A Brief History of Perpetual Contracts and the Future

Decentralized perpetual contract exchanges, such as Hyperliquid, are replacing traditional derivatives with structural advantages, becoming trillion-dollar financial platforms that attract global assets.

Decentralized perpetual contract exchanges, such as Hyperliquid, are replacing traditional derivatives with structural advantages, becoming trillion-dollar financial platforms that attract global assets.Original Author: MONK, Ryan Watkins

Compiled by: ChainCatcher

Introduction

Over the past 17 years, a handful of blockchain innovations have broken out of their information silos, bringing leapfrog improvements to the traditional financial system. Whether it’s digital gold, stablecoins, or prediction markets, each product was initially designed as a niche use case for native cryptocurrency users, only later proving to have broad utility for society as a whole.

We believe the next such output will be perpetual contracts, and more importantly, decentralized exchanges built for trading perpetual contracts.

Although the industry has begun to view decentralized perpetual contract exchanges as an exciting growth story, there remains widespread misunderstanding about their significance and the scale of their potential opportunities. We believe that in the coming years, perpetual contracts will start to absorb a multitude of new asset classes, from stocks to commodities, with decentralized exchanges emerging as the biggest winners in this transformation.

Below we outline our perspective: by 2030, decentralized perpetual contract exchanges will capture a significant portion of the total trading volume of options, futures, and contracts for difference, which we believe could bring hundreds of billions of dollars in market capitalization to the industry.

A Brief History of Perpetual Contracts

Essentially, a perpetual contract is a derivative that allows traders to maintain leveraged exposure to an asset without an expiration or settlement. Depending on price deviations, funding rates are periodically paid between longs and shorts to keep the perpetual contract market aligned with spot market prices. Meanwhile, risk is managed through continuous margin and liquidation mechanisms, with profits and losses redistributed in real-time within a shared collateral pool. These mechanisms work together to allow positions to remain open indefinitely as long as they remain solvent, concentrating trading activity in a 24/7 market rather than dispersing it across different expiration dates.

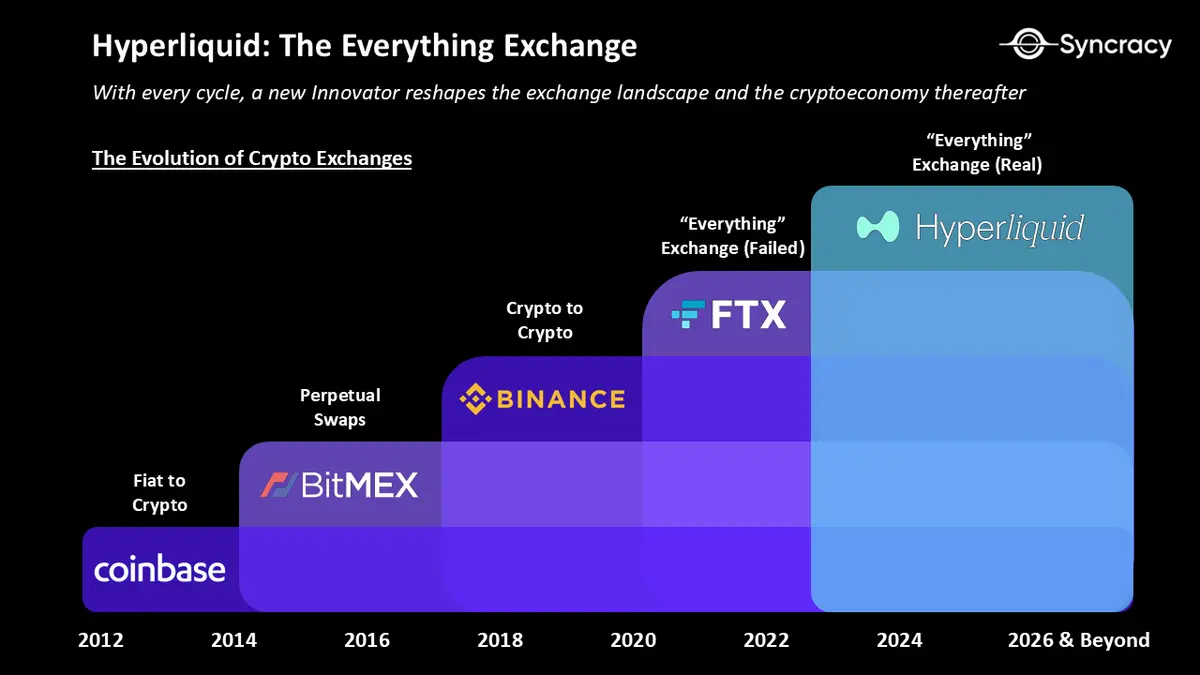

The concept of perpetual contracts was first formally proposed by economist Robert Shiller in 1993 but remained theoretical for decades. In traditional finance, this concept clashed with markets built around fixed expiration dates, batch settlements, centralized clearing, and limited trading hours. This changed in 2016 when Arthur Hayes and BitMEX introduced perpetual contracts into the crypto space under pressure from Asian competitors.

Despite Huobi and OKX controlling over 90% of the daily trading volume in cryptocurrency futures at the time, BitMEX rose to dominance as an exchange in just two years, largely due to the rapid growth of its perpetual contracts. By 2018, BitMEX had effectively phased out its time-limited futures products and led all cryptocurrency exchanges in liquidity and trading volume.

We believe this period serves as an inspiring consumer case study that showcases the competitiveness of perpetual contracts. In a fully neutral market competition, perpetual contracts decisively outperformed traditional fixed-term futures and options structures. Today, perpetual contract trading in cryptocurrencies is so prevalent that the nominal trading volume of Bitcoin perpetual contracts is approximately six times its spot trading volume—this unique market structure dynamic is not found in any other asset class.

The Rise of Decentralized Perpetual Contract Exchanges

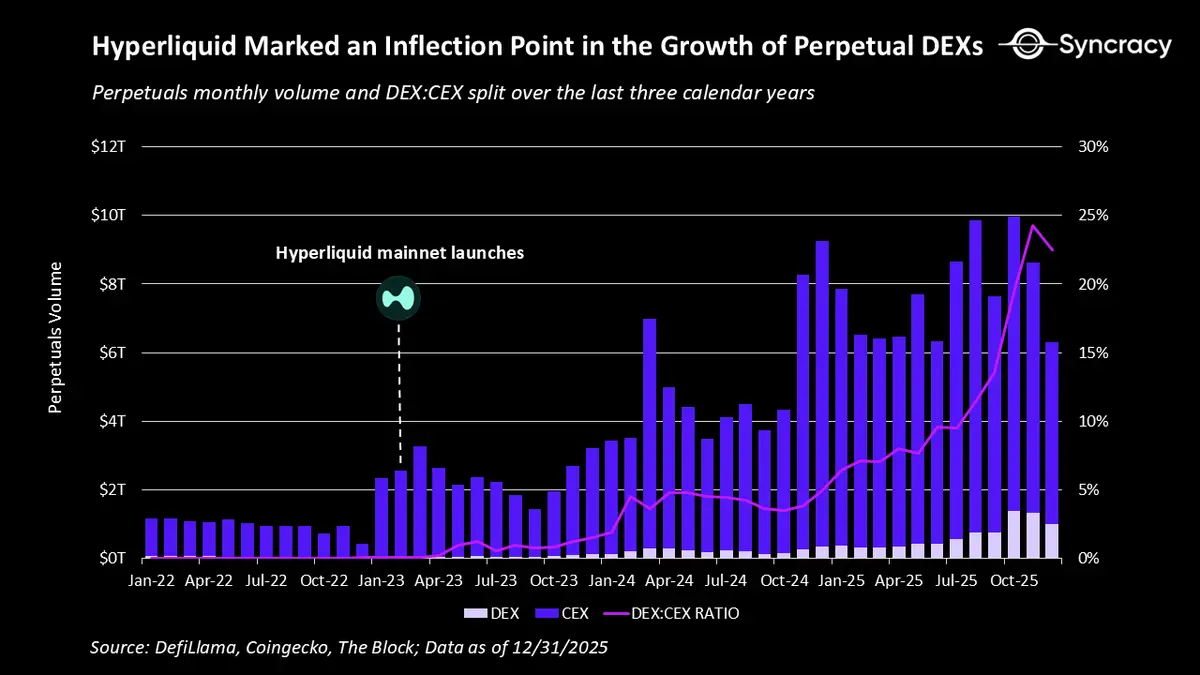

While centralized exchanges like Binance currently dominate the perpetual trading volume with about 83% market share, the most exciting evolution in this market is the accelerated growth of decentralized perpetual exchanges.

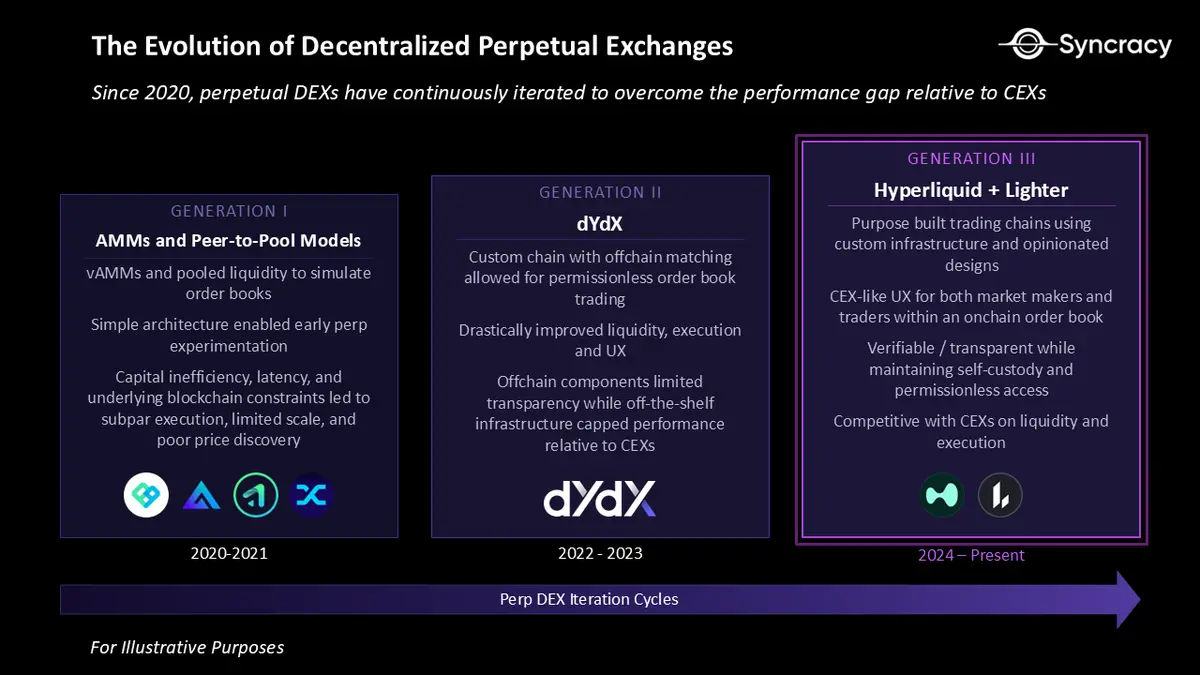

The concept of decentralized exchanges has existed for over a decade, promising self-custody, real-time auditability, permissionless construction, and global accessibility. However, these features often come with significant performance compromises. Early decentralized perpetual exchanges faced issues such as limited throughput, high latency, and rudimentary risk engines, preventing them from competing with centralized exchanges.

The launch of Hyperliquid changed this perception, providing the first truly competitive decentralized exchange experience for perpetual contracts. Hyperliquid did not simply replicate exchange logic on-chain but rethought blockchain architecture from the ground up, placing trading as its core use case.

Its validator nodes are closely co-located, significantly reducing consensus latency and enabling collaborative custody for market makers—something that has long been considered a fundamental requirement in traditional high-frequency trading. Additionally, the team established clear order execution rules, allowing market makers to prioritize order cancellations, effectively alleviating the harmful order flow commonly found in early blockchain systems that relied on auction-style order matching. Finally, the chain employs predefined trading fees rather than variable gas pricing, reducing execution uncertainty and lowering costs for mature participants.

The emergence of Hyperliquid marks a significant turning point in the competitive landscape between DEXs and CEXs. Since its launch, DEXs have been rapidly gaining market share from CEXs as performance and user experience are no longer limiting factors. Today, Hyperliquid and Lighter have become among the best venues for retail trading execution of major crypto assets.

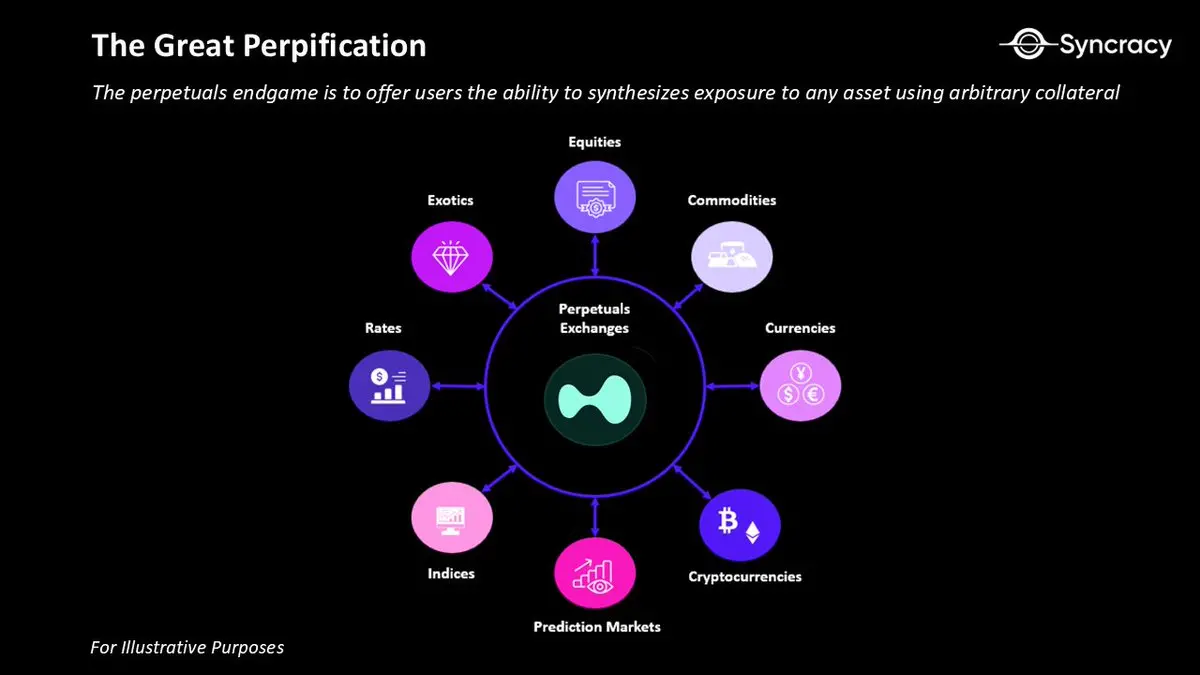

The Great Perpetual Expansion

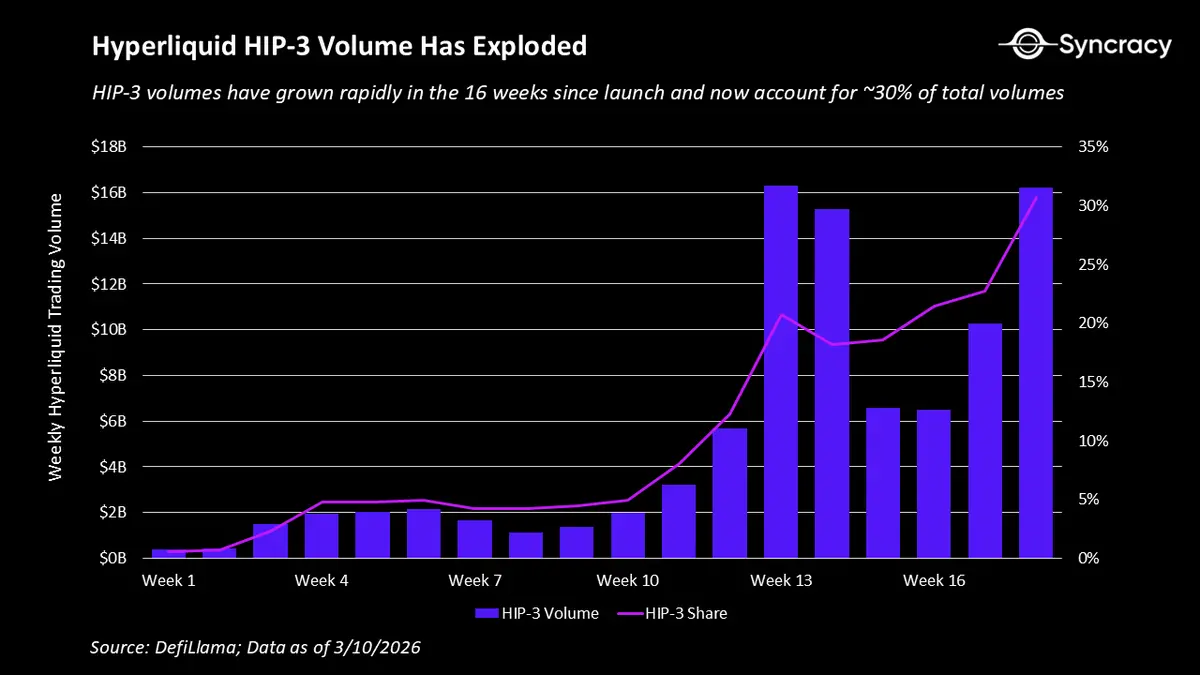

In November 2025, with the launch of HIP-3, Hyperliquid took a decisive step beyond crypto perpetual contracts, transforming from a cryptocurrency-only exchange into a universal perpetual contract platform. HIP-3 allows third-party deployers to launch new perpetual contract markets on Hyperliquid's order book, provided they meet minimum technical standards and post 500,000 HYPE as collateral.

Since perpetual contracts are freely floating derivatives, they can, in principle, be created based on any asset with a reliable price information source. Within three months of HIP-3's launch, Hyperliquid witnessed a rapid surge in new markets covering individual stocks, stock indices, commodities, and even pre-IPO private companies. So far, these new markets have driven over $100 billion in trading volume, marking the most successful attempt to bring traditional asset classes onto the blockchain at scale.

The success of the Hyperliquid HIP-3 market has sparked immense interest from existing giants and emerging competitors. In recent months, both Binance and Coinbase have launched their own perpetual contracts for stocks and commodities. As investors blindly chase the "next Hyperliquid," venture capital inflows into this space have surged. Meanwhile, leading blockchains like Solana have prioritized "solving" perpetual contracts.

All this activity hints at an emerging argument: compared to spot tokenization, perpetual contracts are the fastest and most liquid way to introduce new assets to the blockchain while embedding real-world applications. After all, cryptocurrencies have largely served as an asset class for speculators chasing excess returns, and perpetual contracts provide the "speculative thrill" that makes tokenization feel valuable to real users.

As the perpetual contract market now expands from the core cryptocurrency market to include stocks, commodities, currencies, and long-tail exotic assets (which we referred to as "everything exchanges" in our initial Hyperliquid research report), we believe the opportunities for decentralized exchanges in perpetual contracts are now an order of magnitude greater than before. This development also reshapes the business of these exchanges, significantly reducing their reliance on the cyclicality of cryptocurrencies.

How Perpetual Contracts Are Absorbing the Retail Speculation Market

So far, stock and commodity perpetual contracts have primarily found product-market fit among crypto-native traders. For this user group, the appeal lies simply in bringing traditional assets closer to them. For some users outside the U.S., the appeal is the ability to access assets that would otherwise require residency in specific jurisdictions or specific brokerage/private banking relationships.

Although the poor performance of cryptocurrencies relative to stocks and commodities since the historic 10/10 liquidation event in 2025 has accelerated the adoption of this group, the most important question is: where will the next growth drivers come from? Who else can this innovation be exported to beyond the crypto-native user base? We believe the answer lies in one of the clearest long-term growth trends in finance—the rise of global retail speculators.

The Rise and Resurgence of Retail Speculators

"Looking around, in a country that has become a nation of traders, higher leverage is evident everywhere in the stock infrastructure." ------ Paul Tudor Jones

As more market participants and social commentators have observed, the world seems to be in the midst of a retail-driven speculative supercycle. While the drivers of this behavior are debated—from rising living costs and insufficient social mobility forcing people to speculate, to the proliferation of smartphones and deregulation making speculation easier—the trend is clear. More and more people are becoming traders every day. With a growing middle-class population, internet communities built around trading, and over 4 billion individuals globally still "without brokerage accounts," we believe there is significant room for acceleration in this trend.

As this phenomenon evolves, interest in leverage has also grown. Retail participation in the derivatives market has surged, with record shares of trading volume in options, contracts for difference, and traditional futures.

According to estimates from the Chicago Board Options Exchange, by 2025, trading activity from retail brokers will account for more than half of the total options trading volume in the U.S.

In the same year, retail CFD trading volume reached an all-time high, with five brokers reporting average monthly trading volumes exceeding $1 trillion for the first time.

Meanwhile, the U.S. Commodity Futures Trading Commission noted that the average trading volume of retail futures in the U.S. remains about 50% higher than pre-pandemic levels.

Importantly, these capital flows are not only larger in scale but also faster, increasingly leaning towards short-term positions. Sample data from the CFTC in 2024 indicates that the average retail futures trader holds contracts for only a few days; while data from Cboe shows that retail participation is highest in options trading that expires the same day.

Ironically, the options and futures contracts currently used to satisfy risk appetites were originally designed for risk management. In contrast, perpetual contracts are specifically built for directional risk.

Retail traders are likely being guided to use imperfect tools out of necessity, while perpetual contracts may represent an elegant fit between product design and user demand. Evidence in the crypto space has already emerged, as a new generation of derivatives traders has convincingly expressed their preference for perpetual contracts. Below, we will review some inherent advantages of perpetual contracts compared to existing alternatives.

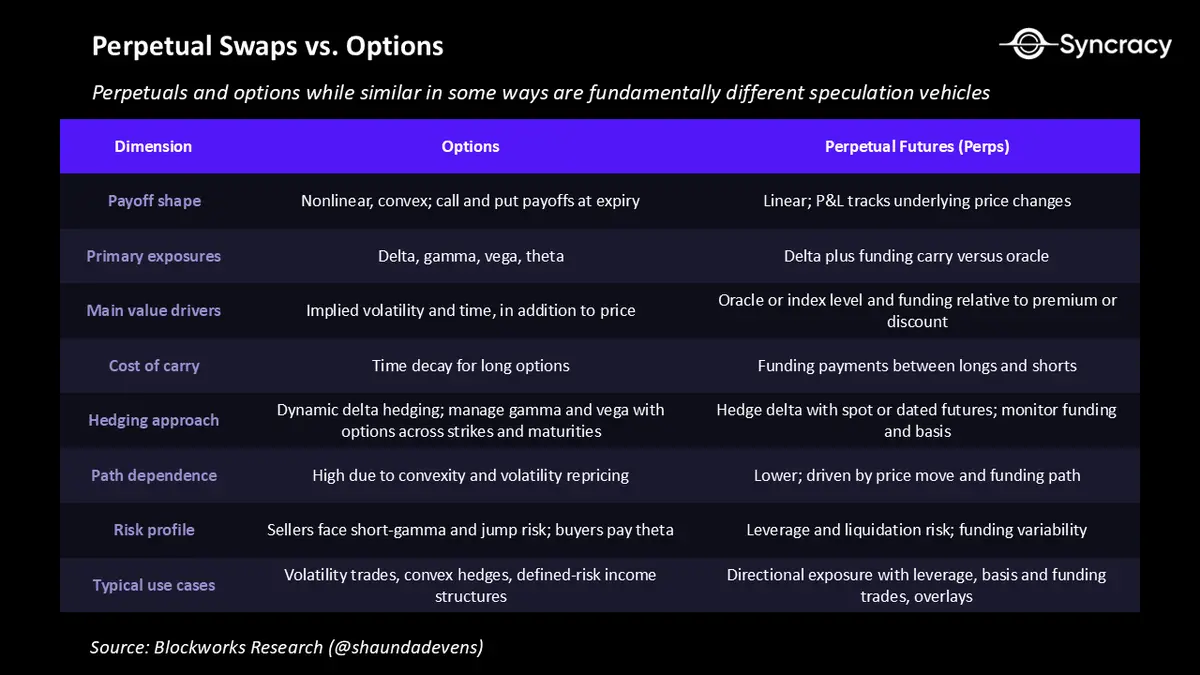

Perpetual Contracts vs. Options

"The principle of Occam's Razor, or the principle of simplicity, tells us that the simplest, most elegant explanation is often the closest to the truth."

The enduring appeal of perpetual contracts compared to options lies in their simplicity.

For retail traders seeking leveraged directional exposure, perpetual contracts eliminate many of the cognitive burdens associated with other derivatives. There’s no need to choose expiration dates, manage time decay, or calculate implied volatility. Instead, exposure (whether long or short) is linear, continuous, and intuitive—similar to holding a spot position.

From the perspective of market makers, perpetual contracts are equally efficient. Liquidity is concentrated in a single order book rather than dispersed across different expiration dates and strike prices as in options and futures markets. The result is deeper liquidity and more robust price discovery.

While perpetual contracts may not be as expressive as options for constructing customized yield curves or hedging complex portfolios, their simplicity is precisely why they remain efficient over any holding period. For traders intending to open and close positions within days rather than months, perpetual contracts offer a clear advantage by completely eliminating the need to manage expiration dates. In the aforementioned Chicago Board Options Exchange case study, retail traders relying on 0DTE options for leveraged trading endure extreme theta decay. With perpetual contracts, they simply need to fine-tune their desired leverage to manage predefined liquidation levels.

Although perpetual contracts are not a universal substitute for options, we do believe they better capture the speculative impulse of retail traders without adding complexity. Options will continue to play a key role in expressing volatility views, managing tail risks, and constructing structured exposures. Their convexity-driven returns remain attractive and can avoid liquidation risks before expiration. However, these use cases lie outside the core range of most retail trading activity.

Essentially, we believe perpetual contracts reflect an "Occam's Razor" approach that satisfies the growing appetite for leveraged trading among retail traders.

Perpetual Contracts vs. Contracts for Difference (CFDs)

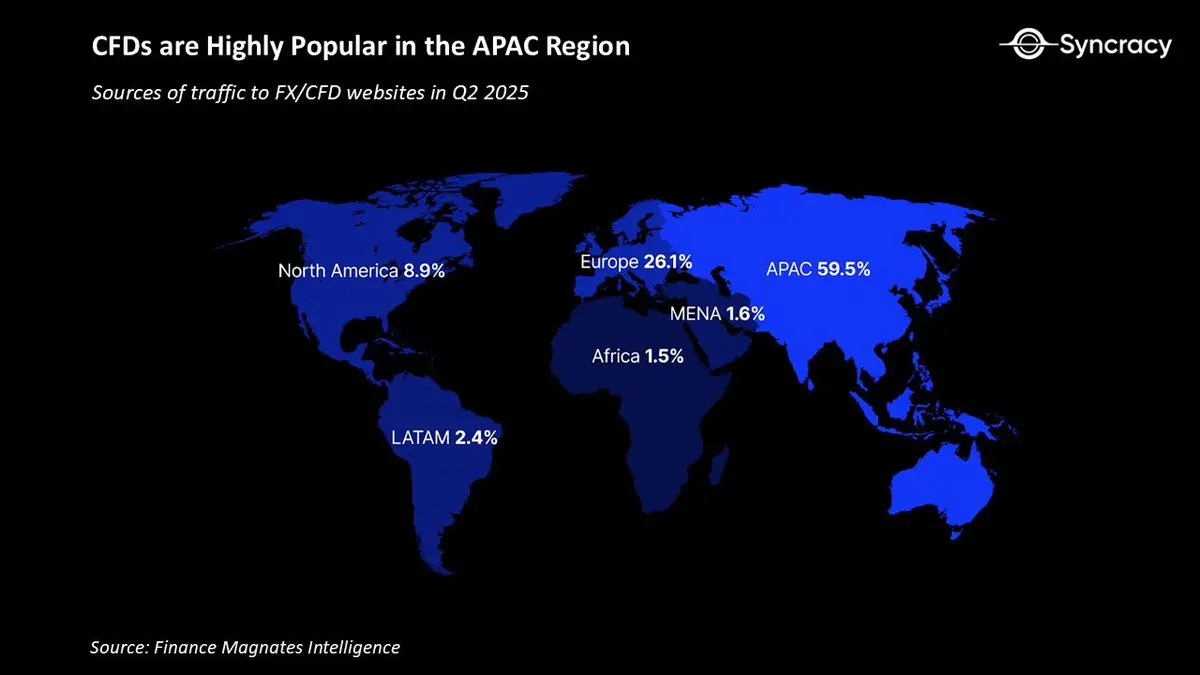

While options trading has exploded among retail traders in the U.S., in Asia, retail traders are increasingly leaning towards contracts for difference. By 2025, the global forex/CFD industry’s average monthly trading volume exceeded $30 trillion, far above less than $10 trillion a decade ago. Notably, about 60% of CFD website traffic comes from the Asia-Pacific region, while North America accounts for only about 9%.

Mechanically, CFDs are similar to perpetual contracts in several important ways. They allow traders to gain leveraged directional exposure without owning the underlying asset, typically have no fixed expiration date, and financing costs are embedded in positions over time. Like perpetual contracts, they can be used for short-term speculation across various asset classes. In many ways, CFDs represent a compromise that traditional systems have attempted to approximate in order to formally establish the economic properties of perpetual contracts more clearly.

However, CFDs are structurally still a compromise. They are provided over-the-counter by brokers, creating bilateral credit exposure between traders and dealers. Pricing is opaque, spreads are set by brokers, and risk controls can be adjusted unilaterally. Liquidity is dispersed across the ledgers of various brokers rather than centralized in a single, transparent order book. Each position is essentially an isolated and arbitrary agreement between the broker and the trader, with the broker determining the terms of the relationship.

While options can offer clear advantages over perpetual contracts, it is difficult to identify what enduring value proposition CFDs hold. They inherit the inefficiencies, opacities, and trust assumptions that perpetual contracts aim to eliminate. In this sense, CFD brokers may be among the traditional businesses most easily disrupted by the perpetual contract market.

Achieving 24/7 Trading Democratization

Another underappreciated advantage of stock and commodity perpetual contracts is their ability to unlock 24/7 trading. This represents a paradigm shift for retail traders by changing when and how returns are accessed.

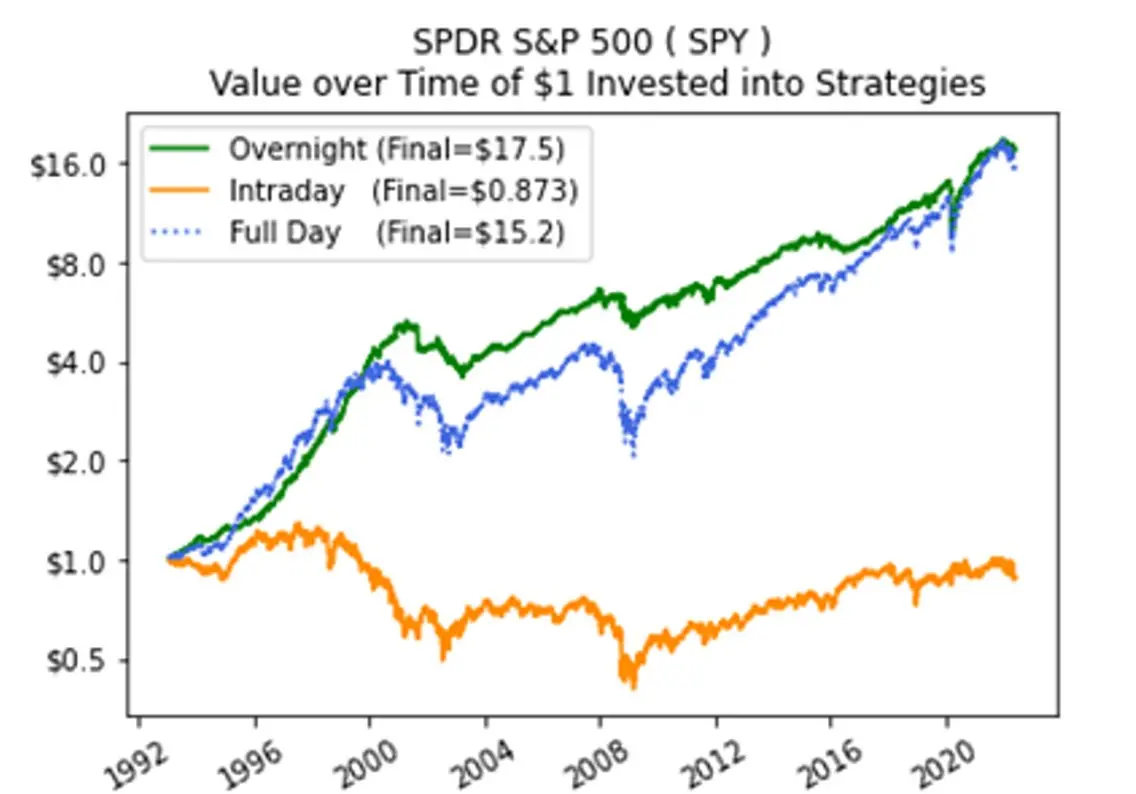

In the stock market, researchers have confirmed that restricted trading hours pose a structural disadvantage to retail traders, primarily due to an effect known as "overnight drift." Data shows that a disproportionate share of long-term returns in U.S. stocks is generated outside regular trading hours, with overnight price movements accounting for a significant portion of realized performance.

This becomes quite intuitive considering that earnings reports and major news releases are often published before the market opens or after it closes, and the U.S. public market has longer closing hours than opening hours. Many market-moving news headlines break overnight or on weekends, during which retail traders are structurally marginalized. Those who can access these timeframes are typically hedge funds, institutions, and high-net-worth participants who can trade through after-hours venues or preferential off-exchange channels.

Academic research suggests that this imbalance may be amplified in so-called "meme stocks," where retail participation is high. A 2022 study found that retail traders disproportionately place orders at market open, which is precisely when liquidity is thinnest and adverse selection is most severe. The authors illustrated the extent of this effect with a striking example: "A day trader who bought AMC Entertainment stock at market open and sold it at market close from early 2019 to late May 2022 would have lost 99.6% of their capital—however, if they had made the same trades overnight, they would have gained 30,000% during the same period (ignoring transaction costs)." While extreme, this example highlights how merely the boundaries of trading timeframes can significantly shape actual outcomes.

In attempting to explain this behavior, one theory posits that retail traders often think about potential trades at night or on weekends (when they are off work) and then submit orders for execution at the next market open. If that’s the case, why not completely eliminate this friction and allow traders to interact with the market whenever it’s convenient for them?

Today, decentralized perpetual contract exchanges may be one of the few places on Earth capable of doing just that. By providing continuous exposure, they allow traders to interact with the market when news breaks, unrestricted by traditional market hours. In fact, this is no longer theoretical. Just last weekend, during extreme concerns over the Iran conflict, Hyperliquid facilitated over $1 billion in crude oil trades. Traders were able to capture 30% of spot volatility from Friday’s close to Monday’s open, while retail traders elsewhere in the world were forced to sit on the sidelines.

It should be noted that during the lack of liquidity trading windows when traditional markets are closed, spreads often widen. However, we believe many users are willing to tolerate imperfect execution in exchange for access opportunities. As perpetual DEX products mature, 24/7 trading may prove to be one of their most powerful user acquisition funnels.

All Roads Lead to Decentralized Exchanges

As the opportunities for perpetual contracts become increasingly evident, traditional exchanges will inevitably enter this arena. We have already seen the Intercontinental Exchange, Chicago Mercantile Exchange, and Nasdaq announce that they are launching 24/7 trading for their respective markets. We believe it is only a matter of time before they launch tools similar to perpetual contracts. If existing enterprises from traditional financial exchanges to U.S. centralized crypto exchanges roll out and expand their perpetual contract products, what lasting advantages will decentralized exchanges have left?

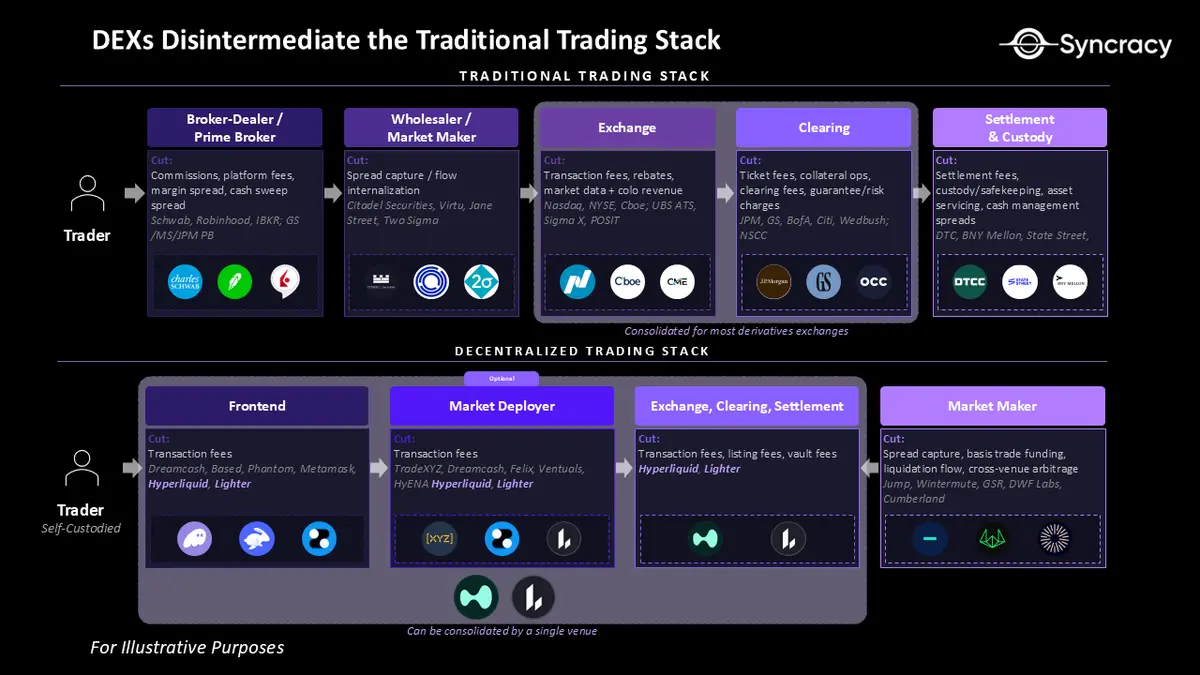

Incompatibility Issues

Decentralized perpetual contract exchanges may be the most misunderstood technology in the crypto space. Many critics view platforms like Hyperliquid as products of regulatory arbitrage, merely waiting to be prosecuted. However, over time, it may become increasingly clear that these exchanges are actually modernizing the trading stack. Just as electronic trading at the end of the 20th century changed how markets handled execution, monitoring, clearing, and settlement, crypto-native exchanges are rethinking how to integrate and automate these functions within a single system. It’s hard to imagine that just a few decades ago, global trading activity was still concentrated in the halls of physical exchanges.

Decentralized perpetual exchanges do not distribute responsibility across multiple intermediaries; rather, they integrate most of the trading stack into a single cohesive system with atomic margin and settlement capabilities. The exchange itself performs many functions traditionally handled by different roles: the front end acts as a broker interface, smart contracts manage clearing and settlement in real-time, and APIs allow market makers to interact natively with takers within the venue. In other words, work that previously required multiple layers of institutions and internal operating systems can now be coordinated by a single protocol that never sleeps.

Moreover, we believe that these decentralized exchanges' ability to transparently and autonomously maintain solvency has not received enough credit. Essentially, Hyperliquid has built the world’s best algorithmic clearing engine on a verifiable ledger. Retail traders gain a powerful and predictable assurance: they deposit a clear amount of collateral, leverage is applied programmatically, and only the deposited margin will be liquidated. Internally, positions between longs and shorts are continuously balanced, and the system can trigger automatic liquidations when necessary to prevent the exchange from becoming insolvent.

While some critics point to tail risks of ADL in extreme market events, it is precisely this mechanism that allows the system to support unprecedented levels of leverage—typically in the range of 20-50x—without relying on centralized capital backstops (i.e., this is a feature, not a flaw). Unlike traditional margin systems, there are no layers of intermediaries, no discretionary credit decisions, and no bilateral loan agreements. On Hyperliquid, risk management is deterministically handled by code, and everyone follows the same set of rules.

For large financial institutions accustomed to multi-layer counterparty agreements and negotiable margin terms, this model may seem rigid or unfamiliar. But for the vast majority of retail traders, this product is more than sufficient and allows them to speculate in the most agile and efficient capital manner. In a sense, Hyperliquid is commoditizing leverage.

While extending trading hours may be relatively straightforward for traditional exchanges, introducing the aforementioned perpetual contract stack is fundamentally incompatible within the current regulatory and infrastructure framework. In the U.S., stock/commodity perpetual contracts remain subject to the Commodity Exchange Act and the Dodd-Frank Act, which require execution in regulated venues and clearing through centralized clearinghouses. These rules disperse the trading stack across brokers, exchanges, and clearinghouses, with each layer extracting its own economic rent and accumulating technological debt. The result is a system where execution, risk management, and settlement are handled by a bloated set of gatekeepers operating on different tracks.

Traditional institutions cannot simply append perpetual contracts to this framework. They require thorough bottom-up regulatory reform or coordinated integration of operations among different participants in the stack. This means that truly reflecting the 24/7 algorithmic capabilities of crypto exchanges in perpetual contracts remains a long-term project for traditional enterprises, measured in years.

While key regulatory frameworks like the Dodd-Frank Act are understandable responses to the embarrassing risk control failures exposed by the 2008 financial crisis, some of these changes may prove to be overreactions in hindsight. In attempting to eliminate risks across an entire category, these reforms may have rendered their industry incapable of innovating in the face of technological change.

With this in mind, the real question is not whether traditional enterprises can replicate the perpetual contract experience of cryptocurrencies, but whether they can build competitive products before it’s too late. Will companies like Robinhood or ICE ultimately be able to construct equivalents to systems like HyperCore and HIP-3? If they have sufficient funding, initiative, and regulatory leniency, it is possible. However, the winners of technology often have path dependencies, and by the time existing enterprises gain the regulatory clarity needed to launch perpetual contracts and complete the structural reforms required to support them, the competitive landscape may have already solidified.

Users will not wait five years for a familiar brand to offer them perpetual contracts. Now, Hyperliquid has gained broader media attention due to the viral spread of its product. As Hyperliquid Labs entities and their partners continue to accelerate their market entry strategies, the window for traditional enterprises to compete effectively is rapidly closing. On the other hand, Hyperliquid is continuously iterating its own system, making it increasingly difficult for new entrants to reach parity with the product.

In this race to serve the global demand for perpetual contracts, native crypto exchanges are running the fastest, and they may soon reach escape velocity. In our view, supporting existing enterprises burdened by outdated infrastructure in this transformation is akin to betting that The New York Times will win the online media war, Intel will win the GPU computing war, or Blockbuster will win the streaming war. History repeatedly tells us that new technologies create new winners.

Permissionless as a Scaling Advantage

Blockchains are inherently open, borderless systems. They allow anyone connected to the internet to access applications and empower developers to build on them, effectively functioning as a global API for currency and finance. Decentralized exchanges built on blockchains inherit these "permissionless" attributes, which we believe provide them with a significant scaling advantage over existing enterprises in the long run.

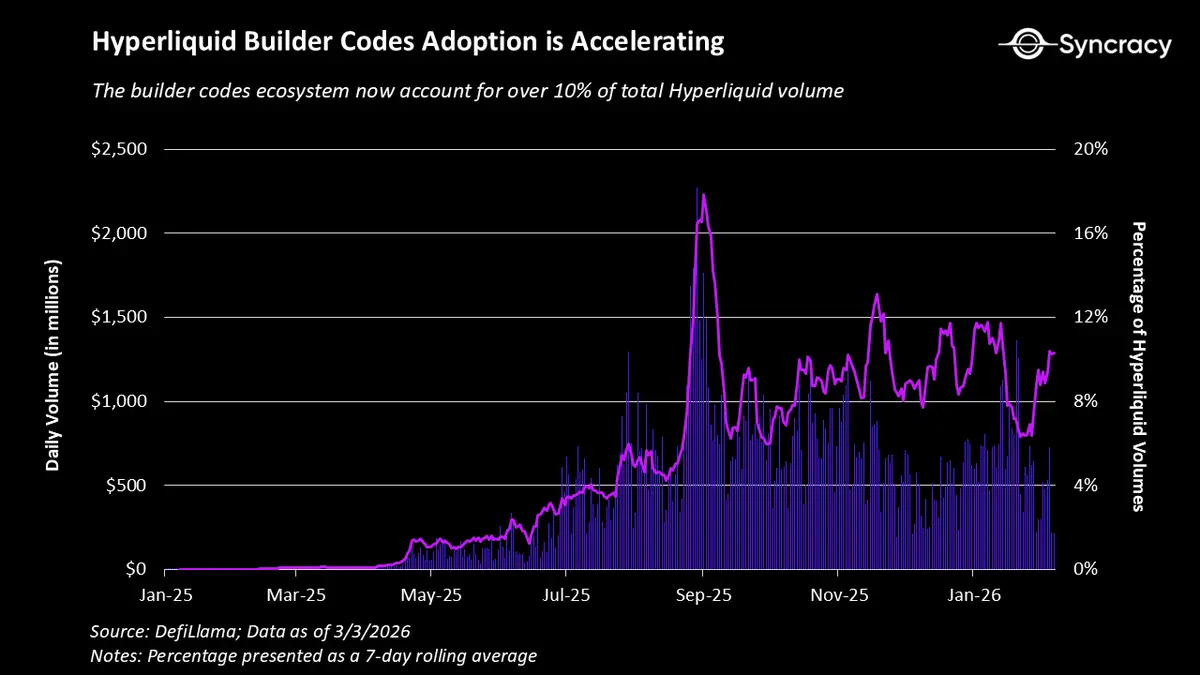

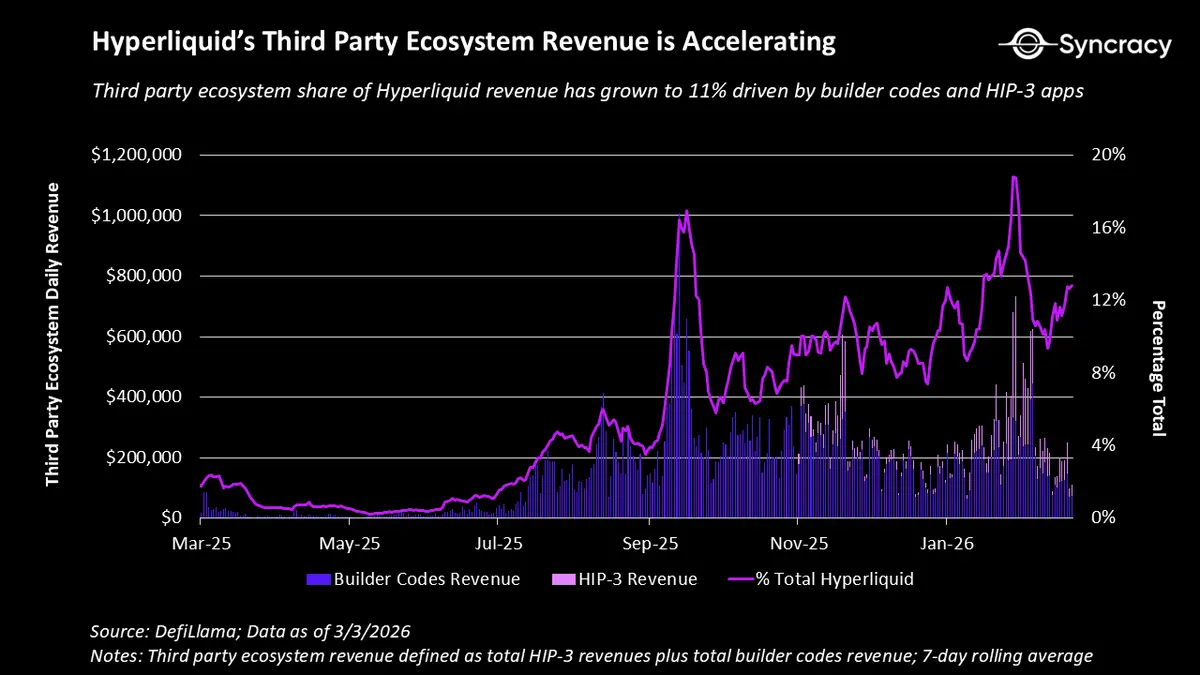

From the builder's perspective, decentralized exchanges benefit from the utility and distribution flywheel generated by the growth of their developer ecosystem. The builder code of Hyperliquid and the HIP-3 market provides an excellent example of this.

The builder code establishes a fee-sharing mechanism that provides strong incentives for third-party applications to integrate Hyperliquid on the backend. The practical implication of this is that while centralized exchanges are busy personally attracting new taker flow, Hyperliquid has a host of front-end applications competing for its traffic. Incremental distribution can be turned on like a switch, such as when Phantom introduced over 10 million new traders overnight. In the future, this could mean a large regional exchange providing access to Hyperliquid in local languages, a U.S.-regulated broker layer offering higher leverage or protection for Hyperliquid traders, or even a social media giant introducing perpetual contracts to its user base to increase average revenue per user.

As mentioned, HIP-3 allows third-party deployers to launch new perpetual contract markets on Hyperliquid's order book to trade new types of assets. This open process for creating new markets enables Hyperliquid to onboard assets faster than any centralized institution. In equilibrium, each new auction should reveal the new assets with the highest speculative demand potential, ensuring Hyperliquid consistently captures trading volume from the areas of greatest attention and volatility. This has already been a significant boon during the recent surge in metal prices, with a single silver perpetual contract market operated by a third-party team achieving daily trading volumes exceeding $1 billion.

Combined with the builder code, these mechanisms allow deployers to launch exchanges entirely built on Hyperliquid. Today, Hyperliquid's third-party ecosystem generates $90 million in annualized revenue. Competitors are now forced to ask themselves a crucial question: is it better to compete with Hyperliquid or simply collaborate with them?

From the user's perspective, decentralized exchanges democratize capital markets. While U.S. users may ultimately benefit from easier access to foreign assets, the biggest beneficiaries may be non-U.S. users. Over 6 billion people globally can access the internet, yet 4 billion remain "without brokerage accounts." Meanwhile, the adoption rate of stablecoins (the leading dollar asset on the blockchain) is experiencing exponential (hockey-stick) growth internationally.

Moreover, a significant portion of speculative activity occurs outside traditional brokerage channels, particularly in Asia, the Middle East, and South America, where overnight and weekend trading predominates, and opportunities to enter the U.S. market are limited. Decentralized exchanges allow these users to participate directly, aggregating global liquidity without jurisdictional islands or access barriers.

In summary, we believe the architecture of decentralized exchanges brings faster experimentation, broader asset coverage, and a larger potential market.

The Economics of Autonomous Systems

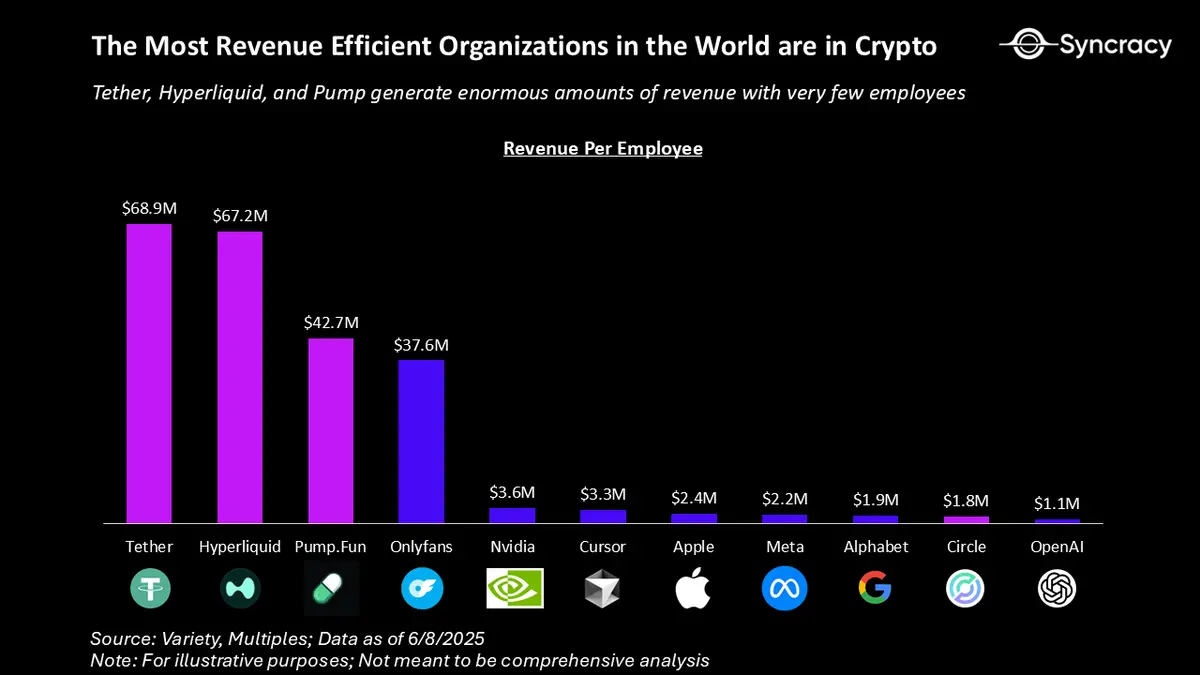

In our initial Hyperliquid research report, we described Hyperliquid as "one of the most efficient cash flow machines in the world." Today, it operates at a run rate of $1 billion in annualized revenue with a net profit margin of up to 99%, yet has only 12 employees. These metrics are not only unmatched by any company in the S&P 500 or Nasdaq but, at $83 million in revenue per employee, it is one of the highest revenue-generating organizations per capita globally.

While Hyperliquid is the largest-scale embodiment of this model, it is not the only decentralized exchange with this economic potential. To understand this, it is important to distinguish between what constitutes internal economics of an exchange and what constitutes external economics.

At the core of the argument is that decentralized exchanges are software, not institutions. The core team bears the upfront costs of building the exchange and may receive token rewards from the protocol for ongoing development. But unlike centralized exchanges, it does not need to maintain fiat banking channels, large compliance teams, regional subsidiaries, customer support, or extensive custody and funding operations. Once a DEX is live, the only ongoing fixed cost is a small fee paid to validators in the form of token inflation. For example, the total estimated monthly cost of running a Hyperliquid validator is around $10,000, which is almost negligible compared to Hyperliquid's $1 billion in annualized revenue.

In fact, as user acquisition, localization, and asset onboarding become increasingly outsourced to third-party front-end and ecosystem builders, the protocol itself can scale more or less at zero marginal cost like software. This means that once a DEX reaches escape velocity, it possesses tremendous operational leverage. In extreme cases, a sufficiently mature DEX may even require no direct payments to any team at all. Instead, third-party teams would maintain the core protocol through open-source contributions while deriving revenue from the businesses they build on top of the exchange. At this point, such a DEX would operate with nearly 100% net profit margins.

Most importantly, perpetual decentralized exchanges will exhibit compounding advantages as they scale. As liquidity deepens, the quality of clearing improves. Improved clearing outcomes support tighter margin requirements and higher capital efficiency. Higher capital efficiency and stronger solvency guarantees enhance user confidence and attract more liquidity. Over time, we believe this dynamic will lead to a winner-takes-all outcome in the industry, with capital accumulating in the places where risk management is most effective.

The Quiet Power of Trust

"Not your keys, not your coins."

"Don't trust, verify."

These maxims circulate in every crypto cycle, warning newcomers of the dangers of trusting centralized counterparties. For a long time, due to the challenges of building decentralized exchanges mentioned earlier, trading cryptocurrencies without centralized intermediaries was impossible. Therefore, the history of the crypto economy is littered with exchange collapses from Mt. Gox to FTX.

Although decentralization is often viewed as a philosophical commitment of blockchain, in practice, blockchain applications provide users with substantively lower counterparty risk. Unlike CEXs, which are essentially opaque closed systems, DEXs offer users irrevocable rights enforced by code.

For the use case of perpetual contracts, this means users can check margin logic, funding rate mechanisms, liquidation rules, and exchange solvency in real-time, rather than relying on broker assurances or post-hoc interventions. We believe this is extremely important, as even years after the collapse of FTX, CEXs continue to erode user trust due to opaque withdrawal controls and opaque internal risk management failures. Furthermore, similar transparency and governance failures are not unique to the crypto space but are common in the broader closed financial system.

Ultimately, financial markets are confidence systems. When rules are clear and enforcement is mechanized, traders are more willing to participate. This is the structural advantage of DEXs. By providing users with maximum transparency, auditability, and backup guarantees (for example, Lighter offers users the ability to withdraw collateral back to the Ethereum mainnet at any time), users face lower counterparty risks. Under equal conditions, this should make users more willing to use DEXs while providing regulators with a strong basis for differentiation from offshore centralized exchanges.

The Path to Hundreds of Billions

"Younger/newer companies are pioneering new markets, and it’s easy to underestimate their potential market size. Is Uber or Lyft replacing taxis, or redefining car ownership?" ------ Philippe Lafont

Today, leading decentralized perpetual exchanges have a fully diluted market capitalization of less than $40 billion. Outside the cryptocurrency space, the total market capitalization of the largest publicly traded exchanges and brokerage firms exceeds $1 trillion. We believe the perpetual decentralized exchange industry can penetrate and even meaningfully expand this total pie. To reiterate, our argument is built on three core assumptions about the perpetual decentralized exchange industry:

Perpetual contracts can be created for any asset with a clear price oracle.

Perpetual contracts can capture a significant share of traditional futures and options trading volume, especially in retail-driven market segments.

DEXs have structural advantages over centralized counterparts and will continue to lead the growth of the new asset class perpetual contract industry.

Assessing the Opportunity Size

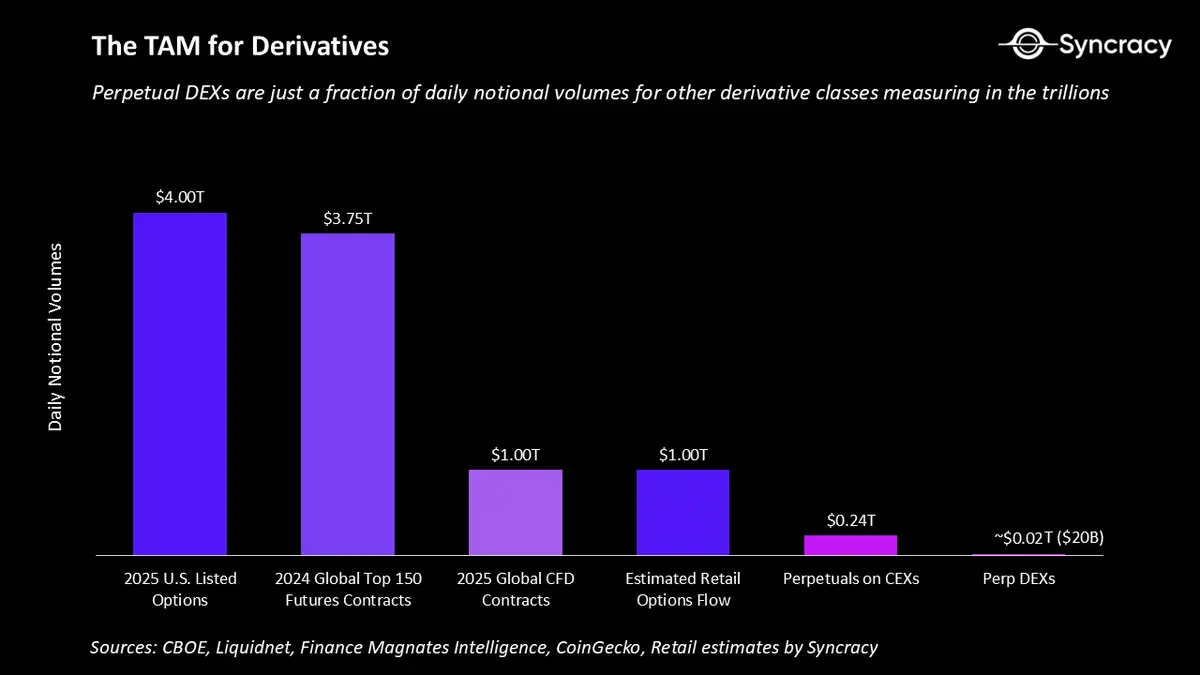

Today, given the scale of centralized exchanges, decentralized exchanges represent only a small fraction of the total trading volume of crypto perpetual contracts.

Compared to the broader global derivatives market, they are essentially negligible. The nominal trading volume generated daily by the options, futures, and contracts for difference markets exceeds $80 trillion, while perpetual DEXs account for only $20 billion.

Of course, not all of this flow can be captured. However, we do believe that in the coming years, short-term options and the global CFD market present a realistic opportunity for these exchanges. As mentioned, as these products become more accessible, retail participation in these markets will only increase, and perpetual contracts represent an elegant alternative for retail traders and their desire for leverage. The scale of this opportunity cannot be overstated. For example, even capturing just 20% of the retail options flow we estimate (which is 5% of total options trading volume) would expand the entire perpetual DEX market tenfold.

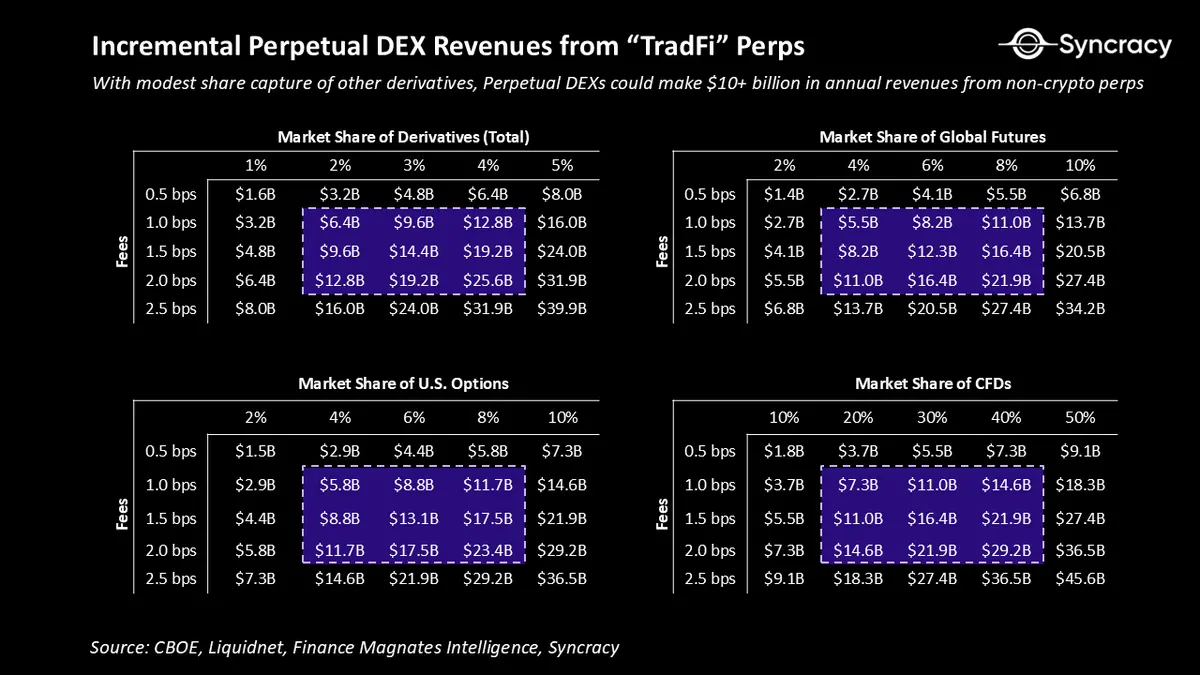

Even capturing a modest market share would have a massive revenue impact. The table above illustrates the annual fee opportunities under different possible fee rates and market penetration rates in the global derivatives market. At effective rates of 1-2 basis points, capturing just 1% of derivatives trading volume could translate to approximately $3-7 billion in annual revenue. If market share reaches 2-4%, the opportunity will rapidly grow to hundreds of billions of dollars. Remember, as mentioned above, perpetual DEXs have incredible profit turnover capabilities, so you can consider these revenues as more or less profit.

The conclusion here is that perpetual DEXs do not need to monopolize global trading to become extremely valuable enterprises. Even with low single-digit penetration rates in these terminal markets, it is sufficient to significantly revalue their expected business outcomes. We believe the scale of the retail speculation funnel is sufficient to accommodate this initial capture rate.

As a benchmark, on January 30, during a day of record volatility in metals, Hyperliquid captured about 2% of the global silver derivatives trading volume while providing competitive spreads for retail traders. Maintaining this level of performance across different assets and market regimes is no easy feat, but early traction is encouraging.

If our vision is long enough, as perpetual contracts develop, traditional fixed-term futures may revert to their original purpose of hedging long-term exposure to physically delivered assets. In today’s major contracts, a significant portion of futures trading volume is driven by traders speculating on direction, arbitrage, or volatility rather than producers or companies hedging operational risks. Data from the CFTC across asset classes indicates that over half (possibly close to 80%) of futures activity is speculative rather than commercial.

If perpetual contracts can replicate the economic risk exposures of these contracts while providing continuous trading, simpler contract designs, and unified cross-asset margining, they will have a structural advantage for speculative share. In that case, fixed-term futures will still be essential for managing real-world risk exposures for commodity producers, airlines, and banks, while perpetual contracts will grow to become the contract type dominated by speculation. Considering this end state, there exists a difficult yet plausible path to achieving double-digit penetration rates across the entire derivatives market.

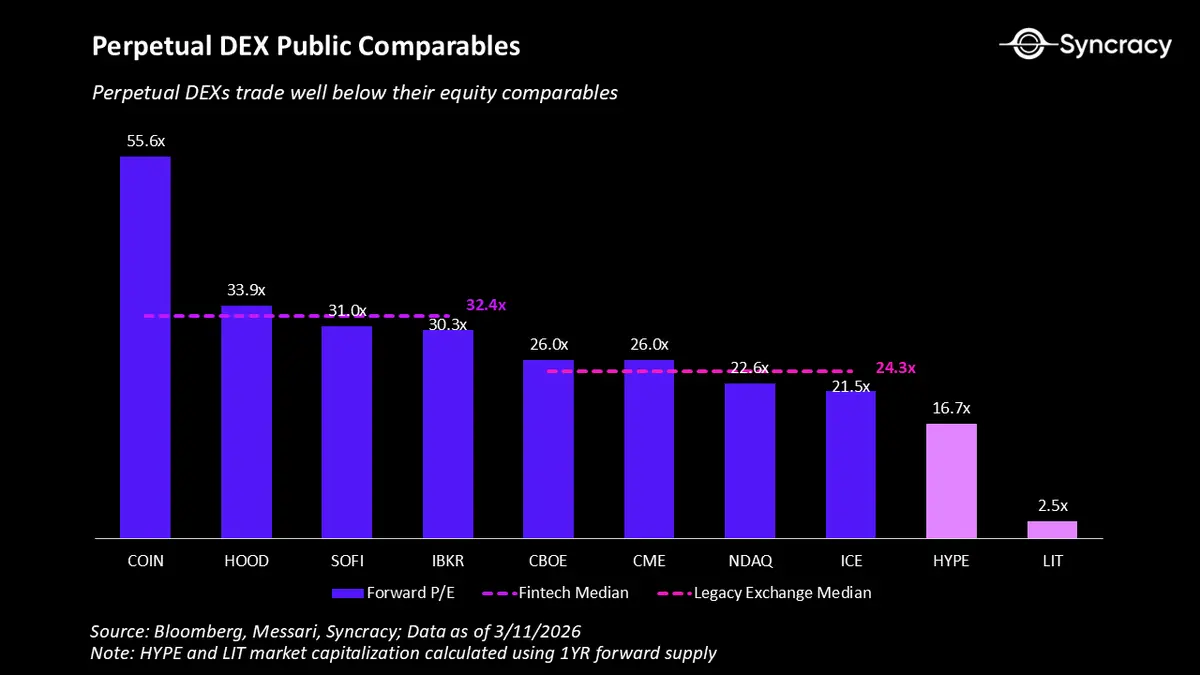

We believe the market has yet to recognize this potential and the long-term competitiveness of decentralized perpetual exchanges. The price-to-earnings ratios of the two market leaders, Hyperliquid and Lighter, are just 17x and 3x, respectively, far below their fintech and traditional exchange peers. Below, we quantify this opportunity using the aforementioned peer multiples and our estimated industry profits for 2030 derived from the analysis above.

As noted, it takes only a small amount to make the numbers large. Nevertheless, it is worth noting that all of the above analysis is U.S.-centric and assumes no growth in total derivatives trading volume in the future. Considering the overall global derivatives trading volume and the larger audience brought by 24/7 trading should meaningfully expand this potential target market.

The Endgame Exchange—Perpetual Contracts as a Trojan Horse

Finally, it must be emphasized that the endgame for perpetual DEXs is not merely to replicate existing derivatives markets more efficiently but to comprehensively expand the scope of derivatives markets. Through initiatives like HIP-4, Hyperliquid can natively support adjacent products such as prediction markets and options within the same unified system. Combined with portfolio margining mechanisms, this opens the door to an endgame exchange architecture that far exceeds the capital efficiency and expressiveness of today’s fragmented traditional stacks.

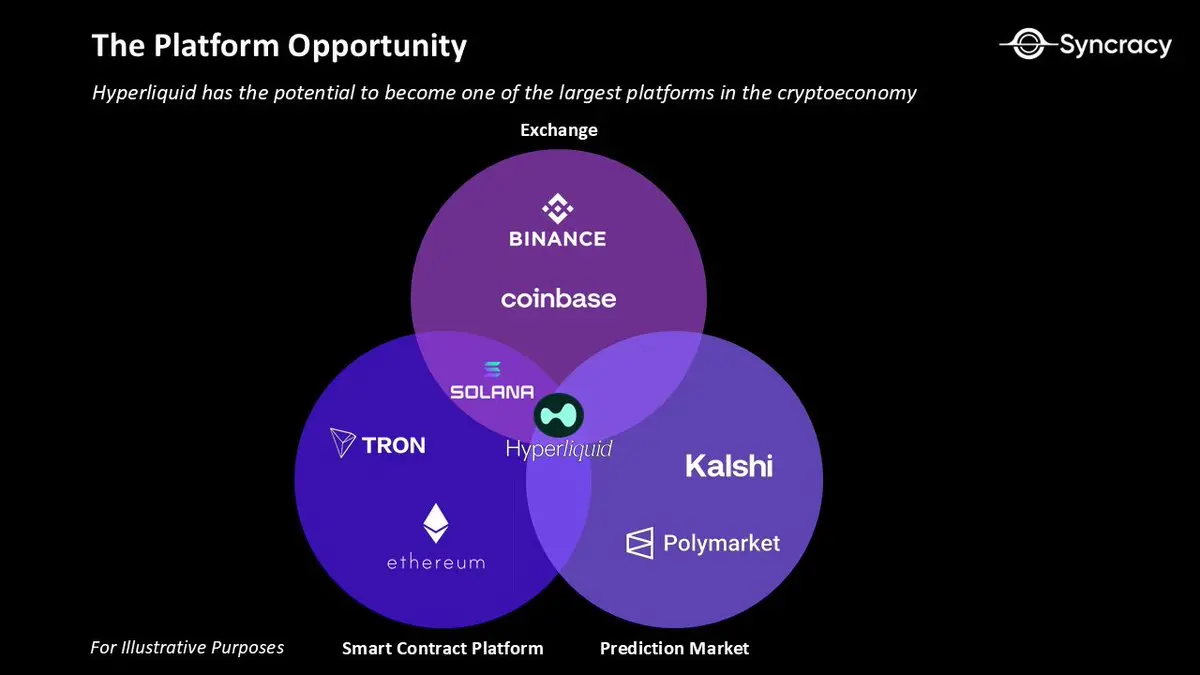

Platform Opportunities

At this point, it should be evident how profitable perpetual contracts can be for blockchains. The data alone indicates this, as Hyperliquid is the highest revenue-generating blockchain in the world. Less obvious, but almost equally important, is that perpetual contracts are one of the hardest use cases to build on blockchains; once they are nailed down, all other use cases on the blockchain become easier to "layer on."

As detailed above, historically, blockchains have been rife with microstructural weaknesses, including high latency, adverse selection, and limited throughput, making it infeasible to build perpetual contracts. Many of these issues, while critical for use cases like payments and spot trading, are not existential. For example, latency and throughput issues may mean stablecoin transfers do not arrive immediately, but that does not mean you ultimately won’t get your money. In contrast, a perpetual exchange that cannot clear collateral quickly enough will become insolvent.

As leading perpetual DEXs solve these issues, it is no surprise that they are beginning to expand into new domains. Hyperliquid and Lighter have both launched spot markets and EVM sidecars in the past year, allowing them to offer products available on general platforms like Ethereum and Solana. During the same period, Hyperliquid launched its own branded stablecoin through a community-driven process. Recently, it announced HIP-4, providing foundational building blocks for prediction markets and options trading on Hyperliquid. The synergies between these use cases are exciting and best illustrated through a hypothetical scenario.

In the future, as more assets are tokenized on Hyperliquid, you can imagine a world where you can use any basket of assets as collateral margin to create any synthetic exposure. For example, you are bullish on the depreciation of the dollar and AI infrastructure and hold a concentrated portfolio consisting of Bitcoin, gold, and tokenized stocks of Nvidia, SK Hynix, and TSMC. You use it as collateral to short a software stock index because you believe these companies are doomed in the age of agent coding.

With a native options market, you can hedge your liquidation levels through rolling expiration contracts. Given your outstanding performance, you start offering portfolio management services through a vault that anyone can access, is real-time auditable, and is self-custodied. A user deposits stablecoins into this vault from a privacy pool on a connected EVM sidecar. That user discovered this opportunity through a brand-new social trading interface built around all on-chain transparent financial data. All of this activity occurs within a single, global, permissionless system.

This is where the endgame exchange becomes something beyond a traditional exchange. Any venue that can gather these primitives under one roof can achieve incremental growth that is greater than the sum of its parts.

There are many steps to achieve this future. But the core idea is that when assets share a flowing ledger, financial activity will experience a Cambrian explosion. Following this, we believe that if perpetual DEXs successfully seize this platform opportunity, they can achieve results on par with Solana or Ethereum and, in the long run, break the trillion-dollar barrier.

Connecting Everything

If you’ve made it this far, congratulations. With the information above, your understanding of the opportunity of perpetual contracts now exceeds that of 99.9999% of people on Earth. To many, perpetual contracts may seem like a financial tool that arose purely from the industry's thirst for endless speculation, but they may ultimately become one of the most important innovations to emerge in the crypto economy. This innovation may one day be listed alongside digital gold, stablecoins, and prediction markets as the "Mount Rushmore" of the industry.

The evidence is in the data. Perpetual contracts not only have a clear path to growing into a dominant derivative tool within the expanding crypto economy, but they also possess distinct advantages over options and futures that will enable them to absorb a larger share of retail demand for traditional asset classes. In the first few months of the perpetual contract "real-world asset" expansion, they have already begun to impact global financial markets, recently serving as a price discovery engine for crude oil during the weekend of the Iran conflict. We believe that over time, the primacy of perpetual contracts will only become more apparent.

In this process, we believe that decentralized exchanges like Hyperliquid will continue to capture market share from centralized exchanges like Binance and Coinbase. Hyperliquid is already the clear leader in the stock and commodity perpetual contract space, which has become a clear harbinger of future trends. Decentralized exchanges possess structural advantages through self-custody, real-time auditability, permissionless construction, and global accessibility. These features will enable them to outperform centralized exchanges in the long run. Additionally, due to regulatory and structural incompatibilities, traditional exchange enterprises like the Chicago Mercantile Exchange and Intercontinental Exchange will face years of being unable to compete.

Finally, as decentralized exchanges lead the growth of perpetual contracts, we believe they will also expand into adjacent categories. Perpetual contracts are the hardest product to land on blockchains, and once blockchains can successfully host them, they will naturally begin to aggregate other crypto use cases as a byproduct. We have already seen early evidence of this, as Hyperliquid has expanded into spot trading and stablecoins, and soon into prediction markets and options. In this sense, perpetual decentralized exchanges are also the Trojan horse for future financial platforms.

Of course, there will be growing pains along the way. There is still no clear regulatory clarity for DEXs. Decentralized perpetual exchanges will need to fine-tune their risk management engines, including optimizing automatic liquidation mechanisms to explore incremental insurance funds. Over time, they will also need to reduce funding costs and gap risks in traditional markets. However, we believe these are merely details and not factors that will break the argument; the most important thing is to stay accurate on the direction of the trend rather than quarreling over obstacles along the way.

We ultimately believe that blockchains are natural monopolists, possessing strong network effects formed around liquidity, integration, security, and developers. As they scale, these networks become digital superstructures composed of interconnected assets, applications, enterprises, and users that cannot be easily replicated or imitated. As mentioned, the potential target market can credibly be measured in trillions of dollars, and the prize for the winning blockchain that accommodates perpetual contracts will be one of the largest achievements in the global financial realm.

While perpetual contracts may seem to have come a long way in the decade since their invention, the fact is that this category is still just a grain of sand on the beach of global finance.

Yet, that is precisely why it is all so exciting.

The great perpetualization has only just begun.

Important Legal Disclaimer This publication is for informational purposes only and does not constitute investment advice, nor is it an offer to sell or solicit the purchase of any securities or investment products. All investments involve risks, including the potential loss of principal. Past performance does not guarantee future results. Any forward-looking statements or hypothetical examples are subject to risks and uncertainties and do not constitute guarantees of future performance. This material does not create any client-advisor relationship. The company assumes no responsibility for the accuracy or completeness of third-party information mentioned herein. Any recommendations or endorsements comply with the disclosure requirements regarding compensation and conflicts of interest in the U.S. Securities and Exchange Commission's marketing rules. The company maintains records of all supporting statements in accordance with regulatory obligations. All content is protected by intellectual property laws and may not be reproduced or distributed without permission.

Risk warning

Risk warning