Hotcoin Research | Behind the Stablecoin Chain Explosion: The Responsibility, Risks, and Future of the Curator Model

The Curator model has rapidly expanded over the past year, with managed funds exceeding $10 billion at one point. Curators are widely distributed across mainstream lending protocols, which means that a single incident could transmit through Curators to the entire DeFi lending landscape.

The Curator model has rapidly expanded over the past year, with managed funds exceeding $10 billion at one point. Curators are widely distributed across mainstream lending protocols, which means that a single incident could transmit through Curators to the entire DeFi lending landscape.1. Introduction

Last week, the collapse of Stream Finance's xUSD triggered a chain reaction, leading to the decoupling of stablecoins such as deUSD and USDX. The DeFi sector witnessed a crisis of cascading stablecoin decoupling and a series of impacts on lending protocols, with the Curator model playing a role in exacerbating the situation, sparking market controversy and reflection.

The Curator model has rapidly expanded over the past year, with managed funds exceeding $10 billion at one point. Curators are widely distributed across mainstream lending protocols, meaning that a single failure can transmit through Curators to the entire DeFi lending landscape. The recent stablecoin decoupling incident confirmed this: xUSD -> deUSD -> USDX resembled a domino effect, breaching the defenses of multiple protocols. This series of failures not only accelerated capital flight but also shook investor confidence in the Curator model, prompting the industry to reflect: does the Curator model reduce risk, or does it concentrate and amplify risk?

This article will delve into the role and function of Curators in on-chain lending protocols, their profit models, and review leading Curators, including their backgrounds, styles, fund sizes, and performances during this incident. It will also expose the risks and challenges of the Curator model revealed by this stablecoin decoupling event, and look ahead to the future evolution of the Curator model and the lending market, aiming to provide comprehensive insights for investors.

2. The Role and Function of Curators

A Curator refers to an external fund pool manager within DeFi lending protocols. They are responsible for designing, deploying, and operating specific strategic fund pools (Vaults), encapsulating complex DeFi yield strategies into products that ordinary users can deposit with a single click. For example, in emerging lending protocols like Morpho and Euler, users can choose different Vaults provided by Curators, who then determine investment strategies on the backend, including asset allocation weights, risk management, rebalancing cycles, and withdrawal rules. Unlike traditional centralized wealth management, Curators cannot directly misappropriate user funds; their authority is limited to executing strategies through smart contract interfaces, and all operations are subject to contract security constraints.

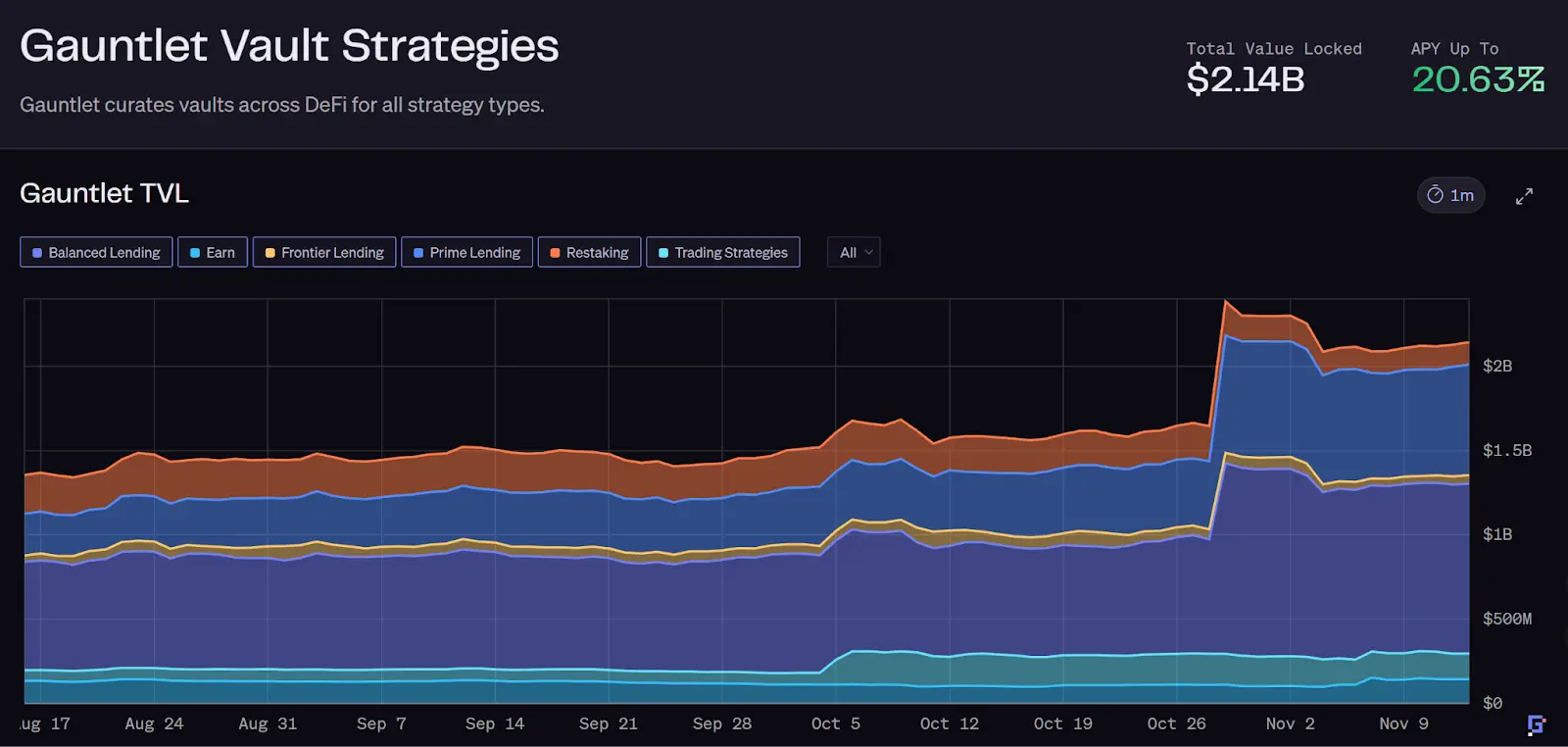

The initial intention of introducing the Curator model was to leverage the strategic management and risk control capabilities of these professional teams to bridge the supply-demand mismatch in the lending market. On one hand, it helps ordinary users achieve higher returns in an increasingly complex DeFi world; on the other hand, it assists lending protocols in increasing TVL and reducing the probability of systemic risk events. Since Vaults managed by Curators often provide higher yields than traditional lending pools (like Aave), they can attract significant capital. According to DefiLlama data, the scale of Curator model fund pools has rapidly grown, surpassing $10 billion in early November 2025. Currently, due to panic, it has decreased to about $7 billion, indicating that some funds are withdrawing from this model.

Source: https://defillama.com/protocols/risk-curators

In this "Curator" model, the lending protocol itself becomes a matching platform, outsourcing risk control and fund allocation functions to Curator teams, which are vividly likened to "fund managers in the DeFi world." This means that over $8 billion in funds are effectively managed by numerous Curators with diverse backgrounds. On the surface, it seems that professionals are doing professional work, making it easy for users to achieve high returns; however, at the same time, risk has shifted from code to human management, making human factors an unavoidable source of risk.

3. Curator Profit Model

To understand the risks inherent in the Curator model, one must first grasp its profit logic. Typically, Curators' income sources include:

Performance Fee: After strategy profits, a certain percentage is taken from net earnings, which is the primary form of income. For example, the USDT Vault managed by Gauntlet on Morpho charges a 5% profit share.

Management Fee: A management fee is charged based on a certain annualized percentage of the total assets in the fund pool (similar to traditional fund management fees).

Protocol Incentives: Lending protocol parties may offer token rewards to Curators to encourage them to create high-quality strategies, such as subsidies for early introduction of new strategies.

Brand Derivative Income: Once Curators gain recognition, they may also issue their own products or even tokens for profit.

In short, the larger the Vault size and the higher the strategy yield, the more profit Curators can obtain. In fierce competition, no Curator dares to arbitrarily raise the commission rate to grab profits, as users are more concerned about the APY. Therefore, to attract funds, Curators often strive to increase the nominal yield of strategies, leading to yield-driven competition.

This incentive mechanism contains obvious moral hazards: Curators earn excess profits, but losses are borne by users. Driven by the internalization of profits and externalization of risks, Curators inevitably seek higher yields, which equate to higher risks, making safety easily overlooked. When most deposit users only focus on yield numbers without understanding strategy details, this tendency becomes even more dangerous.

4. Review of Leading Curators

Currently, a number of leading professional Curator institutions have emerged in the DeFi lending space, managing assets worth hundreds of millions. Below is a review of representative leading Curators, each with distinct team backgrounds, management scales, risk control styles, and profit methods:

1. Gauntlet

Source: https://app.gauntlet.xyz/

Founded in 2018 by Tarun Chitra and other quantitative finance experts, Gauntlet is one of the earliest teams deeply engaged in DeFi risk management. Gauntlet is known for its data-driven risk assessment and management, having provided parameter optimization services for Aave, Compound, and others. In the Curator model, Gauntlet emphasizes robust risk control, continuously calibrating strategy parameters and compliance audits through an automated quantitative platform. Its Vaults have a total locked value exceeding $2 billion, covering multiple chains such as Ethereum, Base, and Solana. Gauntlet's income mainly comes from management fees (charged annually), with annual management fee income estimated at about $7.2 million.

Gauntlet's model is closer to "risk control consultant + Curator." During the recent deUSD decoupling, Gauntlet assisted Compound in urgently freezing withdrawals to stop losses, doing so three hours ahead of manual operations, reducing losses by approximately $120 million. This demonstrates its professional and rapid risk control response.

2. Steakhouse Financial

Source: https://www.steakhouse.financial/

Founded in 2020, Steakhouse has promoted the introduction of U.S. Treasury bonds and private credit onto the blockchain through MakerDAO, aiding the development of RWA tokenization. It utilizes Morpho's infrastructure to dynamically allocate and rebalance funds across various lending pools based on different market yield conditions, creating institution-level robust yield strategies. Steakhouse excels in detailed interest rate risk analysis and portfolio optimization, focusing on stablecoin yield spreads and staking returns. Currently, Steakhouse manages 48 Vaults across chains such as Ethereum, Base, and Polygon, with a fund management scale of about $1.5 billion. Its clients include institutions like Coinbase, Lido, and Ethena, helping them design stablecoin yield products.

In the xUSD incident, Steakhouse completely avoided this risk exposure and did not invest user funds into high-risk projects like Stream xUSD, reflecting its cautious style. Overall, Steakhouse is known for its stability, striving for solid returns while ensuring safety.

3. MEV Capital

Source: https://www.mevcapital.com/

A Curator known for its DeFi quantitative hedging strategies, MEV Capital managed assets peaking at nearly $1 billion, which have now decreased to $400 million. The team consists of traditional hedge fund and on-chain arbitrage experts, skilled in enhancing returns using MEV and other means. MEV Capital excels in using over-the-counter options hedging strategies combined with cyclical lending to improve capital utilization. In extreme market conditions, this high-leverage design accelerated failures.

MEV Capital became a focal point during the Stream incident: as a core cooperative Curator introduced by the Stream protocol, its business was deeply involved in the xUSD strategy. The two parties were closely bound by an agreement of "strategy licensing - fund custody - profit sharing." Currently, MEV Capital's TVL on Morpho has rapidly declined, with some pools' TVL being only one-tenth of peak levels. MEV Capital recently began "bad debt liquidation" for some stablecoins, handling it in a manner that spreads losses among depositors.

It is evident that MEV Capital's style is aggressive, willing to introduce complex derivatives and high leverage in pursuit of high returns, with a high risk tolerance. Additionally, its profit-sharing arrangement with Stream has sparked controversy among users.

4. K3 Capital

Source: https://www.k3.capital/

A Curator positioned for institutional compliance, K3 emphasizes providing safe and transparent on-chain asset allocation services for institutions and high-net-worth individuals. K3 manages approximately $570 million in funds. K3 has a close partnership with the Gearbox protocol, having utilized Gearbox's "pool-to-account" model to launch a customized USDT credit market, allowing users to borrow up to 10 times leverage against USDT collateral, investing in DeFi strategies like Ethena, Sky, and Pendle for returns. Through this approach, some of K3's Vaults provide users with stable annual returns of 8%-12%. In terms of risk control, K3 tends to prefer basis arbitrage while avoiding excessive nested risks.

In this round of failures, K3 was also unable to escape: it invested part of its Vault managed on the Euler platform in the stablecoin deUSD issued by the Elixir protocol. After the Stream collapse on November 3, K3 negotiated with the Elixir founder for a 1:1 redemption of deUSD but was met with avoidance. Unable to do otherwise, K3 sold off deUSD for liquidation on November 4, but still had $2 million that could not be redeemed, resulting in losses. Subsequently, Elixir officially announced bankruptcy, promising that retail investors and liquidity pools could redeem deUSD at a 1:1 ratio for USDC, but the deUSD held by the Curator Vault would not be redeemed, requiring separate negotiations. K3 has hired top lawyers in the U.S. and plans to sue Elixir and its founder Philip Forte for breach of contract and false statements, seeking compensation for reputational damage and forced redemption of deUSD.

5. Re7 Labs

Source: https://defillama.com/protocol/re7-labs?events=false

A rising Curator, Re7 Labs found itself at the center of the storm alongside MEV Capital during this incident. Re7 managed assets peaking at about $900 million, which have now decreased to $250 million. As one of the top Curator partners on the Stream platform, Re7 once controlled over 25% of Stream's total locked value (approximately $125 million). However, its investment configuration was aggressive: it was disclosed that Re7 invested $65 million into Balancer's non-insurance pool for liquidity mining, $40 million into emerging chain mining, and $20 million into off-chain perpetual contracts, speculating with up to 10 times leverage. All three directions belong to high-risk, high-reward areas.

After Balancer encountered a security incident that indirectly triggered the xUSD collapse in early November, Re7 and MEV faced issues in other protocols' Vaults: the lending vaults operated by both on the Lista DAO platform were drained using sUSDX/USDX collateral loans, leading to a utilization rate of 99% and borrowing rates soaring to over 800%, triggering forced liquidation mechanisms. It can be said that Re7 Labs' operations reflect the most aggressive side of the Curator model: highly concentrated risk exposure combined with multiple layers of high leverage. Re7 is now also mired in loss and reputational crisis, with its published decoupling impact report indicating over $13 million in affected funds.

It is evident that during this stablecoin decoupling crisis, different Curators exhibited vastly different styles and outcomes: some Curators heavily invested in high-risk assets and ultimately faced disaster, while others adhered to risk control bottom lines and successfully avoided catastrophe. This proves that professional Curators are not incapable of identifying and avoiding risks; the key lies in self-discipline and restraint.

5. Risks and Challenges of the Curator Model

In summary, the Curator model has exposed multiple inherent challenges during this incident:

Incentive Misalignment and Excessive Profit-Seeking: The performance-based profit model drives Curators to pursue high-yield strategies, leading to increased risk appetite. When profits come from high-risk investments while losses are borne by users, Curators lack sufficient motivation to prioritize safety, easily giving rise to moral hazards. Curators may take risks for profits, ignoring the possibility of black swan events.

Lack of Transparency: Many Curator strategies operate as black boxes, with serious disclosure deficiencies. Users often only see vague strategy descriptions and historical return curves, while being completely unaware of core risk information such as underlying holdings, leverage ratios, and liquidation mechanisms. For example, after the Stream incident, users discovered that MEV Capital had actual leverage as high as 5 times, with xUSD having only $170 million in assets but borrowing $530 million. Overall, the lack of transparency is one of the biggest hidden dangers of the current Curator model.

Risk Concentration and Domino Effect: Under the Curator model, a few Curators often control the majority of funds. Once these Curators simultaneously step into the same pit, the consequences can be dire. For instance, before the Stream collapse, MEV and Re7 managed 85% of its funds and heavily invested in the same protocol, leading to batch failures and bad debts. Additionally, Curator cross-protocol activities themselves become conduits for risk transmission: Vaults are interconnected through common assets and leverage chains, forming a domino effect. Furthermore, some Curators have highly similar strategies, exacerbating the impact of single-point failures. Therefore, the lack of independent strategies and highly overlapping positions is a problem that the Curator field needs to be wary of.

User Awareness and Responsibility Definition: Many deposit users do not truly understand the existence and role of Curators, mistakenly equating Vault risks with protocol risks. If a Curator encounters issues, the protocol party has to "take the blame," facing pressure from rights protection and public opinion. This time, Euler faced huge bad debts caused by Curators, leading users to question Euler's safety; the suspension of withdrawals from Morpho Vault also impacted its reputation. This ambiguity of responsibility further leads some Curators to act recklessly in pursuit of profits.

Technical and Liquidation Mechanisms: Curator strategies are often complex and cross-protocol, sometimes challenging the timeliness and effectiveness of existing liquidation mechanisms. For example, Morpho experienced a situation where Vault utilization reached 100%, making timely liquidation impossible, resulting in $700,000 in bad debts, forcing a suspension of some on-chain operations. Complex strategies lengthen the liquidation chain, and in extreme market conditions, technical execution may fail.

In summary, this stablecoin decoupling chain event has sounded the alarm, as the Curator model has reintroduced previously dispersed human risks into DeFi, concentrating and amplifying many issues of traditional finance: information asymmetry, moral hazard, concentration risk, and regulatory gaps.

6. Improvements and Future Outlook for the Curator Model

In response to the aforementioned challenges, various industry parties are exploring paths to improve the Curator model to rebuild trust and harness its positive value:

Self-discipline and capability enhancement of Curators are crucial: Excellent Curators should possess compliance awareness from traditional finance and comprehensive risk management capabilities, including portfolio risk assessment, understanding of oracles and contracts, market monitoring, and smart rebalancing. Curators should also abandon short-sighted gambling mindsets, focusing more on long-term stable returns and prioritizing user interests. Transparency is also a part of self-discipline: Curators have a responsibility to proactively disclose key information such as strategy structure, collateral composition, leverage ratios, and liquidation rules for external review and verification. This not only protects users but also safeguards Curators from false accusations. Future Curators must establish "high transparency standards" to expose hidden risks to the light.

Users should cautiously evaluate and select Curators: Before investing in a Vault, pay more attention to the Curator team's reputation, publicly available risk models or stress test reports, whether they have been audited, how they performed during extreme market conditions, and whether the incentive mechanisms align with users. It is especially important to remember the iron rule that high returns correspond to high risks, and to stay away from claims of "double-digit risk-free returns." Ordinary investors may not have the energy to delve into every Vault detail, but they can at least use community discussions and third-party data to assist in their judgment.

Protocol layers need to strengthen supervision and constraints on Curators: Lending protocols should not blindly allow Curators to increase TVL but should take on a basic "regulator" role. Specific measures include: requiring Curators to publicly release risk models and regular reports, allowing protocols to independently verify strategy data; introducing staking and penalty mechanisms, requiring Curators to lock a certain margin, which would be proportionally forfeited in case of significant violations or losses; establishing Curator admission and replacement systems, regularly evaluating Curator performance, and replacing those who perform poorly or are overly aggressive, forming continuous external supervision to avoid systemic resonance risks. It is expected that future protocols will impose stricter contractual restrictions and governance clauses when introducing Curators to prevent similar events from recurring.

Looking ahead, modular, composable but mutually isolated lending strategies may become a trend. The Curator model has indeed enhanced yields, enriched strategy categories, and attracted institutional participation in DeFi. However, to make Curators a positive force for the long-term prosperity of DeFi, it is essential to design mechanisms that leverage strengths and avoid weaknesses, integrating the flexibility of Curators into a proven liquidation and governance framework while maintaining the unity and safety of underlying fund pools. Perhaps in the near future, Curators will evolve into controlled modular plugins, allowing various service providers and integrators to build specific strategies within a mature protocol ecosystem. At that time, the Curator model will shed its phase of barbaric growth and enter a regulated and secure new era.

Conclusion

After experiencing this series of stablecoin collapses, the Curator model in DeFi lending has entered a profound reflection and adjustment opportunity. In just a few days, the TVL of Curator Vaults evaporated by about 25%. However, amidst the burst of the bubble, more mature mechanism innovations are poised to emerge. The Curator model has the potential to undergo a phoenix-like rebirth—under transparency, accountability, and structural optimization, becoming a key component in the DeFi ecosystem that enhances yields while safeguarding security. We have already seen some positive signs: some Curators are strengthening information disclosure, lending protocols are exploring the introduction of staking accountability mechanisms, and leading projects like Aave are providing new ideas for modular isolation. These efforts are expected to reshape user confidence, and through collaborative efforts, the Curator model could very well transform into one of the cornerstones of DeFi innovation.

About Us

Hotcoin Research, as the core investment research institution of Hotcoin Exchange, is dedicated to transforming professional analysis into your practical tools. Through our "Weekly Insights" and "In-Depth Reports," we analyze market trends for you; leveraging our exclusive column "Hotcoin Selection" (AI + expert dual screening), we help you identify potential assets and reduce trial-and-error costs. Every week, our researchers also engage with you through live broadcasts, interpreting hot topics and predicting trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and seize value opportunities in Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investment itself carries risks. We strongly advise investors to invest only after fully understanding these risks and within a strict risk management framework to ensure the safety of their funds.

Risk warning Risk warning

Risk warning Risk warning

Popular articles