The Hub of Cross-Chain Economy: How Does Folks Finance Integrate a Unified Financial Network Through Cross-Chain Lending?

The next phase of DeFi will ultimately be defined by protocols that can weave chains into a network.

The next phase of DeFi will ultimately be defined by protocols that can weave chains into a network.Data Statement: All token prices, FDV values, and on-chain metrics referenced in this report are based on market data as of December 1, 2025.

TL;DR

Transition from "Multi-chain" to "Cross-chain": Folks Finance has achieved true cross-chain lending through a Hub-Spoke architecture, rather than simple multi-chain deployment. The core lies in transmitting state instructions across chains rather than the assets themselves, allowing collateral, debt, and liquidation risks to be managed uniformly on the central chain. Users can collateralize on Chain A and borrow on Chain B, breaking the liquidity islands between chains.

Unlocking cross-chain capital efficiency for high and stable yields: By constructing a globally unified liquidity pool that aggregates supply and demand from all connected chains, interest rates for the same asset are consistent across chains. Funds can be automatically directed to chains with higher interest rates, resulting in a structurally higher APY.

Building a multi-tiered financial infrastructure to form a complete ecological loop: Centered around cross-chain lending, Folks Finance has expanded into liquid staking, a DEX router that aggregates cross-chain liquidity, and Ultraswap, which optimizes liquidity for niche trading pairs, collectively forming a complete product matrix capable of supporting complex strategies and enhancing capital recyclability.

Valuation has upward potential, and structural advantages have yet to be fully realized: The current FDV is approximately $400-450 million, placing it at the industry median. However, its unique cross-chain lending mechanism, comprehensive ecological layout, and first-mover advantage in unified liquidity provide significant growth elasticity in terms of TVL, revenue, and valuation, with value expected to increase as cross-chain network effects become apparent.

1. Is it "Multi-chain" or "Cross-chain"? Why does DeFi lending still suffer from liquidity islands?

In an era of narrative inflation, hot topic rotation, and rapid project iteration, every wave of cleansing in the crypto industry is reshaping the landscape. Few sectors have managed to maintain a stable foothold after multiple rounds of reshuffling, and DeFi lending is one of the few segments that has consistently demonstrated resilience through cycles.

Lending is not only one of the earliest validated models in DeFi but also serves as the infrastructure and liquidity hub of the entire on-chain financial system: liquidity pools provide the underlying liquidity for stablecoin minting, leverage strategies, derivatives, and cross-chain assets, acting as the key engine driving the entire ecosystem.

As DeFi matures, lending protocols are expected to meet higher expectations—not only to be safer and more efficient but also to genuinely accommodate the growing liquidity demands of a multi-chain ecosystem. In recent years, the number of public chains has surged, and users have dispersed across different ecosystems, creating natural divides between chains. Capital struggles to flow across chains, leading to declining liquidity efficiency and preventing the overall TVL of the lending market from being fully activated.

In recent years, various solutions claiming to have "achieved cross-chain lending" have emerged, but these solutions essentially remain at the level of multi-chain lending rather than true cross-chain lending.

Most so-called "cross-chain lending" is merely an improvement at the user experience level:

They only provide asset-level cross-chain migration without achieving cross-chain unification of core states such as collateral, debt, interest rates, and liquidation risks at the smart contract level. Protocols operate independently on different chains, forming isolated liquidity pools, independent risk parameters, independent liquidation systems, and independent user positions, meaning liquidity has never truly been consolidated.

As a result, deposits on one chain cannot serve as a source for borrowing on another chain, and multi-chain liquidity remains fragmented, which is far from true cross-chain lending. True cross-chain lending requires:

Liquidity across different chains to be directly shared;

Collateral deposited on one chain to generate borrowing capacity on another chain;

Users' risk exposure to be managed uniformly across chains, rather than being fragmented into multiple isolated accounts.

If such a future is realized, it will become a key turning point for unlocking DeFi lending liquidity, allowing on-chain finance to transition from "multi-island" to a "unified network": assets, collateral, risks, and borrowing demands across different chains will operate collaboratively within a unified system.

This is precisely the new solution offered by Folks Finance: it addresses the user experience issues faced by DeFi in the multi-chain era and achieves cross-chain "capital liquidity integration" at the protocol level, laying the foundation for a truly cross-chain financial network.

2. Technological Innovation: What Solutions Does Folks Finance Bring?

2.1 Hub-Spoke Cross-chain Lending as a Replacement for Multi-chain Lending Solutions

Folks Finance's current cross-chain architecture has integrated with multiple mainstream blockchains, as shown in the diagram, including Avalanche, Monad, Sei, Arbitrum, Base, Ethereum, BSC, Monad, and the Polygon ecosystem. It achieves cross-chain interoperability through the integration of messaging layers such as Wormhole, Chainlink CCIP, and Circle CCTP.

|--------|---------------------------|--------------------------------------| | Comparison Dimension | Multi-chain Lending | Hub & Spoke Cross-chain Lending | | Overall Architecture | Each chain independently deploys a complete protocol | Hub is responsible for storing all lending function states | | State Management | State fragmentation: each chain independently manages collateral, debt, interest rates, HF | Unified state: collateral, debt, risks, and liquidation are all managed uniformly in the Hub | | Collateral Reuse | Collateral can only be used on the same chain | Users can collateralize on Chain A and borrow on Chain B | | Liquidation Logic | Independent liquidation on each chain | Liquidation is uniformly handled on the central chain (Hub) | | Cross-chain Interaction Method | Transfer of aToken quantity through burn/mint between chains | Spoke chains are responsible for sending cross-chain messages, and all lending-related states are updated uniformly by the Hub chain | | User Experience | Multi-chain operations are complex, hard to manage, and cross-chain lending is unfeasible | One account enables multi-chain access and true cross-chain lending |

2.1.1 Technical Implementation

In Folks Finance's cross-chain architecture, when a user initiates an operation on a connected chain, the contract on that chain generates a corresponding instruction message and sends it to the hub chain, which acts as the "hub" via cross-chain messaging protocols like Wormhole and Chainlink CCIP. The hub chain serves as the single source of truth for the protocol's state, executing the corresponding lending or liquidation logic upon receiving the message, and triggering fund transfers or position updates on other chains as needed; each connected chain retains only the minimal state related to communication, maintaining consistency with the hub through message exchanges.

In simple terms, the entire process is essentially on-chain message passing + unified execution on the central chain: users do not need to manually bridge assets or handle traditional cross-chain bridge processes such as locking, minting, or redeeming, allowing them to complete one-time lending and position adjustments across multiple chains seamlessly.

2.1.2 Cross-chain Capital Efficiency

Unlike standard multi-chain lending platforms with dispersed and independent liquidity, Folks Finance achieves the integration of cross-network capital.

Multi-chain protocols have multiple isolated protocol copies, so deposits on one protocol cannot be borrowed from another; however, "cross-chain" protocols are different—regardless of which chain users are on, liquidity is available. This makes "cross-chain" protocols more capital-efficient than "multi-chain" protocols.

- Cross-chain transmission of state instructions

Cross-chain communication transmits "state instructions" rather than the assets themselves, allowing lending states to be managed uniformly in the Hub. This provides the foundation for unified liquidity and cross-chain lending.

- Cross-chain collateral reuse

Collateral only needs to be deposited on one chain to enable borrowing on another chain, eliminating the need for bridging, asset transfers, or waiting for cross-chain bridge confirmations. This results in faster transaction speeds, higher security, and more flexible capital turnover.

As more chains connect, the platform continuously expands the coverage of cross-chain lending, significantly enhancing the availability, efficiency, and utilization of capital.

This approach not only unlocks the dormant liquidity on edge chains but also enables seamless capital flow between different ecosystems—users do not need to switch interfaces or rely on external tools, resulting in a smoother overall experience and lower transaction friction costs.

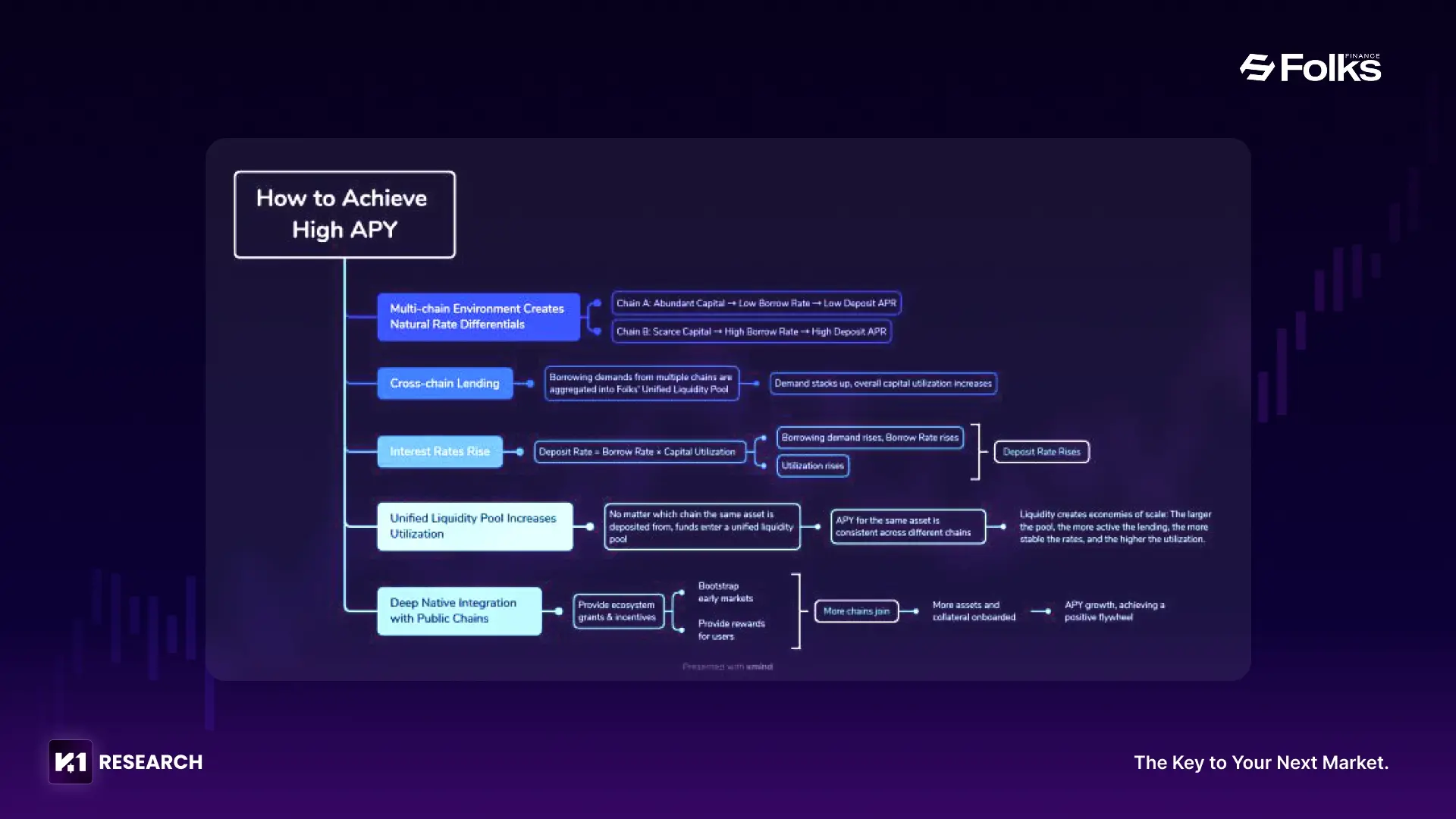

2.2 High APY Formation Logic

Because Folks Finance adopts a cross-chain unified liquidity pool structure, funds deposited in the same asset from any chain ultimately flow into the same globally shared liquidity pool. This means that the interest rate model, borrowing utilization rate, and interest distribution mechanism are all calculated and updated uniformly by the central Hub.

As a result, the APY for the same asset across different chains will not deviate but will be consistent and fully unified across chains.

The traditional multi-chain lending model stands in stark contrast to Folks Finance's cross-chain unified liquidity pool. In the traditional architecture, each chain corresponds to an independent liquidity pool, and supply-demand relationships are completely isolated, leading to significant discrepancies in APY for the same asset across different chains. Users, in pursuit of higher yields, are forced to compare and migrate funds across multiple chains. This process is fraught with friction costs and execution risks, making it difficult for users to truly capture returns.

In contrast, Folks Finance's cross-chain unified pool mechanism aggregates supply and demand from all chains, ensuring consistency in interest rates and achieving economies of scale in liquidity.

At the same time, Folks Finance's high APY not only stems from the increased utilization of the unified liquidity pool but also benefits from its deep native integration with multiple public chains.

As the protocol expands to multiple ecosystems such as Avalanche, Arbitrum, Polygon, and Sei, these chains are offering ecosystem grants and incentives to accelerate cross-chain liquidity growth and expand the lending market scale, thereby providing rewards for early market participants and lending and deposit users.

These ecosystem incentives have significantly boosted deposit APY in the early stages, rapidly increasing the scale of the cross-chain unified liquidity pool.

As more chains join and more assets and collateral are onboarded, these incentives further drive capital inflows across the entire chain, creating a positive feedback loop for APY based on structural foundations.

Cross-chain lending expands the available range of capital, allowing the previously dispersed supply and demand across different chains to be unified and coordinated.

When a particular chain experiences higher borrowing demand or better interest rates, idle funds from other chains can immediately fill the gap, allowing overall capital to continue operating within higher yield ranges. Compared to traditional lending protocols that can only rely on supply and demand from their own chains, this cross-chain scheduling allows Folks to achieve inherently higher utilization rates and makes it less susceptible to interest rate declines due to single-chain cyclical changes.

Thus, Folks' APY exhibits characteristics of being "higher and more stable": high, because capital can flow across chains and be directed to higher interest rate scenarios; stable, because the supply-side structure is more robust and less prone to short-term emotional disturbances affecting the overall protocol.

2.3 Deeply Integrated Ecosystem

Folks Finance's Hub-Spoke architecture centralizes all core risk assessments on the central chain, while the spoke chains only execute operations, structurally reducing risk sources from oracles, liquidations, and cross-chain communications. This architecture inherently provides higher systemic security and offers a unified interface for ecological collaboration.

Oracle Integration

The central chain uses Chainlink and Pyth to provide price data, eliminating the need for spoke chains to deploy oracles, significantly shortening risk pathways and reducing potential erroneous liquidation risks caused by multi-chain synchronization.Stablecoin Infrastructure

Native integration with Circle ensures that USDC maintains consistency in a multi-chain environment, reducing additional credit risks associated with cross-chain wrapped stablecoins.Protocol-level Security

Folks Finance has indicated that the protocol has undergone audits by over ten institutions, including Trail of Bits, Certik, and OtterSec. Additionally, it has set collateral and borrowing limits for various assets to ensure that systemic risks do not spread in extreme market conditions.

- Cross-chain Swaps and Data Coordination

Cross-chain swap scheduling is achieved through LI.FI, and SubQuery provides unified data indexing, allowing cross-chain lending to maintain efficiency and transparency close to that of single-chain operations.

Recent ecosystem collaborations and activities:

Technical Collaborations: Wormhole (cross-chain messaging), Chainlink CCIP (oracles), Circle CCTP (stablecoin transfers).

New Integrations: CoinStats (November 18, supporting cross-chain portfolio tracking). Monad Mainnet (November 24, launching the first 5,000 $FOLKS incentives). New assets launched on Monad include: sMON, USDT0, AUSD, wBTC, wETH.

More ecosystem resources are converging to promote the collaborative development of the cross-chain economy.

Community Activities: Auraboard Phase II (launching November 19, with $200,000+ in $FOLKS rewards).

Folks Points: This is one of the best ways to participate early, rewarding sustained activity across all chains and providing a clear pathway for new and existing users to enter the ecosystem and future community allocations.

Community activities and airdrop rewards effectively enhance user participation and engagement.

In the future, as more ecosystems are onboarded, the comparative advantages and economies of scale between multi-chains will be further unlocked, and overall capital efficiency is expected to improve.

3. Core Product Architecture: Multi-tiered Financial Infrastructure Centered on Cross-chain Lending

3.1 xChain: The Core Value of Cross-chain Lending

xChain is the core of Folks Finance's cross-chain architecture, aggregating multi-chain lending demands onto the same execution layer, allowing capital to flow freely between different public chains while maintaining the native security and integrity of assets.

Folks Finance's cross-chain architecture has significant structural advantages in terms of security and asset consistency:

The protocol does not rely on the traditional lock-mint model of bridges; all collateral is retained in contracts on their native chains, achieving true non-custodial status and avoiding centralized risks associated with cross-chain transfers.

The central chain uniformly accesses high-quality pooled assets like native USDC, ensuring consistency in asset standards for cross-chain lending and reducing potential issues such as premiums and synchronization errors associated with wrapped assets, thus providing a smoother and more reliable capital utilization experience in a multi-chain environment.

3.1.1 What Can Cross-chain Lending Bring?

Cross-chain lending may seem conceptually simple, but it involves several underlying challenges such as asset security, state consistency, and unified risk frameworks, and its true implementation carries significance far beyond the surface concept itself.

(1) Capital can flow freely across chains, significantly enhancing efficiency

Users can collateralize on Chain B and borrow on Chain A, allowing collateral to exert financial utility across chains without being restricted by chain boundaries, thereby improving capital utilization.

(2) Multi-chain lending pools achieve unified shared liquidity

Supply and demand from different public chains are aggregated into a unified framework, avoiding fragmentation in single-chain markets and allowing capital to operate within a larger pool.

(3) Forming a unified cross-chain financial operating system

Execution is centralized on the hub chain, and multi-chain operational logic is uniformly processed, enabling users to manage cross-chain portfolios from a single interface, closely resembling single-chain operations.

(4) Significantly friendlier and lower-friction user experience

Cross-chain collateralization, repayments, and liquidations do not require manual bridging, and the interaction methods are essentially consistent with single-chain operations.

3.1.2 Technical Implementation

Folks Finance's Hub-Spoke architecture stores all lending-related protocol states, including lending status, risk parameters, collateral rates, and liquidation logic, solely on the central Hub, while each Spoke chain is responsible for token custody, transfer, and cross-chain message sending.

This model has significant advantages in consistency, security, and operational costs, making it particularly suitable for lending protocols that heavily rely on unified risk and consistent states.

For tokens like USDC, the protocol bridges assets to the Hub via Circle CCTP, forming a global USDC liquidity pool on the Hub side. Users can deposit USDC on any Spoke chain, and these deposits will aggregate into the same Hub pool; when users on other chains borrow USDC, it is also deducted from this global pool, ensuring that USDC liquidity is fully shared across all chains.

For Spoke chain tokens like AVAX, their tokens remain locked in their respective Spoke chain smart contracts and can only be deposited or borrowed on their own chain. However, their position states are all uniformly recorded on the Hub, calculating borrowing limits and liquidation conditions alongside assets from other chains.

Afterward, the Spoke only initiates operations, and all logic and states are forwarded to the Hub for unified processing via Wormhole/CCIP.

In this way, the protocol has a single, cross-chain shared state layer and risk engine, enabling users to collateralize on one chain and borrow on another; compared to the traditional multi-chain, multi-pool fragmented liquidity model, this architecture allows users from different chains to share the same lending system, achieving higher capital efficiency, unified risk control, and true cross-chain lending capabilities.

3.2 Core Lending

3.2.1 Core Mechanisms and Features

Folks Finance's lending module is based on cross-chain capabilities, integrating collateralization, borrowing, and liquidation within the same execution layer, breaking through the traditional single-chain protocol's limitation that "capital can only be used on its own chain." The core value lies in: collateral remains on its native chain, security remains unchanged, but the utility of funds can be called across chains.

In practical scenarios, users can collateralize assets on Chain A and borrow funds on Chain B. For example, collateralizing ETH on Ethereum and borrowing USDC on Arbitrum to participate in trading or liquidity mining; or leveraging lower interest rates on Avalanche. This type of cross-chain usage significantly reduces bridging costs and operational friction while avoiding the additional risks associated with wrapped assets.

Folks supports both variable and stable interest rate models, covering short-term strategies and long-term holding needs. The cross-chain structure allows the protocol to balance supply and demand over a larger scope, making interest rates more sustainable and elastic compared to traditional single-chain protocols.

At the same time, the protocol includes features such as flash loans, rebalancing, and automatic liquidation. Flash loans can be used for arbitrage, position adjustments, and other one-time operations without occupying additional collateral; the rebalancing mechanism synchronizes risk indicators across chains, ensuring consistency in lending positions across different chains. These tools reduce strategy execution costs and enhance overall capital efficiency.

3.2.2 Data Performance: Current Utilization Structure

The overall lending utilization rate is currently around 32%, reflecting that the protocol is still in the early stages of capital construction but has strong security and future elasticity:

In a construction cycle, there is room for growth: as the coverage of cross-chain expands and strategy demands increase, borrowing sides are expected to gradually catch up, transitioning from low utilization to mid-high ranges, which will naturally push up APR and bring about a more stable yield structure.

3.3 Liquid Staking, DEX Router, and Ultraswap: Ecological Support and Completeness

Beyond the core lending function, Folks Finance has built a supporting ecosystem through liquid staking, a DEX router, and Ultraswap, forming a complete multi-chain product matrix.

Liquid Staking: Allows native assets to be staked while maintaining liquidity, enabling continued participation in lending or trading, enhancing capital recyclability, and increasing token utility, thereby supporting a positive economic cycle within the protocol.

Folks Finance is the issuer of xALGO, a leading liquid staking asset on Algorand. Users can stake ALGO to receive xALGO, which accumulates staking rewards. Since xALGO is liquid, it can be supplied or collateralized within Folks Finance, traded, or used in integrated DeFi protocols.DEX Router Integrating Multi-chain Liquidity: Provides optimal paths for asset scheduling, reducing slippage and the complexity of cross-chain operations, making cross-chain operations smoother for users.

On xChain: Folks uses Li.Fi to aggregate cross-chain liquidity for transactions and connect all supported networks. Li.Fi can find the optimal path among dozens of decentralized exchanges (DEXs) and bridges, enabling direct and cost-effective cross-chain position management.

On Algorand: Folks uses its self-developed Folks Router, which is designed to provide optimal trading routes between local DEXs within the Algorand ecosystem.

Ultraswap: Provides deeper liquidity for niche trading pairs, allowing more assets to be safely included in the collateral system, supporting the execution of complex strategies while enhancing the overall trading depth and robustness of the ecosystem.

Lending, liquid staking, routing, and market-making tools form a synergy, creating a complete product network capable of supporting high liquidity and token economic recyclability across multiple chains, laying the foundation for the protocol's long-term growth and ecological expansion.

3.4 Developer Ecosystem

Folks Finance provides an open-source SDK to support ecosystem growth, facilitating developer participation in innovation and supporting community and third-party developers in ecosystem building:

Cross-chain SDK: A JavaScript library supporting xChain interactions, including deposits, loans, and portfolio queries.

Folks Router SDK: Supports integrating DEX aggregators into dApps.

Simplicity JS SDK: Simplifies lending and staking operations specific to the Algorand market.

3.5 Future Development and Plans: What Will Folks Finance Do Next?

Recently, Folks Finance has made significant progress in three key areas, aiming to upgrade from a specialized lending protocol to a super gateway connecting traditional finance with a decentralized future, laying a solid foundation for the next leap.

Recent achievements include:

- Strategic Partnerships and Mobile Layout

The platform has partnered with a licensed virtual asset service provider to launch the standalone app Folks Mobile. This app integrates core DeFi functionalities such as liquid staking, swapping, and lending, optimizing the experience through AI routing, and plans to launch a debit card service supporting stablecoin collateral consumption. The newly released FOLKS token will also be deeply integrated, providing users with exclusive benefits.

- xChain V2 Upgrade

xChain V2 is set to launch, merging monolithic and vault architectures to achieve cross-chain circular liquidity, aiming to break down barriers between EVM and non-EVM chains and realize true cross-chain unification. This architecture will provide a foundation for deeper asset liquidity aggregation and advanced yield strategies.

- Next-Generation Liquid Staking Solutions

Based on xChain V2, the LST vault will initiate the next generation of liquid staking paradigms, optimizing yield efficiency through cross-chain circular vault designs. The new system will significantly enhance capital utilization efficiency and strategy flexibility while ensuring security, providing users with smarter yield generation capabilities.

4. Ecosystem Development and Market Performance: From Single-chain Champion to Cross-chain Infrastructure

4.1 Usage Statistics

Folks Finance launched on Algorand in April 2022, initially focusing lending activities on its native chain. Starting in mid-2024, the introduction of cross-chain lending mechanisms has expanded lending demand across multiple chains. This mechanism effectively allocates funds to various networks, making Folks Finance a cross-chain lending platform rather than a single-chain application. Since then, the overall lending scale has surpassed early levels, reflecting the protocol's growth and application across various ecosystems.

In terms of user activity, the total number of users on the platform has exceeded 200,000. This structure has further room for expansion and decentralization in the future, as cross-chain products are gradually opening up to more chains.

4.2 Ecosystem Development

TVL: Ecological Position and Cross-chain Expansion Capability

Folks Finance is a leading lending protocol within the Algorand ecosystem, consistently maintaining a high TVL. Its current scale has surpassed some of the leading lending projects on other mainstream public chains, demonstrating the attractiveness and expansion potential of cross-chain capital. As more chains connect, Folks' TVL reflects not only single-chain expansion but also structural improvements in cross-chain scheduling, solidifying its position as a leading cross-chain lending financial infrastructure.

5. Economic Model and Token Performance: Value Capture Pathways and Incentive Design Assessment

5.1 Token Distribution

The total supply of FOLKS is 50 million, with approximately 12.2 million currently in circulation, and an initial TGE circulation of 12.7 million, with an FDV of approximately $323 million. The combined proportion of community and ecosystem growth exceeds 50%, reflecting the protocol's user and ecological orientation.

The release of tokens for the team and investors follows a linear cycle of 12-30 months, including a lock-up period to ensure controllable circulation rhythms.

Notably, community rewards can be claimed immediately or released linearly with additional returns, optimizing the structure of lock-up and market pressure.

5.2 Token Functions and Value Circulation

The FOLKS token serves multiple functions within the protocol, each driving a positive cycle of protocol value:

Governance: Token holders participate in decision-making, aligning the protocol's direction with ecological development, enhancing governance efficiency and community engagement.

Staking: Token staking can enhance yields, increasing the time funds remain within the protocol and improving liquidity stability.

Economic Incentives: Rewards are provided within ecological products such as lending, market-making, and cross-chain execution, incentivizing users to continue participating in protocol activities.

Value Recirculation: As cross-chain lending expands, cross-chain liquidity strengthens, and components like Ultraswap and liquid staking mature, the fees and economic activities generated by the protocol increase the usage scenarios for the token, allowing FOLKS' value to circulate continuously within the ecosystem, forming a stable value flywheel.

5.3 FDV and Price Performance: Relative Undervaluation Amidst Steady Performance

After five years of development, Folks' product matrix and value capture mechanisms are relatively mature, with cross-chain lending, Ultraswap, and routing forming a complete ecosystem. Despite steady FDV performance, there remains room for undervaluation compared to the protocol's functionalities, ecological completeness, and first-mover advantages in cross-chain capabilities. The main reasons include:

Unique cross-chain lending mechanism: No need for bridging, maintaining native assets, providing a clear competitive moat.

High ecological completeness: Reducing friction costs and enhancing security.

Integration of financial tools like flash loans: Offering a broader strategy space and potential user base.

Strong adaptability to the Algorand chain: The chain-level characteristics align closely with mainstream financial scenarios, providing underlying support for the protocol's robust operation.

Folks Finance's FOLKS token was first listed for trading on Binance Alpha on November 6, 2025, and that same evening, its USDT perpetual contract was also launched on the Binance contract platform. The price on the first day was $2, subsequently peaking at $11.50, an increase of approximately 475%, reflecting the market's high recognition of the token.

6. Investment Observations and Valuation Framework: Finding Paths to Value Realization in Cross-chain Evolution

Development Overview:

|------------|---------------------------------------------| | Date | Event | | 2022/1/20 | Folks Finance completed a $3 million seed round financing | | 2022/4/4 | Folks Finance launched on the mainnet | | 2024/2/6 | Folks Finance completed strategic financing, amount undisclosed | | 2024/11/14 | Folks Finance completed a $3.2 million Series A financing, with a valuation of $75 million | | 2025/11/6 | Binance Alpha and perpetual contracts will launch Folks Finance (FOLKS) | | 2025/11/6 | FOLKS token officially launched |

6.1 Financing Situation

To date, Folks has completed a total of $6.2 million in financing. Folks Finance's multiple rounds of financing have attracted leading institutions such as Coinbase Ventures, Borderless Capital, and Jump Crypto, with investors spanning infrastructure funds, exchange ecosystem funds, and strategic capital. The overall structure is diverse and professional, supporting both cross-chain infrastructure and providing strategic synergy with public chains, ensuring solid support for the protocol's cross-chain expansion, liquidity construction, and ecological development. The financing reflects the market's high recognition of the positioning of cross-chain financial infrastructure.

6.2 Valuation Analysis

6.2.1 Sector Perspective

From a sector perspective, the overall TVL of DeFi lending protocols is $64.67 billion, currently at a new high since 2025.

Folks Finance's current TVL is approximately $132 million, corresponding to borrowed funds of about $31.14 million, consistently ranking at the top within the Algorand ecosystem, gradually expanding to multiple public chains.

Under a conservative assumption of maintaining market share, a linear projection can be derived:

|-----------|-----------|--------------------| | Industry TVL Scenario | Industry Scale (in billions) | Folks TVL Projection (in millions) | | Current | ~65 | ~132 | | 2× | ~130 | ~264 | | 5× | ~325 | ~660 | | 10× | ~650 | ~1320 |

However, due to Folks adopting a cross-chain lending architecture, its growth will not strictly follow a linear path. The cross-chain model can simultaneously accommodate lending demands from multiple chains, structurally enhancing capital utilization compared to single-chain lending; thus, the "effective TVL" tends to be higher at the same scale. Therefore, during industry expansion, Folks' actual TVL growth rate often exceeds linear projections.

6.2.2 Secondary Market Perspective

From the secondary market perspective, FOLKS' current FDV is approximately $400-450 million, with an FDV/TVL ratio of about 3-3.5 times and a circulating market cap/TVL ratio of about 0.9 times, overall still positioned in the mid-range of the industry pricing spectrum. Compared to some leading lending protocols with circulating market cap/TVL ratios often exceeding 1-2 times, or even FDV/TVL ratios of 4-5 times, Folks' current valuation is not expensive.

At the same time, according to data from Coingecko, $FOLKS ranks among the top three by market cap in the EVM DeFi lending space, only behind Aave and Morpho. Its leading capabilities in cross-chain lending and unified liquidity are significantly higher than those of similarly sized protocols, providing ample room for upward expansion in terms of TVL, utilization, and revenue.

Overall, FOLKS currently appears to be in a rapid growth phase characterized by "cross-chain network effects yet to be fully realized": underlying technology is mature, ecological components are gradually improving, but the scaling effects of cross-chain lending have not yet fully reflected in TVL and revenue. As more multi-chain assets are onboarded and cross-chain usage increases, the liquidity aggregation effects will become more pronounced, making it easier for valuations to converge towards industry averages, with high elasticity and recovery potential.

7. Conclusion: When Capital Truly Flows Freely, It Marks the Starting Point for On-chain Finance's Long-term Development

The fragmentation of multi-chains is a core bottleneck hindering the growth of DeFi, while capital truly needs the freedom to cross chain boundaries. What Folks Finance has built is not just cross-chain lending, but a gateway to the integration of on-chain finance. When liquidity is re-aggregated and value is reconnected, dispersed ecosystems can move towards integration, generating positive externalities between chains and enhancing overall efficiency and user experience in tandem with scale.

The next phase of DeFi will ultimately be defined by protocols that can weave chains into a network.

Risk warning Risk warning

Risk warning Risk warning