Where is the last mile for stablecoins?

As technology continues to evolve, stablecoins are given a grand mission: to become an efficient and low-cost payment tool.

As technology continues to evolve, stablecoins are given a grand mission: to become an efficient and low-cost payment tool.As technology continues to evolve, stablecoins have been given a grand mission: to become efficient and low-cost payment tools.

Data shows that the number of stablecoin wallets is continuously increasing, and the number of transactions is also on the rise. However, the number of people who truly use stablecoins as "everyday payment tools" has not shown a proportional increase. According to the Where Are Stablecoins Being Spent report, most stablecoin activities are still concentrated in capital flows, trading, and DeFi scenarios, with retail transactions accounting for less than 5% of global stablecoin usage.

Although this percentage is slowly rising, overall, it is still a significant distance from becoming a large-scale, everyday payment tool. If technology, capital, and narrative are already in place, then where exactly is the "last mile" of stablecoins stuck?

1. From "having a wallet" to "being able to use it," there are three real barriers in between

The popularity of stablecoins is not just a technical issue; it also includes practical barriers to usability.

1. User Barriers: Having a wallet ≠ Knowing how to use money

For many users in emerging markets, the exposure to stablecoins often begins in a very passive scenario: receiving a transfer of USDT or USDC, or using it as an alternative asset for "hedging." However, moving from "having" to "using" requires overcoming many obstacles:

Wallet operations are complex; managing private keys, selecting networks, and dealing with Gas fees are high barriers.

Lack of trust; concerns about operational errors or fraud.

No clear usage path: After receiving stablecoins, what can be done? Where can they be spent?

As a result, stablecoins have become a "digital cash storage" in many places, rather than a truly circulating "currency."

2. Merchant Barriers: Accepting stablecoins does not equal good business

From a merchant's perspective, their concerns are never about "technological advancement," but rather more direct issues:

After accepting stablecoins, how do they pay rent, employee salaries, and utility costs?

How to record transactions? How to account for them? How to handle taxes?

If they need to convert to local currency, are the channels stable, transparent, and compliant?

Even if merchants have an open attitude towards stablecoins, they still prefer to use familiar card organization channels and local payment networks to ensure stable and predictable operations.

3. Regulatory Barriers: The issue is not "whether to allow," but "how to regulate"

In the eyes of regulators, stablecoins are not a romantic technological concept, but involve:

Anti-Money Laundering (AML)

Capital flow control

Foreign exchange management

Consumer protection

Data review and cross-border compliance

For many countries, the real issue has never been "whether to allow stablecoins," but rather: how to incorporate this new tool into the regulatory framework without compromising the safety of the existing financial system? At this stage, any product that is "outside the system" will become the biggest obstacle to large-scale adoption.

2. The "last mile" of stablecoins is not necessarily on-chain

A common misconception is that many believe the next step in the popularization of stablecoins depends on better blockchains, faster TPS, or lower Gas fees. But the reality is: from a technical perspective, blockchains are already ready. What is truly missing is another dimension: how stablecoins can naturally integrate into existing financial and payment systems. This includes:

Banking account systems

Card organization networks (Visa / Mastercard)

Merchant acquiring systems

Corporate financial systems

Compliance, risk control, and clearing networks

In the daily lives of ordinary users, people do not want to learn a new financial system; they just want to continue using familiar methods to consume, pay, transfer, and operate. This precisely indicates that for stablecoins to truly achieve widespread adoption, they need to be "invisible" to users.

Users do not need to know whether they are using Web3, Web2, or blockchain. They just need to know: "This method is usable, faster, cheaper, and safer."

3. Real change comes from the reconstruction of the "intermediate layer"

In the past two years, the key to the real implementation of stablecoins has not been the on-chain technology itself, but rather how to connect underlying assets, payment channels, and compliance capabilities into a usable real payment system.

Infrastructure / Rail Layer: On-chain stablecoins, exchanges, and settlement networks form the foundation of capital flow.

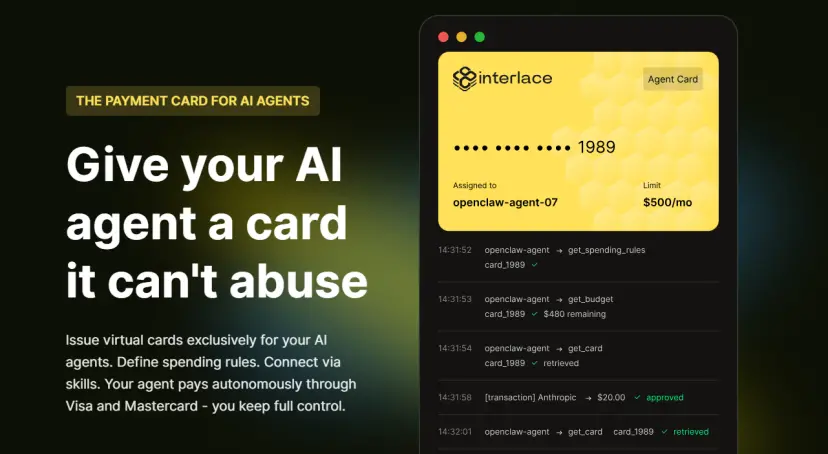

Orchestration Layer: Provides compliance, clearing, fund transparency, and API interface capabilities, serving as the core support of the entire ecosystem. Innovative financial platforms like Interlace offer comprehensive solutions for global accounts, card issuance, currency exchange, embedded compliance risk control, and unified APIs, helping enterprises efficiently manage capital flows in multi-currency and multi-region environments.

Application / User Layer: Daily scenarios such as corporate payments, retail collections, and cross-border settlements allow users and enterprises to use stablecoins without awareness.

The map illustrates the capability layering of the current stablecoin ecosystem, but having only the orchestration capability in the intermediate layer is not enough to enable users and enterprises to truly "use" stablecoins. Between on-chain capabilities and the real world, there still needs to be a perceivable, operable, and embeddable product form, such as U-cards, that transforms underlying stablecoin assets and intermediate layer capabilities of accounts, clearing, and compliance into payment methods that users can directly use, such as:

Corporate daily expenses: Directly pay for advertising, SaaS subscriptions, logistics, and storage costs without manual conversion or operating on-chain assets.

Employee reimbursements and travel payments: Employees can use cards or embedded wallets for expenses related to business trips, office purchases, transportation, and accommodation, simplifying the reimbursement process.

Retail and merchant consumption: Individual users or small merchants can use U-cards for daily consumption without needing to understand blockchain or the underlying technology of stablecoins.

In this process, enterprises and users hardly need to perceive the technical details; their payment experience is similar to traditional financial tools while simultaneously enjoying the efficiency and settlement advantages brought by stablecoins. This is precisely the embodiment of the "stablecoin sandwich structure": funds are settled and circulated on-chain, but the entry and exit points for usage remain within the fiat currency system, i.e., fiat currency → stablecoin → fiat currency.

It is this structure that allows stablecoins to move beyond the realm of crypto assets and naturally integrate into corporate cash flows, personal consumption, and cross-border business activities: the upper layer experience allows users to use it without awareness, the intermediate layer ensures the safety and compliant circulation of funds, and the lower layer provides stable assets and settlement capabilities.

Before full-chain payments become widespread, it is the existence of such "bridge-type infrastructure" that drives the evolution of stablecoins from on-chain assets to real payment tools, truly completing their "last mile" implementation.

Risk warning Risk warning

Risk warning Risk warning