The beginning of "Meme 2.0"? Pump.fun and the future path of on-chain financing

The on-chain issuance craze of Pump.fun has sparked valuation controversies, and its innovative mechanisms, capital layout, and strategic vision reveal the evolutionary direction of Meme coins.

The on-chain issuance craze of Pump.fun has sparked valuation controversies, and its innovative mechanisms, capital layout, and strategic vision reveal the evolutionary direction of Meme coins.Guests: Haseeb Qureshi, Managing Partner at Dragonfly

Joe McCann, Founder and CEO, Chief Investment Officer at Asymmetric

Host: Laura Shin

Podcast Source: https://x.com/laurashin/status/1945260654434083086

Compiled by: ChainCatcher

ChainCatcher Editorial Summary

Haseeb Qureshi, as a Managing Partner at Dragonfly Capital, is a leader in the field of crypto infrastructure investment, with his modular blockchain theory profoundly influencing industry evaluation standards; Joe McCann's Asymmetric has achieved counter-cyclical profits in a bear market through quantitative models, and its research on MemeCoin liquidity layering is changing market valuation logic.

This episode of the podcast gathers industry experts to delve into hot topics surrounding the innovative platform Pump.fun. You will hear unique insights into Pump.fun's rapid rise, its fierce competition with rival Bonk, and its grand future strategy. In this episode, Haseeb emphasizes that the stablecoin liquidity index has reached levels indicative of a bull market, while Joe reveals a historic turning point where retail spot buying has surpassed institutional buying for the first time.

ChainCatcher has organized and compiled the content (with edits).

Key Points Summary

- Pump.fun's ICO unexpectedly sold out in 12 minutes, demonstrating its strong market appeal despite complex market sentiment.

- Let's Bonk has rapidly emerged as a competitor, at one point surpassing Pump.fun in weekly revenue and token issuance, especially gaining widespread community support, while Pump.fun is viewed by some as a "predatory" platform.

- The differing stances of Coinbase and Kraken in participating in the Pump.fun ICO reflect their respective regulatory considerations and market positioning.

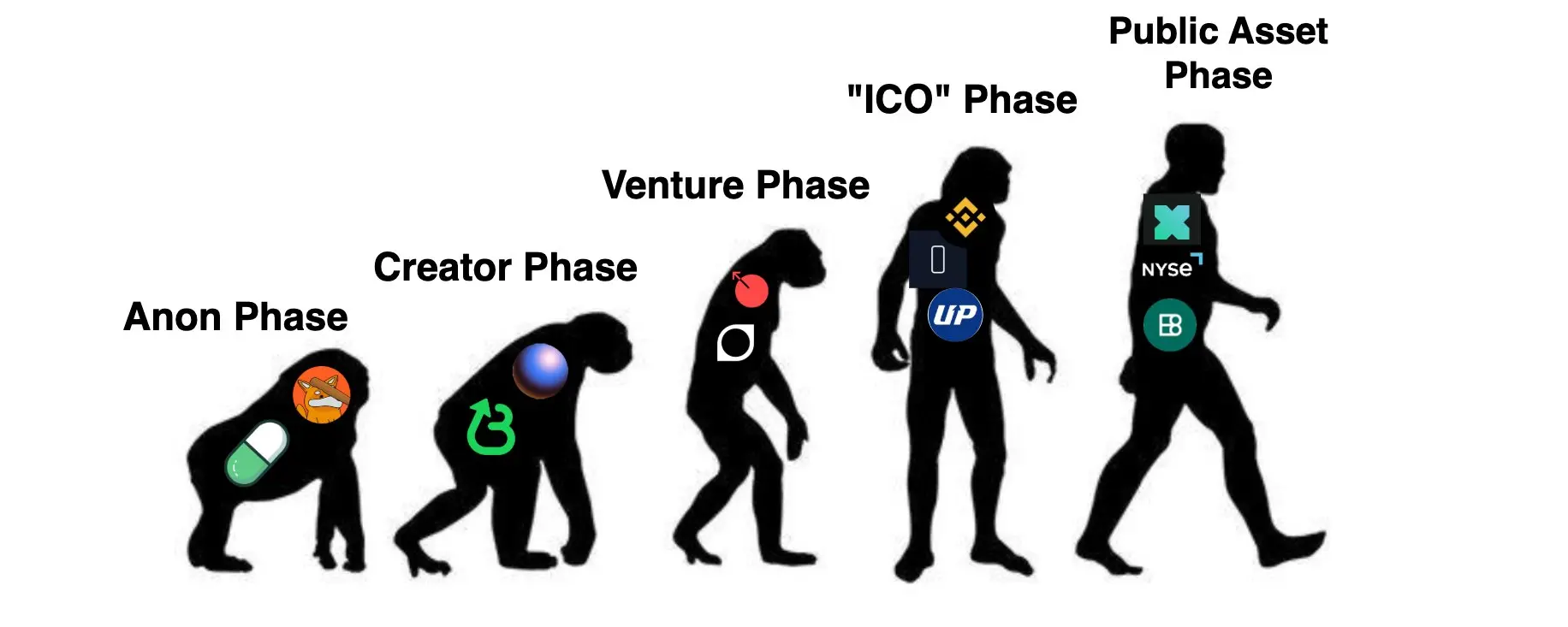

- Meme coins are not a fleeting trend but are entering a new stage of development as an iteration of "software."

- Pump.fun's acquisition of Kolscan aims to vertically integrate its business and optimize revenue streams by controlling user experience.

- Pump.fun has ambitions to challenge Twitch and TikTok, planning to build a comprehensive platform that integrates streaming, trading, analytics, and portfolio management, targeting younger audiences and streaming demographics.

- Despite some negative views on meme coins in parts of the market, their continued activity and the success of the Pump.fun ICO suggest that the altcoin market may be entering a new, more active cycle.

1. Pump.fun ICO: Valuation Controversy and On-chain Financing Wave

Laura Shin: As we all know, Pump.fun officially announced its ICO last week. They claim to want to beat Facebook, TikTok, and Twitch on Solana. However, the market response has been very complex. Some say it is "predatory," while others question the high valuation. Joe and Haseeb, what do you think about the financing data, valuation, pricing, and token distribution of this ICO?

Joe McCann: I’ve mentioned before on other shows that the crypto industry has redefined the term "revenue" to mean "predation." Pump.fun is a clearly profitable company; they have developed a killer app and generated actual revenue. Of course, some may misuse it, which has led to the "predatory" claims. But no one calls it predatory when meme coin prices skyrocket; it’s only when they go to zero that people say that. So I think Pump.fun is a model for building successful companies. While people online may be unhappy due to the lack of airdrops or distribution ratios, you can never satisfy everyone on the internet.

Haseeb Qureshi: I also noticed a few particularly interesting points. First, as Joe mentioned, the online reaction to this financing has been very negative, claiming it is predatory. Second, although there is a lot of criticism on social media, the actual financing was oversubscribed, indicating strong demand. Third, it may mark the return of ICOs, especially in the context of the Trump administration and the SEC relaxing regulations; this method of on-chain capital formation may become popular again. Of course, this ICO did KYC, unlike the old-fashioned ICOs of 2017 where "money was sent to a wallet," but it does resemble a CoinList on steroids.

Laura Shin: That’s right, I remember some ICOs in 2017 also did KYC, like Civic.

Haseeb Qureshi: Yes.

Laura Shin: I want to ask about the fact that they have $750 million in revenue. I can think of some reasons why they might need more funding, but I'm just curious, as a venture capitalist, I believe Dragonfly must have had the opportunity to invest. I’ve heard Rob Haddick say they usually don’t invest in companies at that stage, but from a venture capital perspective, do you think this is reasonable? Do you think the valuation is reasonable? What are your thoughts on these numbers?

Haseeb Qureshi: The token is currently trading at about $0.052. I think as people gradually receive their tokens, along with the exchange listings, the price will fluctuate significantly. So it’s clear that this pricing is reasonable. In fact, I think they did a great job with the pricing, like a fantastic IPO premium. You make 25%, leaving little profit margin but making everyone involved feel good. Simply put, if you participated in the ICO, you’re probably up about 25% now. I think this pricing is smart; you want to see everyone making money, with some safety net, while still having room for growth.

From my perspective, it’s unlikely that the price of Pump's token will fall significantly below the issue price, so their pricing approach is friendly to retail investors. However, the market environment has changed significantly from when they first announced the price to now; the token market is rising, Bitcoin has also hit new highs, while the market was quite sluggish when they initially priced it. If you look at the presale market on Aevo and the performance of Hyperliquid after its listing yesterday, prices are generally around $5 to $6. The overall market view is quite consistent, with everyone believing that the project should trade at a market cap of $5 billion to $6 billion.

Joe McCann: There are two points worth expanding on regarding his perspective. First, the most special aspect of this ICO is that the vast majority of the fundraising was done on-chain. 75% of the tokens were allocated to wallets that invested at least $1 million, which are typically not retail investors but rather a form of "smart money" that is very familiar with on-chain infrastructure. This is completely different from traditional fundraising methods.

Second, this fundraising adopted a model of on-chain Solana capital formation + Hyperliquid price discovery. This concept is very interesting. For example, I am a Circle investor; look at its IPO process: there was a lot of criticism about their pricing being too low or repeatedly adjusting the listing price, and they had to struggle to match orders when trading officially began. For us crypto natives, this method seems particularly outdated. In contrast, Hyperliquid's price discovery mechanism is very efficient. Even though the token hasn’t officially launched, the trading volume has already surged to around $500 million, which is incredible. The final opening price also closely matched the presale price. In my view, this combination of on-chain fundraising + off-chain price discovery does not exist in traditional finance, which is what makes it so appealing.

2. Multi-Exchange Coordination and On-Chain Price Discovery Mechanism

Laura Shin: We just talked about the issue of price reasonableness, but I want to delve deeper into the design of this ICO. We see that this is not the traditional "send funds to a contract address" type of issuance model, but rather conducted through multiple centralized exchanges. This structure is quite rare in the crypto space. Haseeb, can you talk about the details in this regard? What innovations does this mechanism bring, and what issues does it have?

Haseeb Qureshi: This ICO indeed has many noteworthy design points. The main difference is that it was not conducted through a unified issuance platform, but rather used six centralized exchanges like Bybit, Gate.io, and Kraken. Each exchange received a portion of the token inventory to sell to its own users. These exchanges accessed the system through an API built by the Pump team, and when an exchange received user orders, it needed to request quota confirmation from the API in real-time, which would then return whether it could continue selling. This is essentially a collaborative inventory system.

The problem is that the Pump team completely underestimated the heat of this issuance. The API was almost immediately overwhelmed after the opening, responding very slowly, and even completely failing. Some exchanges, like Kraken, mistakenly thought they had received no quotas, so they oversubscribed user orders and later had to compensate users through airdrops. Bybit also had a similar situation, where they chose to give users $20 in trading credits as compensation.

Joe McCann: I heard that some users tried to successfully subscribe on Bybit while hedging short on Hyperliquid, but because the subscription failed, they ended up with only naked short positions, resulting in significant losses. This structure inherently carries many technical and game-theoretic risks.

Haseeb Qureshi: Indeed, this design was prepared for the "worst-case scenario." The Pump team initially worried that the project would not sell out and planned to sell it slowly over three days. They even consulted many VCs on how to design the fundraising structure, and everyone was concerned about the possibility of a failed auction, so the entire system was designed to ensure that exchanges could catch the project. The result was completely unexpected; demand far exceeded expectations, and on-chain bidding surged in an instant, overwhelming the API. This directly led to oversubscription by exchanges, uncontrolled distribution, and system chaos. However, in the long run, this distribution structure may be emulated by other projects, as these exchanges have already built the necessary infrastructure and may continue to use it in the future.

Laura Shin: It sounds like a new type of token issuance logic. I want to ask, is this mechanism more reliable than decentralized issuance methods? From the perspective of participant experience, what insights does this event bring?

Joe McCann: This reminds me of Hyperliquid's role. Although the token hasn’t officially launched, their price discovery before launch was very successful, with trading volume reaching $500 million. In contrast, companies like Circle had to constantly adjust their issuance prices and struggled to match orders during their IPO, which seems very outdated. Hyperliquid's performance indicates that on-chain capital formation + off-chain price discovery is a new collaborative mechanism. We have never seen this model in traditional finance, and this structure will be a significant breakthrough in the crypto financing market.

Haseeb Qureshi: One more point worth emphasizing: the capital formation method of this ICO is also very different. 75% of the funds were subscribed directly from on-chain wallets, many of which had investment amounts exceeding $1 million. These are clearly not ordinary retail investors but rather "smart money" that is very familiar with on-chain infrastructure and acts quickly. So this is not the traditional retail subscription model seen in traditional finance, but more like a collective action of Web3 native capital.

3. Investor Composition, Token Distribution, and Community Game Theory

Laura Shin: The token distribution of this ICO has also sparked considerable controversy. The official disclosure shows that 20% goes to the team, 13% to early investors, 33% to ICO participants, and the remaining 24% for the community ecosystem. However, many community members are dissatisfied with the low airdrop ratio, especially the creator airdrop of only 10 million tokens. Some comments point out that compared to Uniswap's 6.4 billion and Arbitrum's 12 billion, this number is too small. Joe, what do you think of these criticisms?

Joe McCann: In the crypto space, no matter how tokens are distributed, there will always be dissatisfaction. Founders have to face pressure from teams, investors, communities, and creators, and it’s impossible to make everyone happy. This is not an exact science; it’s more of a dynamic game. However, token distribution is indeed key to a project's success. Bonk is a great example. They prioritized broad distribution and now have over a million wallet holders, along with many practical products and strong user engagement.

I always advise founders to optimize the distribution mechanism to allow as many people as possible to obtain tokens, and then push for utility development. Did Pump.fun achieve that? It’s unclear at this point, but the token is still above the ICO price, indicating that the market still recognizes it.

Haseeb Qureshi: I want to add that the biggest difference between Pump and other projects is that it made no airdrop promises from the start, nor did it imply any. Users participated because they liked the product and the community, not for the airdrop. In other words, Pump has no "implicit social contract." Surprise airdrops like Uniswap are indeed wonderful, but Pump did not have such expectation management. From this perspective, any airdrop they do now is an extra benefit. Of course, the community will still complain, as complaining is incentivized in the crypto space. The cost is almost zero, and the potential gain could be huge. As long as you complain loudly enough, you might get a larger share of the airdrop. This has become a kind of game theory tactic.

Laura Shin: Indeed, many people use complaints to exert pressure. I also noticed that investors in this ICO do not have a lock-up period. Haseeb, does this mean that some institutions might sell immediately?

Haseeb Qureshi: Yes. Strictly speaking, the institutions participating in this ICO cannot be fully called "venture capitalists." The team’s initial plan was to focus on retail investors, with institutions as a supplement; this design was prepared for the "worst-case scenario." If retail demand was insufficient, institutions could fill the gap.

But in reality, retail demand far exceeded expectations, and institutions became the ones scrambling to buy. Many of them could not participate directly on-chain or on exchanges and had to buy OTC from the team, with terms the same as retail investors. So you could say they participated "on the same terms," but because there was no lock-up, there was no holding obligation. There is indeed some selling pressure in the market.

Joe McCann: I agree. And going back to our earlier discussion of "extreme capitalism vs community idealism," if an institutional investor takes on risk and chooses to exit after a 25% gain, that is completely reasonable. This is very common in traditional finance. For example, PIPE investors buy at a low price and quickly cash out when the stock rises. This is not a crypto-specific issue but rather a matter of investment logic itself.

Laura Shin: Let’s talk about who actually bought these tokens. Statistics show that about 8,200 people invested less than $1,000, while 200 invested over $1 million, with a total participation of about 13,000 people. There are even suspicions of "witch-hunt" style on-chain operations. At the same time, 24,000 people completed KYC. What does this indicate? Can we infer the investor profile of this ICO from this?

Haseeb Qureshi: These data indicate several things. First, on-chain funds dominate absolutely, with the tokens selling out in just 12 minutes. Many thought they had three days to participate, perhaps planning to come after breakfast, only to miss out. Furthermore, due to the strict KYC for this issuance, users from the U.S. and U.K. were completely excluded, with participants mainly from Asia or other regions. This also explains why retail investors were active while centralized exchanges frequently experienced mismatches.

Laura Shin: This issuance happened on a Saturday, which was quite suitable for U.S. time. But because of KYC, it’s not something that can be solved by VPNs.

Joe McCann: Exactly. For me, all of this reminds me of that "lightbulb moment" during the first ICO boom: we can actually complete global capital formation in just a few minutes. This model is redefining how companies raise funds. I do not agree with the notion that "centralized exchanges are dead"; CEX still has a powerful distribution network, with companies like Coinbase and Robinhood having tens of millions of KYC users. These networks will not disappear overnight, but we are indeed seeing an increase in on-chain participation, especially for projects like Pump that naturally embody the Web3 narrative.

4. Differences in Exchange Participation and Regulatory Trade-offs

Laura Shin: Another interesting point about this ICO is that Kraken participated in the token issuance, while Coinbase did not join at all. Why is there such a difference? What do you think of Kraken's decision and Coinbase's absence?

Haseeb Qureshi: Coinbase's absence is actually not surprising. They are a publicly traded company, deeply rooted in the U.S. market, and face greater regulatory constraints. In contrast, Kraken, while also regulated, primarily operates in Europe and is still a private company, giving it more flexibility. This may not only be a regulatory factor but also a brand consideration. If Coinbase supports the Pump ICO and then has to inform U.S. users that they cannot participate, it could confuse or disappoint them even more. So they might think, "Let’s just not participate to avoid trouble."

Joe McCann: Kraken's decision indeed demonstrates leadership. They are willing to take risks proactively to secure participation opportunities for users and chose to airdrop compensation when order issues arose, which is impressive. In comparison, the $20 credits given by Bybit seem a bit perfunctory. I also noticed that some users who originally tried to buy on Bybit hedged short on Hyperliquid to maintain market neutrality. But because they ultimately did not successfully buy in, they ended up with only naked short positions, leading to direct losses.

Haseeb Qureshi: This reflects the differences in infrastructure capabilities among exchanges. Established institutions like Kraken are more mature in dealing with emergencies; they realize that compensating customers is more important than saving money. Bybit, on the other hand, seems more focused on cost control as an emerging platform.

However, ultimately, this is not a big business for exchanges. Even platforms like Kraken might only sell a few tens of millions of dollars' worth of tokens. This money itself does not constitute a major source of income. Their willingness to participate is largely for user stickiness and brand recognition.

Laura Shin: So you believe exchanges will not treat this issuance model as a main business line in the future?

Haseeb Qureshi: Yes, this will not become a primary source of income. It’s more like a marketing event, similar to how FTX used to list many "junk coins" just to attract traffic. Token projects like Pump attract attention and bring users in, but the real money still comes from mainstream coins like BTC, ETH, and XRP.

Joe McCann: I agree. Moreover, Kraken's customer base leans more towards high-net-worth individuals, who actually care more about participating in these high-exposure new projects than retail investors. Even if they are fewer in number, they can bring in significant business volume, so Kraken is more willing to serve this group. In contrast, Coinbase's customers are primarily retail, making them more sensitive to compliance risks.

Haseeb Qureshi: And remember, Kraken is not yet publicly traded, which allows them to take on greater risks. Coinbase must be accountable to shareholders and cannot easily get too involved with meme coins or controversial projects. They know that Wall Street analysts do not want to hear about the company participating in projects like Pump—this would only bring negative perceptions. For Coinbase, the risk of association may far outweigh the short-term revenue it brings.

Laura Shin: But isn’t Kraken also preparing for an IPO?

Haseeb Qureshi: Yes, but they are not yet listed, which makes a significant difference in operational flexibility.

Joe McCann: One more detail worth noting: Coinbase actually launched Pump's perpetual contracts through its international platform. However, this product is not accessible to U.S. users. In other words, Coinbase is not completely uninvolved; they just did not participate in the ICO itself and did not promote it on their main platform. But they clearly recognize that this token has attention and are trying to participate in price discovery through other means.

Laura Shin: It’s indeed quite subtle. Coinbase promotes the vision of "on-chain future" through Base while deliberately avoiding the most attention-grabbing on-chain events. Is this duality part of their strategy?

Haseeb Qureshi: I think so. Coinbase has a positioning on Wall Street: they are the "decent representative of the crypto industry." They must maintain credibility in the traditional financial world, telling stories about Bitcoin as a macro asset, the tokenization of real assets, and ETF regulatory compliance. At the same time, they want to profit from retail trading, and these retail investors are indeed very interested in meme coins and on-chain activities. So they must walk a tightrope, maintaining a traditional financial image on the surface while trying to engage in on-chain excitement behind the scenes.

Joe McCann: I actually appreciate this strategy. We need people like Coinbase, who dress in suits to lobby in Washington D.C., but we also need teams that experiment on-chain and drive technological innovation. Both forces are necessary for the industry to move forward.

Laura Shin: Indeed, I also noticed that the a16z team is actively pushing policies in Washington. But projects like Pump, which are more "trench-style," clearly represent another path. Do you think these two routes can coexist?

Haseeb Qureshi: I believe they absolutely can. Coinbase and Base themselves embody this dual-track structure: one side is a serious, compliant public company, while the other is a chaotic on-chain experimental ground. If they can capture both worlds, it would be the best scenario for the entire industry.

5. Market Reaction and Competition: The Rise of Bonk and Community Diversion

Laura Shin: We are looking forward to what will emerge on Base, but I personally believe that Pump's ICO may trigger a new wave of ICO enthusiasm on Solana. Joe, you’ve previously echoed similar sentiments. Now I want to bring the topic back to trading performance: how do you see Pump's market cap or price trends in the coming months?

Haseeb Qureshi: First, let me clarify that this is not investment advice; I am neither an investor nor holding Pump. We are still in the early stages of price discovery because not all tokens have been distributed yet, and exchange listings are not comprehensive. Currently, the token is trading on a few platforms: I saw it trading on Bybit, KuCoin, and Pump's own Pump Swap today; among these, Pump Swap has the highest trading volume because most of the on-chain allocated people trade there. Typically, mainstream price discovery occurs on Binance, but it has not yet listed. Once Binance or other large exchanges go live, retail participation will increase.

On another note, some institutional investors who bought in during the ICO have not yet received their tokens, and many cannot use DEX. If they want to lock in profits (for example, securing ~25% initial gains), they need to wait for trading channels to open. Therefore, as more listings and token unlocks occur, short-term price fluctuations may be very large in the near future (over the next week or two) until positions are reconfigured.

Joe McCann: I don’t like to give specific price targets; that’s a Wall Street sales tactic. But I want to emphasize two points.

First, many people will try to backtrack token value using traditional fundamental models, which often does not work in crypto. You will see some protocols priced like cabbage fundamentally, yet the price remains stagnant.

Second, the core focus is attention. Tokens themselves are products, and whether people participate, discuss, trade, or speculate often drives price more than cash flow models. Pump claims to challenge platforms at the level of Twitch and TikTok and plans to integrate creator economies with crypto trading. If they can truly attract streamers, creators, and traders to interact, the attention will persist, and the token may benefit.

By the way, if Pump's fully diluted valuation (FDV) reaches the $5 billion to $10 billion range, we will need to reassess its relative valuation against competitors like Bonk, which has actually done a lot in terms of product, token distribution, and on-chain activities and may be undervalued.

Laura Shin: Speaking of Bonk, we see a phenomenon: the launch platform of the Bonk team, "Let's Bonk," also known as Bonk Fund, surpassed Pump.fun in 24-hour revenue for several days. As of earlier today, it is still leading. According to community data: over 1,200 tokens graduated from Bonk Fund, while Pump.fun is slightly above 600; the total number of tokens launched by Bonk Fund is about 130,000, while Pump.fun is about 77,000. Joe, why do you think this shift is occurring?

Joe McCann: I think the reason lies in sentiment and community positioning. People like Pump's product, but there has been a lot of negative narrative surrounding Pump recently: predatory, scams, exit scams, etc., even though these are often external behaviors of the platform. Bonk has a good reputation in the Solana community, seen as friendly, actively developing, and genuinely returning protocol revenue to the ecosystem by buying back and burning Bonk, etc. So when Pump sparked controversy, users naturally tried to issue or trade on the Bonk platform, leading to visible market share movement.

This is not necessarily a permanent migration; it could reverse next week. But we may be witnessing a competition between "community trust vs profit platforms." Pump has substantial cash flow; Bonk has deep community recognition. This will be healthy competition, but ultimately it may be a winner-takes-all scenario.

Laura Shin: I’ve checked out Let's Bonk, and the visual style of the meme coins there doesn’t seem as refined and Western as Pump's. Subjectively, it feels more Asian, with varying quality, while Pump appears more "neat." Do you think this cultural difference will affect users?

Joe McCann: Bonk has been deeply rooted in Southeast Asia for years, which may bring visual or cultural differences. But honestly, most meme traders do not care about image quality; they are looking for the next hundred-fold coin. Not to mention that a lot of funds participate through bot strategies, not even looking at the front-end interface.

Haseeb Qureshi: From a venture capital perspective, this is not surprising: when a dominant platform (like Pump) cools in sentiment and new creators find it hard to break through, it opens up space for competitive networks. Let's Bonk provides a new entry point and a different market atmosphere, naturally siphoning off some momentum. Additionally, it receives cross-subsidies from ecosystems like Raydium; while the scale may not be decisive, it does provide a boost.

I wouldn’t be bearish on Pump because of this. Don’t forget they just completed a massive financing round: they not only have hundreds of millions of dollars in cash on hand but also a large inventory of Solana assets and tokens. They can completely launch a market offensive using incentives, subsidies, buybacks, creator funds, etc., just like launching T-shirt cannons. I actually expect them to adopt a very aggressive counter-strategy.

6. Transition from Meme Coins to On-Chain Entertainment Financial Platforms

Laura Shin: I also noticed an interesting dynamic: Pump recently acquired Kolscan. This is a trading data analysis platform that can track addresses, hedging strategies, opening and closing operations on Hyperliquid in real-time. Does this mean Pump is building a closed-loop ecosystem? Are they not just trying to be a meme platform but have deeper ambitions?

Haseeb Qureshi: I think this is a very smart acquisition. Pump does not want to be just a meme platform; their goal seems more like to become the Twitch of the crypto space: integrating content creation, audience interaction, and financial speculation. Through Kolscan, they can analyze in real-time which on-chain traders have influence, who the hot topics are, and which coins are exploding. This helps Pump better incentivize creators and traders, pushing the most explosive content to the forefront. It’s not just a front-end product but a combination of a "trading engine + ranking recommendation system + incentive distribution system." You can think of it as a "financial version of TikTok + Twitch," but with a crypto-native narrative. This represents a completely new paradigm for the industry.

Joe McCann: I completely agree. Many people are still viewing Pump through the lens of traditional social platforms, thinking it’s just a meme coin incubator. But in reality, Pump aims to create an "attention-driven financial platform" that not only incubates coins but also controls trading flow, user perspectives, and community narratives. For example, Kolscan allows them to know who the KOL behind a coin is, whether there are bots washing trades, and who is driving buy orders; if Pump can use this data to adjust hot lists, rankings, and revenue distribution, they can "financially allocate" traffic. This is much more complex and powerful than the recommendation algorithms of ordinary social platforms.

Moreover, we see that traditional content platforms cannot establish a solid mechanism between user attention and content monetization. But crypto gives Pump a native incentive mechanism. You can not only watch content and interact but also place orders, buy in, and share profits. This model of trading as content is something traditional Web2 platforms cannot achieve.

Laura Shin: Do you think this direction will be the next stage of development for meme coins? They evolve from the original "image memes + community hype" into a hybrid of "financial games + native content + investment behavior"?

Haseeb Qureshi: Indeed, I believe that the next stage of meme coins will see more structured financial forms. Pump is just the first step; it proves that you can bring tens of millions of dollars in trading to a platform using a low-threshold, high-fun format. Next, we may see more systems like Pump, but perhaps not meme coins; they could be on-chain entertainment, on-chain gambling, AI-generated content markets, etc. Their commonality is that they arrange incentive structures around "attention + speculation." This is not merely about trading coins or just about Web2 creation; it’s a hybrid.

Joe McCann: To add a point: Pump also represents a return to "founder culture." In previous years, the meme craze on Solana leaned more towards anonymous culture, while Pump is clearly different; they have a very strong team that dares to advertise, take the stage, and play a paranoid and humorous style, yet can secure $500 million in financing and acquire tools while designing complex incentive models. This operation resembles a high-growth Web2 startup rather than a "DAO + community slowly governing."

I believe this route will attract more entrepreneurs to meme projects because you can quickly iterate using Web2 methods while leveraging the token model for significant leverage. This founder-driven meme project will become a new species.

Laura Shin: A very brilliant conclusion. Thank you for your analysis. Today we discussed a complete PUMP from financing structure, on-chain innovation, investor behavior, exchange game theory, to strategic future. Perhaps this is just the beginning of "meme 2.0."

Risk warning

Risk warning Risk warning

Risk warning