In-depth Exploration: The Evolution of Decentralized Lending: From Monolithic Capital Pools to Unified Liquidity Layers and Agnostic Primitives

The evolution of the decentralized finance (DeFi) lending market not only reflects the iteration of technology but also mirrors the eternal trade-offs between capital efficiency, risk control, and cross-chain interoperability in DeFi protocols. The DeFi lending market in 2026 is highly likely to evolve into a dual oligopoly of Aave and Morpho. The former occupies the "retail and standardized institutional market," while the latter occupies the "geek, customized, and high-efficiency arbitrage market."

The evolution of the decentralized finance (DeFi) lending market not only reflects the iteration of technology but also mirrors the eternal trade-offs between capital efficiency, risk control, and cross-chain interoperability in DeFi protocols. The DeFi lending market in 2026 is highly likely to evolve into a dual oligopoly of Aave and Morpho. The former occupies the "retail and standardized institutional market," while the latter occupies the "geek, customized, and high-efficiency arbitrage market."Deepcoin Research is a research brand launched by Deepcoin, focusing on market trends, trading behaviors, and industry structure research in the cryptocurrency sector. By continuously publishing research reports and data insights, it provides a deeper market understanding for the industry.

Executive Summary

The decentralized finance (DeFi) lending market has undergone a profound architectural revolution over the past five years. From the initial peer-to-peer (P2P) attempts to the establishment of the "Monolithic Pool" model represented by Aave and Compound, and now to the differentiation towards the "Unified Liquidity Layer" and "Agnostic Primitive," this evolution reflects not only the iteration of technology but also the eternal trade-offs that DeFi protocols face between capital efficiency, risk control, and cross-chain interoperability.

This report aims to thoroughly outline the evolution of DeFi lending protocols, focusing on the architectural leap from Aave v1 to v4, particularly how version 4 attempts to address liquidity fragmentation in the multi-chain era through a "Hub-and-Spoke" architecture. At the same time, we will deeply compare the drastic shift in risk control philosophy between Compound v2 and v3 (Comet), explaining why it transitioned from a "pooled risk" to an "isolated risk" single-coin lending model. Through empirical data analysis from three dimensions—governance efficiency, token economics, and TVL capture ability—we will demonstrate how Aave achieved overwhelming victory in its competition with Compound. Finally, the report will explore the new forces represented by Morpho Blue, analyzing how its "Agnostic Primitive" design philosophy challenges traditional DAO governance lending models and reshapes the yield curve of DeFi.

1. Evolution of Protocols: Aave's Architectural Evolution Panorama (v1 to v4)

The history of Aave reflects the journey of DeFi lending from "primitive tribes" to "modern financial infrastructure." Each version iteration essentially corrects the inefficiencies in capital utilization and rigid risk management of the previous generation architecture.

1.1 Aave v1: Paradigm Shift from P2P to Pool Model (2020)

Before being renamed Aave, the project operated under the name ETHLend, adopting a peer-to-peer (P2P) lending model. In the P2P model, borrowers and lenders must completely match on loan amount, interest rate, term, and collateral type to complete a transaction. This model resulted in extremely high friction costs and very low liquidity matching efficiency, with funds often lying idle and a poor user experience.

The launch of Aave v1 in January 2020 marked the entry of DeFi lending into the "Pooled Liquidity" era.

- Breakthrough in Smart Contract Logic: Aave v1 introduced the concept of a "shared liquidity pool." Depositors no longer needed to find specific borrowers but instead deposited assets into a smart contract (pool) and received aTokens representing their deposit share. Borrowers could directly withdraw liquidity from the pool and pay interest dynamically calculated by an algorithm based on the utilization rate.

- Initial Improvement in Capital Utilization: This model achieved "instant liquidity," completely eliminating matching wait times. Although, by modern standards, v1's capital efficiency was still limited by static risk parameters, it solved the core issues of "cold start" and "liquidity matching."

- Interest Tokenization (aToken): v1 innovatively introduced aToken, a derivative token pegged 1:1 to the underlying asset, with interest reflected directly through balance growth. This allowed the deposit certificates to have liquidity themselves, which could be used in other DeFi protocols, achieving initial composability in DeFi.

1.2 Aave v2: Financialization and Instant Leverage (End of 2020)

If v1 addressed the question of "whether," Aave v2 tackled the question of "how well it works," pushing the protocol towards high financialization.

- Standardization of Flash Loans: Although flash loans were not originally created by Aave v2, v2 standardized and promoted them on a large scale. This feature allows developers to borrow the entire liquidity of the pool without collateral, provided that the principal and fees are repaid within the same transaction (Block). This technological breakthrough greatly enhanced the efficiency of the DeFi market, democratizing arbitrage and liquidation, and providing the protocol with a stream of risk-free fee income.

- Debt Tokenization and Credit Delegation: v2 also tokenized debt positions, enabling "credit delegation." Depositors could delegate their borrowing limits to other addresses (even uncollateralized institutions), laying the groundwork for subsequent institutional lending and uncollateralized credit.

- Collateral Swapping and Repayment Optimization: v2 allowed users to swap collateral directly without closing debt positions or use collateral to repay debts. This was achieved through a mechanism called "Flash Liquidation," significantly lowering the operational threshold and Gas fees for users during market volatility.

1.3 Aave v3: Refined Risk Control and Cross-Chain Prototype (2022)

The release of Aave v3 was set against the backdrop of the explosion of multi-chain ecosystems. To efficiently deploy on Layer 2 (such as Arbitrum, Optimism) and sidechains (Polygon), v3 made minimally invasive innovations in capital efficiency and risk isolation.

- Efficiency Mode (E-Mode): This was the biggest breakthrough in capital utilization for v3. In v2, lending parameters (LTV) were set individually for assets, ignoring the correlations between assets. v3's E-Mode allows highly correlated assets to be grouped (for example: USDC/DAI/USDT belong to the stablecoin category, ETH/stETH/wstETH belong to the Ethereum category). Within the same category, LTV can reach 97%-98%. This means users can conduct forex-level high-leverage arbitrage (for example, cyclically borrowing stETH/ETH to earn staking rewards) at very low capital costs, greatly releasing capital potential.

- Isolation Mode: To address the difficulty of listing "long-tail assets," v3 allows new assets to be listed in "isolation mode." Users can use these higher-risk assets as collateral but can only borrow specific stablecoins, with a debt ceiling set. This establishes a firewall at the smart contract level, preventing price manipulation attacks on a single long-tail asset from causing the entire protocol to collapse.

- Portal: Although seamless cross-chain functionality was not fully realized, v3's Portal feature allows governance-approved bridging protocols to destroy aTokens on the source chain and mint aTokens on the target chain, enabling liquidity cross-chain roaming. This laid the theoretical foundation for v4's unified liquidity layer.

2. Aave v4: Redefining Infrastructure with Unified Liquidity Layer

Expected Release: Q4 2025 / 2026

Aave v4 is not just an upgrade; it is a complete reconstruction of the underlying architecture of DeFi lending. In response to the industry's pain point of multi-chain liquidity fragmentation, v4 proposes the concept of a "Unified Liquidity Layer," attempting to end the status quo of "chains as islands."

2.1 Core Architectural Breakthrough: Hub-and-Spoke Model

In versions v3 and earlier, Aave's deployment on each chain (and even different markets on the same chain, such as Core and Prime) was independent. USDC on Ethereum could not be immediately utilized for borrowing needs on Arbitrum, leading to idle funds and inefficient interest rates. Aave v4 addresses this issue through the Hub-and-Spoke architecture.

- Liquidity Hub:

- Functional Positioning: The Hub is the heart of the v4 architecture, acting as a central bank for the entire network (Per Network) or even cross-network. It centrally stores all assets, manages core accounting, and oversees solvency but does not directly handle user lending interactions.

- Smart Contract Logic: The Hub employs a share-based system to track liquidity, simplifying the interest accumulation calculation logic, making it more compliant with the ERC-4626 standard, and facilitating integration with other DeFi protocols.

- Modular Spokes:

- Functional Positioning: The Spoke serves as the interface for user interactions and the carrier of specific business logic. Each Spoke can represent an independent lending market (such as RWA market, institutional market, long-tail asset market).

- Dynamic Credit Lines: The Spoke itself does not hold large amounts of liquidity but "wholesales" funds from the Hub based on the dynamic credit line granted by the Hub, then retails to users. This completely solves the "cold start" problem when launching new markets—newly launched Spokes can directly utilize the existing billions of dollars in liquidity from the Hub without starting from scratch to attract deposits.

- Risk Isolation: Each Spoke can have independent risk parameters (LTV, liquidation threshold, oracle source). If a high-risk Spoke experiences bad debts, the Hub can isolate it through a pre-set "debt ceiling" in the smart contract, preventing risk from spreading to the core Hub and other Spokes.

2.2 Technical Breakthrough in Cross-Chain Liquidity Management: CCLL and CCIP

2.2 Technical Breakthrough in Cross-Chain Liquidity Management: CCLL and CCIP

Aave v4 attempts to build a Cross-Chain Liquidity Layer (CCLL), with its core technological pillar being Chainlink's Cross-Chain Interoperability Protocol (CCIP).

- Superfluid Capital: The vision of v4 is to allow users to manage all positions across chains from a single interface (Unified Account). Users can deposit wBTC on Ethereum and instantly borrow USDC on Arbitrum without manually bridging assets across chains.

- Technical Implementation Logic:

- GHO Stablecoin: For Aave's native stablecoin GHO, v4 utilizes CCIP's "Burn and Mint" mechanism. The Hub can authorize the Spoke on the target chain to directly mint GHO to lend to users while recording liabilities on the source chain ledger. This makes cross-chain borrowing of GHO atomic and zero-slippage.

- Non-Native Assets: For assets like USDC or ETH, the Hub synchronizes the "liquidity status" across the network through CCIP's messaging layer. While physical assets may move through "Lock and Release" or liquidity pool rebalancing, from an accounting perspective, the Hub allows Spokes to issue loans based on the total liquidity of the entire network. This design attempts to transform cross-chain operations from "asset transportation" to "credit accounting," significantly reducing user wait times and operational thresholds.

2.3 Fuzzy Logic and Dynamic Interest Rates

To further squeeze capital efficiency, Aave v4 introduces dynamic interest rate curves (sometimes referred to as Fuzzy Logic).

- Adaptive Mechanism: Traditional interest rate curves (Kink point) are static and require governance voting to modify. v4's smart contracts include automatic adjustment logic: if the utilization rate remains above the optimal point for an extended period, the curve slope will automatically steepen to attract deposits or suppress borrowing; conversely, it will flatten. This mechanism allows the protocol to automatically adjust its metabolism based on market supply and demand, like a living organism, without manual intervention.

3. AAVE Strategic Pillars for 2026

3.1 Horizon: Institutional RWA Bridge

- Specifically targeting the real-world asset (RWA) market, allowing qualified institutions to collateralize tokenized U.S. Treasury bonds and other credit assets to borrow stablecoins.

- Currently, net deposits are approximately $550 million, with a target to expand to over $1 billion by 2026. Partners include top financial institutions such as Circle, Ripple, Franklin Templeton, and VanEck.

3.2 Aave App: The "Trojan Horse" for Millions of Users

- A flagship mobile application designed to shield users from the underlying complexities of DeFi. By integrating Push, it provides a zero-fee stablecoin deposit and withdrawal channel globally, bringing the Aave protocol to millions of mainstream mobile payment users.

4. Comparative Analysis: Divergence in Risk Control Philosophy between Compound v2 and v3

While Aave adds features through addition, another giant in DeFi lending, Compound, chose subtraction in its v3 (Comet) version, a decision that profoundly reflects its fear of systemic risk.

4.1 Compound v2: Pooled-Risk Model

Compound v2 adopts a classic many-to-many lending model, similar to Aave v2.

- Mechanism: Users can deposit any supported asset (such as UNI, LINK, WBTC) and borrow any other asset. All assets are mixed in a large liquidity pool.

- Fatal Flaw (Barrel Effect): The security of this model depends on the "weakest collateral." If a small market cap collateral (such as BAT or ZRX) in the pool suffers from an oracle attack or infinite minting attack, hackers can deposit a large amount of these falsely valued tokens and borrow all the hard currency (USDC, ETH) in the pool. This means that users depositing USDC effectively bear the tail risk of all the altcoins in the pool. This systemic risk increases exponentially with the number of supported assets.

4.2 Compound v3: Single-Coin Lending and Risk Isolation (Base Asset Model)

Compound v3 (codenamed Comet) is a complete denial of the v2 model, shifting to a single base asset model.

- Single Borrowable Asset: In a Comet market (for example, the USDC market), users can only borrow one asset (the base asset USDC). Other assets (WBTC, ETH, UNI, etc.) can only be deposited as collateral and cannot be borrowed.

- Why the Shift?

- Protecting Lenders: In the USDC market, lenders only deposit USDC. Since attackers cannot borrow other collateral, even if a collateral (such as UNI) goes to zero, attackers can only borrow a certain proportion of USDC. Although the protocol may incur bad debts, it will not result in the catastrophic outcome of "the entire pool being emptied." Risks in different markets are physically isolated (the risk of the USDC market does not affect the WETH market).

- Trade-off in Capital Efficiency: For borrowers, v3 is highly attractive because it allows "unified collateral"—borrowing one currency with multiple collaterals, and borrowing interest is lower (due to a lower risk premium). However, for suppliers of collateral, v3 is extremely inefficient because deposited WBTC or ETH as collateral cannot earn interest (since they cannot be borrowed). Compound bets that most of the demand in DeFi is for "collateralizing volatile assets to borrow stablecoins."

4.3 Differences in Liquidation Mechanisms: Public Auctions vs. Protocol Absorption

The liquidation logic of both reflects the trade-off between efficiency and fairness.

Compound v2 (and most protocols): Dutch/English Auction

When a user falls below the liquidation line, external liquidators (Bots) compete to repay debts and obtain collateral. This relies on on-chain liquidity and the capital size of liquidators. In times of market volatility or extremely high Gas fees, liquidation may fail, leading to bad debts.

Compound v3: Absorption and Storefront Price

v3 introduces a liquidation method more akin to traditional banks.

- Protocol Absorption: When an account defaults, the protocol directly absorbs all collateral and debt of that account. At this point, the borrower's balance is zeroed.

- Reserve Payout: The protocol uses its own reserves to instantly repay bad debts. This prevents panic selling.

- Collateral Resale: The collateral held by the protocol is then sold to liquidators at a "Storefront Price Factor." This is a fixed discount rate (for example, 94% or 95%), allowing liquidators to purchase collateral from the protocol at this discounted price without waiting for an auction process. This mechanism reduces the risk of market-wide cascading collapses by having the protocol act as the "last buyer" and "buffer."

5. The Outcome is Clear: An In-Depth Analysis of Aave's Victory over Compound

Although Compound initiated the liquidity mining era in 2020, Aave has established an absolute dominant position in the competition of 2024-2025. Data shows that Aave's TVL has surpassed $40 billion (once reaching $55 billion), while Compound hovers in the $2-3 billion range.

5.1 Governance Speed: Agile Development vs. Code as Law

- Compound (Conservative): Compound's governance philosophy is "minimize governance" and "code as law." Its governance process is extremely slow, with proposals often requiring weeks of review and long timelocks of several days. While this ensures "robustness," it also causes it to miss the window of opportunity for Layer 2 explosion. For example, Compound's speed in deploying to Arbitrum and Base is much slower than Aave, leading to a loss of first-mover advantage in the new ecosystem.

- Aave (Radical): Aave is effectively driven by a company with strong execution capabilities (Aave Labs / BGD Labs) and a highly active governance agency (Aave Chan Initiative, ACI). ACI, as a professional governance representative, greatly accelerates the speed of proposal drafting, voting, and execution. Aave is often among the first mainstream protocols to support new chains (such as Avalanche, Polygon, Scroll), and this "blitzkrieg" strategy allows it to quickly monopolize liquidity in new chains.

5.2 Token Model and Value Capture: GHO vs. COMP

- COMP (Value-less Governance): The COMP token has long been seen as a "value-less governance token." The massive interest income generated by the Compound protocol is primarily allocated to reserves, and COMP holders cannot directly benefit from the protocol's growth aside from voting rights. Although the community has discussed the "Fee Switch" multiple times, progress has been slow and contentious during the 2024-2025 period (such as the "golden child" Humpy governance attack incident).

- AAVE & GHO (Monetary Minting Rights): Aave empowers its tokens in multiple dimensions.

- Safety Module: Users staking AAVE can earn safety incentives, but this will serve as insurance payouts in extreme cases.

- GHO Stablecoin: This is Aave's trump card. By minting GHO, the Aave DAO not only captures lending interest but also captures "seigniorage." The interest paid by borrowers on GHO goes 100% to the DAO, rather than to depositors like USDC. This allows Aave to evolve from a pure intermediary platform into a decentralized central bank, greatly enhancing the protocol's revenue ceiling.

5.3 TVL Capture Ability: Dimensionality Reduction of Product Matrix

Aave attracts a wide range of users from retail to institutional by continuously launching new features (flash loans, E-Mode, isolation mode). In contrast, while Compound v3 is secure, its product form is too singular (only suitable for users borrowing USDC). Aave v4 further clarifies its ambition for RWA (Real World Assets), connecting tokenized U.S. Treasury bonds with institutions like BlackRock through dedicated Spokes, allowing Aave to capture trillions of traditional financial liquidity outside of DeFi, while Compound lags in this area.

5.4 Current Dominance of Aave

- Absolute Market Share Leader (2025 Data): Aave holds 59% of the DeFi lending market share and accounts for 61% of the total active loan volume across the entire sector.

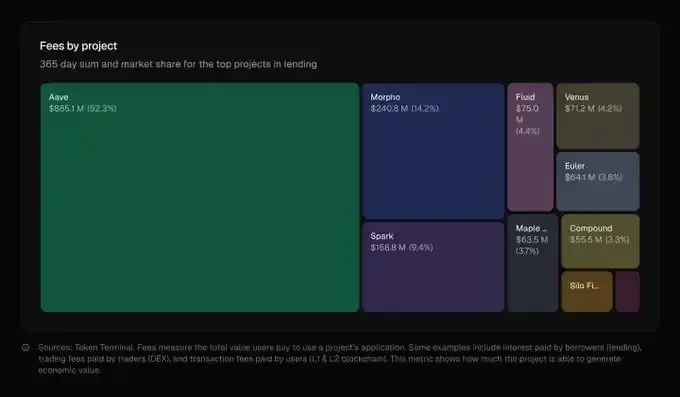

- Remarkable Financial Performance: In 2025, the protocol's fee income reached $885 million (accounting for 52% of total fees from lending protocols), even exceeding the combined total of its next five competitors.

- Volume Comparison: Its net deposit size once reached $75 billion, making it large enough to rank among the top 50 banks in the United States.

6. Analysis of New Forces: Morpho Blue and the Challenge of Agnostic Primitives

As Aave attempts to build a "unified bank" through v4, Morpho Blue challenges it with a completely opposite philosophy.

6.1 Design Philosophy: Agnostic Primitive vs. Monolithic Pool

- Inefficiency of Monolithic Pools: In the monolithic pools of Aave and Compound, the DAO must assess the risk of each asset. For safety, the DAO often sets conservative parameters (low LTV, high spreads). This means that those wanting to borrow WBTC and those wanting to borrow altcoins are in the same pool, leading to averaged capital utilization and significant spreads—the loss between the interest paid by borrowers and the interest received by depositors.

- Morpho Blue's Agnosticism: Morpho Blue is designed as an immutable, minimal piece of code (only 650 lines of Solidity). It does not know what constitutes a "good asset" or a "bad asset," nor does it rely on the DAO for risk parameter voting.

- It allows anyone to create a lending pair (Market): consisting of one collateral (like wstETH) and one loan asset (like USDC).

- Parameter Agnosticism: Creators only need to specify the liquidation LTV (LLTV) and oracle address. The Morpho Blue protocol itself does not impose restrictions based on asset risk.

- Significance: This design separates "risk management" from the protocol layer and delegates it to the market. It eliminates the bottleneck of DAO governance and theoretically supports an infinite variety of long-tail assets.

6.2 Challenge Mechanism: MetaMorpho Vaults Restructuring Credit Layers

If users were to choose where to deposit money among hundreds or thousands of Morpho Blue markets, the experience would be disastrous. Morpho's solution is MetaMorpho Vaults.

- Specialized Division of Risk Management: MetaMorpho is an aggregation layer built on Morpho Blue. Professional risk management institutions (Curators) like Steakhouse, Gauntlet, or B.Protocol can open a "USDC Vault."

- Operational Model: Users simply deposit USDC into the "Steakhouse USDC Vault," as easy as depositing into Aave. But behind this vault, the Steakhouse team dynamically allocates funds to different underlying markets in Morpho Blue based on algorithms (for example, 90% allocated to the wstETH/USDC market, 10% to the RWA/USDC market).

- Competitive Advantage: This creates a survival of the fittest risk management market. If Aave's risk parameters are poorly set, users have no choice. But in Morpho, if the Steakhouse vault yields low or incurs bad debts, users can immediately switch to Gauntlet's vault. This competition forces spreads to compress significantly, and Morpho often offers higher deposit rates and lower borrowing rates than Aave.

6.3 Market Penetration: From Optimizer to Infrastructure

By the end of 2025, Morpho's data growth is astonishing.

- TVL Surge: Morpho Blue's TVL has surpassed $3.9 billion, and it has substantially replaced Compound on Ethereum and Base chains. In certain niche markets (like wstETH collateral borrowing), Morpho's liquidity depth even exceeds that of Aave.

- Penetration Strategy: Morpho initially started as an "optimizer" for Aave/Compound, siphoning liquidity from the two major protocols. Now, it is becoming the preferred venue for institutions and whales to conduct "carry trades" by providing higher capital efficiency (utilization rates of 80%-90% vs. Aave's 40%-50%).

7. Conclusion: The Final Battle for DeFi Credit

The evolution of DeFi lending presents two clear paths:

- Aave v4 (Superbank Path): Moving towards vertical integration. Through Hub-and-Spoke and the unified liquidity layer, Aave attempts to incorporate all chains, all assets, and all users into its closed ecosystem. It relies on a strong brand and DAO governance to provide "one-stop" security services. Aave bets that users and institutions trust a "too big to fail" unified brand and a vast liquidity moat.

- Morpho (Infrastructure Path): Moving towards horizontal layering. Morpho Blue commodifies the underlying ledger and marketizes risk management through MetaMorpho. It does not aim to become a bank but rather to become the settlement system underlying banks (TCP/IP). Morpho bets that capital will always seek profit, and more efficient market structures will ultimately replace inefficient monolithic intermediaries.

- Compound (Conservative Retreat): In this race for innovation, Compound v3 seems to retreat into an extremely risk-averse "Treasury bond-level" yield tool. While safe, its market share in the battle for liquidity hegemony among DeFi protocols is likely to be further divided by Aave and Morpho.

Final Outlook:

The DeFi lending market in 2026 is likely to evolve into a duopoly between Aave and Morpho. The former occupies the "retail and standardized institutional market," while the latter captures the "geek, customized, and high-efficiency arbitrage market."

Risk warning

Risk warning![[In-depth] The Awakening of Sovereign Agency: From the Local Revolution of OpenClaw to the Financial Framework of Silicon-based Society](https://public.chaincatcher.com/upload/image/20260409/1775710083342-317845.webp)