices in the gold market. To protect the global bond market, central banks like the Fed must print money again. In June 2023, BlackRock officially applied for a Bitcoin ETF, which was approved in 2023. This drew attention, especially compared to the Winklevoss brothers' applications that had gone unapproved for years.

A spot Bitcoin ETF is a trading product, not actual Bitcoin, and does not detach from the traditional financial system. To truly escape, one must buy Bitcoin and store it oneself.

I wrote this lengthy preface to explain "Why now?" Why, at this critical moment for the empire and its financial system, was the spot Bitcoin ETF finally approved? I hope you can appreciate the significance of this development. The global bond market is estimated to be worth $133 trillion; imagine if bond prices continue to fall, even if the Fed might start cutting rates in March, funds will flood into Bitcoin ETFs. If inflation bottoms out and begins to rise again, bond prices may continue to fall. Remember, wars lead to inflation, and wars are certainly occurring in the empire's periphery.

Market Impact of Spot Bitcoin ETF

The remainder of this article will discuss the market impact of the spot Bitcoin ETF. I will focus solely on BlackRock's ETF, as BlackRock is the largest asset management company in the world. They have the best ETF distribution platform globally. They can sell products to family offices, retail financial advisory firms, retirement and pension plans, sovereign wealth funds, and even central banks. All other companies will try their best, but in asset management, BlackRock ETFs will undoubtedly be the winners. Regardless of whether this prediction is correct, the following strategies will work for any issuer with high ETF trading volume.

This article will discuss the following topics, as well as how the internal workings of the ETF will create astonishing trading opportunities for those able to trade in traditional finance and crypto markets: the creation and redemption process of ETFs, spot trading arbitrage, and time series analysis of trading, ETF derivatives such as listed options, and the impact of ETF financing trades.

Putting all this aside, let’s make some money!

Cash Rules Everything Around Me

The problem is solved. The injection of funds (creation) and withdrawal (redemption) can only be done in cash. The most concerning aspect of this ETF is that it allows ordinary people to purchase the ETF with fiat currency and choose to redeem the ETF in Bitcoin. The purpose of this product is to store fiat currency, not to provide an easy way to buy Bitcoin with retirement accounts.

Creation

To create ETF shares, authorized participants (AP) must send the dollar value of the creation basket (i.e., a certain number of ETF shares) to the fund before a specific time each day.

APs are large traditional financial trading firms. Some significant institutions in traditional finance have already registered as APs for different ETFs. Some companies that once called for the government to ban cryptocurrencies, such as JP Morgan's CEO Jamie Dimon's firm, will also participate. This surprises me; )

Example:

The value of each ETF share is 0.001 BTC. The creation basket contains 10,000 shares, and at 4 PM Eastern Time, the value of these Bitcoins is $1,000,000. The authorized participant (AP) must wire this amount to the fund. The fund will then instruct its counterparty to purchase 10 Bitcoins. Once the Bitcoin purchase is completed, the fund will credit the ETF shares to the AP.

1 basket = 0.001 BTC * 10,000 shares = 10 BTC

10 BTC * 100,000 BTC/USD = $1,000,000

Redemption

To redeem ETF shares, the authorized participant (AP) must send the ETF shares to the fund before 4 PM Eastern Time. The fund will then instruct its counterparty to sell 10 Bitcoins. Once the Bitcoins are sold, the fund will issue $1,000,000 to the AP.

1 basket = 0.001 BTC * 10,000 shares = 10 BTC

10 BTC * 100,000 BTC/USD = $1,000,000

For us traders, we want to know where Bitcoin must be traded. Of course, the counterparties that help the fund buy and sell Bitcoin can trade on any exchange they prefer, but to minimize slippage, they must match the fund's net asset value (NAV).

The fund's NAV is based on the BTC/USD price from CF Benchmark at 4 PM Eastern Time. CF Benchmark obtains prices from Bitstamp, Coinbase, itBit, Kraken, Gemini, and LMAX between 3-4 PM Eastern Time. Any trader wishing to perfectly match NAV and reduce execution risk by trading directly on all these exchanges can do so.

The Bitcoin market is global, and price discovery primarily occurs on Binance (I guess based in Abu Dhabi). CF Benchmark excludes another large Asian exchange, OKX. This will be the first time in a long while that the Bitcoin market sees predictable and lasting arbitrage opportunities. I hope billions of dollars in trading volume will converge on those exchanges with lower liquidity, which follow the prices of their larger Asian competitors more closely, within an hour. I expect there will be some attractive spot arbitrage opportunities to exploit.

Clearly, if the ETF achieves great success, price discovery may shift from the East to the West. But don’t forget about Hong Kong and its mimicked ETF products. Hong Kong only allows its listed ETFs to trade on regulated exchanges in Hong Kong. Binance and OKX may service this market, but new exchanges will also emerge.

Regardless of what happens in New York or Hong Kong, neither city will allow fund managers to trade Bitcoin at the best prices; they may only trade on "selected" exchanges. This unnatural state of competition will only lead to lower market efficiency, from which we as arbitrageurs can profit.

Here’s a simple arbitrage example:

Average Daily Trading Volume Days (ADV) = (Exchange CF Benchmark Weight * Daily Closing Market Price (MOC) Nominal Value) / CF Benchmark Exchange USD ADV

Choose the least liquid exchange in CF Benchmark, i.e., the one with the highest ADV days. If buying pressure increases, the Bitcoin price on the CF Benchmark exchange will be higher than on Binance. If selling pressure increases, the Bitcoin price on the CF Benchmark exchange will be lower than on Binance. Then, sell Bitcoin on the expensive exchange and buy Bitcoin on the cheap exchange. You can estimate the direction of creation/redemption flows by looking at the premium or discount of the ETF trading against its intraday net asset value (INAV). If the ETF is at a premium, there will be creation flows. The authorized participant (AP) shorts the expensive ETF and then creates at the cheaper NAV. If the ETF is at a discount, there will be redemption flows. The AP buys the ETF at a low price on the secondary market and redeems at a higher NAV.

To conduct this trade in a price-neutral manner, you need to place dollars and Bitcoin on the CF Benchmark exchange and Binance. However, as a risk-neutral arbitrage trader, your Bitcoin needs to be hedged. To do this, you can buy Bitcoin with dollars and short the Bitcoin/USD perpetual swap contract on BitMEX. Place some Bitcoin as margin on BitMEX, while the rest of the Bitcoin can be spread across the relevant exchanges.

ETF Options

To truly get the ETF casino running, we need leveraged derivatives. In the U.S., the zero-day options (0DTE) market has exploded. One-day expiration options are akin to lottery tickets, especially when you buy them at out-of-the-money (OTM) prices. Now, 0DTE options have become the most traded options instrument in the U.S. Of course, people love to gamble.

After the ETF is listed for a while, options will start appearing on U.S. exchanges. Now, the real fun begins.

In TradFi, it’s hard to get 100x leverage. They don’t have places like BitMEX that can solve the problem. But the premiums on shorter-dated OTM options are very low, which creates high leverage or gearing. To understand why, brush up on your theoretical options pricing knowledge by studying the Black-Scholes theory.

Degen traders with brokerage accounts that can trade on U.S. options exchanges will now be able to make high-leverage bets on Bitcoin prices in a liquid manner. The underlying asset for these options will be the ETF.

Here’s a simple example:

ETF = 0.001 BTC per share

BTC/USD = $100,000 ETF share price = $100

You believe Bitcoin's price will rise by 25% by this weekend, so you buy a call option with a strike price of $125. This option is an out-of-the-money option because the current ETF price is 25% lower than the current strike price. The volatility is high but not extreme, so the premium is relatively low at $1. You could lose a maximum of $1, and if the option quickly goes into the money (above $125), you can earn more profit from the change in the option's premium, while if you just bought the option, you could earn a 25% profit by selling the ETF shares yourself. This is a very rough way to explain leverage.

In the U.S. capital markets, these enthusiastic traders are a serious bunch. With these new high-leverage ETF options products, they will create some chaos in Bitcoin's implied volatility and forward structure.

Forward Arbitrage

Call Option Price - Put Option Price = Long Forward Contract

As lottery ticket traders push up the prices of ETF options, the prices of out-of-the-money options will rise. The opportunity provided can be realized through arbitrage between the BTC/USD perpetual contract (like the one on BitMEX) and the ATM forward contracts derived from ETF option prices.

Futures Basis = Futures Price - Spot Price

I expect the trading price of the ETF ATM forward basis to be higher than the BitMEX futures basis. Here’s how to trade it.

Short the ETF ATM forward by selling ATM call options and buying ATM put options.

At the same time, buy a BitMEX Bitcoin/USD fixed expiration futures contract with an expiration date similar to the ETF options.

Wait for prices to converge as expiration approaches. This won’t be a perfect arbitrage, as BitMEX and the ETF use different trading prices to construct the Bitcoin spot index price.

Volatility (Vol) Arbitrage

To a large extent, when you trade options, you are trading volatility. Currently, traders trading Bitcoin options on crypto-native non-U.S. exchanges have different preferences for expiration and strike prices compared to traders trading ETF options. I predict that the trading volume of ETF options will dominate the global Bitcoin options liquidity. Since these two groups of traders, the dollar-based U.S. traders and the non-dollar trading traders, cannot interact on the same exchange, arbitrage opportunities will arise.

When options with the same expiration and strike price trade at different prices, there will be direct arbitrage opportunities. Additionally, there will be more general volatility arbitrage opportunities, where certain parts of the ETF options volatility surface outside the U.S. show significant differences from the Bitcoin volatility surface. Discovering and exploiting these opportunities requires more trading experience, but I know there will be many French speculators engaging in arbitrage in these markets.

MOC (Market on Close) Liquidity

As the ETF will lead to a surge in trading volume of ETF derivatives listed in the U.S., the CF Benchmark index's closing price at 4 PM will become very important. The value of derivatives comes from their underlying assets. With billions of dollars in nominal options and futures expiring daily, matching the closing transaction price of the ETF is crucial to aligning net asset value (NAV).

This will create statistically significant trading behavior around 4 PM Eastern Time and during trading hours on other days. Those skilled at handling datasets and possessing excellent trading bots will earn substantial profits by arbitraging these market inefficiencies.

ETF Financing (Creation Loans)

Centralized lending platforms like Blockfi, Celsius, and Genesis have been very popular among Bitcoin holders who want to borrow fiat currency using their Bitcoin as collateral. However, the dream of an end-to-end Bitcoin economy has yet to be realized. Loyal Bitcoin supporters still need fiat currency to pay for necessities, using that not-so-clean fiat currency.

All the centralized lending platforms I just mentioned have collapsed, along with many others. It has become more difficult and expensive to borrow fiat currency using Bitcoin as collateral. Traditional finance is very accustomed to lending against liquid ETFs as collateral. As long as you pledge Bitcoin ETF shares, it will now be possible to obtain large-scale fiat currency loans at competitive prices. For those who believe in financial freedom, the question is how to maintain control over Bitcoin while leveraging this cheaper capital.

The solution to this problem is to exchange Bitcoin for ETFs. Here’s how it works.

APs who can borrow in the interbank market will create ETF shares and hedge Bitcoin/USD price risk. This is the creation of a lending business. In Delta-One terms, it is the repo value of ETF shares.

Here’s the process:

Borrow dollars in the interbank market and cash create ETF shares.

Sell ATM call options on the ETF and buy ATM put options on the ETF to create a synthetic short forward contract.

The act of creating ETF units will generate a positive spread, i.e., forward basis > interbank dollar interest rates.

Lend ETF shares in exchange for Bitcoin collateral.

Let’s bring in Chad (a degen-like figure in the crypto space) to discuss how he needs to handle his Bitcoin:

Chad is a holder of 10 Bitcoins who needs to pay his AMEX bill in dollars; the champagne at those bars is expensive. Chad contacts his friend Jerome, a cunning Frenchman working at SocGen, who was once an alternative in major financial back offices and went to jail for aggressive futures trading but got his job back (in France, you can’t fire anyone) and is now responsible for running the crypto trading desk. Chad asks Jerome for an exchange of Bitcoin for ETFs for 30 days. Jerome quotes -0.1%. This means Chad will exchange 10 Bitcoins for 10,000 ETF shares, assuming each share is worth 0.001 Bitcoin, and after 30 days, Chad will get back 9.99 Bitcoins.

During the 30 days that Chad holds 10,000 ETF shares instead of 10 Bitcoins, he will pledge the ETF shares to his traditional financial brokerage for a very cheap dollar loan.

Everyone is happy. Chad can continue to show off at the club without having to sell his Bitcoins. And Jerome earns the financing spread.

The ETF financing business will gradually become very important and influence Bitcoin interest rates. As this market develops, I will focus on attractive ETFs, physical Bitcoins, and Bitcoin derivatives financing trades.

Liquidity Will Ultimately Flow to Bitcoin

For these trading opportunities to last a long time and allow arbitrageurs to execute them at sufficient scale, the complex structure of the Bitcoin spot ETF must trade billions of dollars in shares daily. On Friday, January 12, the total daily trading volume reached $3.1 billion. This is very encouraging, and as various fund managers begin to launch their vast global distribution networks, trading volume will only increase. There is a way to trade the financial version of Bitcoin within the traditional financial system, allowing fund managers to escape the poor returns currently offered in this global inflation environment.

We are in the early stages of this ongoing global inflation period. There is a lot of noise, but over time, for fund managers running stock-bond correlations, the changes will become apparent. At the zero interest rate point, bonds cease to play a role in portfolios, especially in the presence of persistent inflation. The market will gradually realize this, and the sell-off of over $100 trillion in the bond market will devastate nations. Then, these fund managers must find another asset class that has no substantial correlation with stocks or any traditional financial asset category. Bitcoin achieves this.

Risk warning

Risk warning Risk warning

Risk warning