BitMEX Founder: The Brutal Drop Has Not Broken the Spirit of the Bull Market

The crypto capital market is the last free financial market on Earth. Support levels: Bitcoin at $28,500, Ethereum at $1,700.

The crypto capital market is the last free financial market on Earth. Support levels: Bitcoin at $28,500, Ethereum at $1,700.Author: Arthur Hayes

Original Title: 《Bottomless》

Translation: Wu Zhuocheng, Wu Says Blockchain

Three weeks ago, I wrote an article titled 《混乱局面》 (Maelstrom), in which I described a thought process that rationalized my cryptocurrency asset portfolio, namely holding only Bitcoin, Ethereum, and a few altcoins I believe in.

While many appreciated my candor and perspective, some correctly pointed out that my bearish article was published weeks after Bitcoin and Ethereum had fallen more than 30% from their ATH. This is my essay, and I hope it is persuasive, supported by logic and evidence. I am not here to help you time the market accurately, but to challenge your views; I hope to help you grow as a trader or investor.

The crypto capital market is the last free financial market on Earth. All other major asset classes and the intermediaries that help people trade these products have become political targets for governments and central bank officials. "When a measure becomes a target, it ceases to be a good measure" — Goodhart's Law.

The stock, fixed income, and foreign exchange markets are deeply influenced by central banks and those "too big to fail" banks. This means they can run infinite leverage on the backs of taxpayers, with the consequence of inflation caused by reckless money printing. The balance sheets of these banks are used to fix asset prices at levels that achieve political balance. This benefits the wealthy, as ownership of financial assets is highly concentrated among the richest 10% or even 1% of citizens in any society.

Cryptographic assets exist entirely outside the TradFi system, and therefore will find a market clearing level before stocks or bonds. Crypto assets are now a true asset class traded by ordinary people like us, hedge fund masters, and a few sell-side banks. As the last truly free financial market, crypto assets will find a clearing price reflecting the current macroeconomic environment's ups and downs earlier than all other assets.

My belief in the above perspective has led me to a dilemma.

In the first three weeks of this year, the crypto asset market fell sharply. The U.S. stock market — the S&P 500 and the Nasdaq 100 — is slightly below its historical highs. The stock market has certainly not entered a true bear market yet. However, the capital losses experienced by crypto asset holders indicate that the Federal Reserve's cancellation of dollar liquidity in a new round of fighting inflation will hit index holders in the short term.

That's fine. But the Federal Reserve hasn't even stopped buying bonds or raised policy rates. If I wait until the market predicts the Fed will raise rates at the March meeting, will it be too greedy and cause me to miss an excellent entry point to exchange dirty fiat for clean crypto assets? I cannot deny that if Bitcoin trades below $30,000 and Ethereum below $2,000, my finger on the buy button would be very excited. But does this impatience align with the probability map of the future in my mind?

This article attempts to give people more flexibility in deciding when to bottom-fish.

Last week, the U.S. president held a press conference alone and confidently stated that controlling inflation is the Fed's responsibility. Whether or not you believe the Fed is 100% responsible for high inflation in the U.S. and can act with their policy levers, the Fed must raise interest rates policy-wise. The Fed will never make a 100% commitment to any policy; they always leave room to change their minds in the event of significant occurrences in the financial markets.

The question becomes: Can the Fed publicly change its future restrictive monetary policy before the March meeting? At the March meeting, everyone expects the Fed to raise policy rates by 0.25%. Here are three scenarios in which the Fed might change its policy direction:

The S&P 500 and Nasdaq 100 indices fall at least 30% from their historical highs (S&P 500 at 3,357 points, Nasdaq 100 at 11,601 points).

A collapse of the U.S. Treasury or money market.

A significant widening of spreads between investment-grade and speculative-grade bonds.

I have elaborated on the importance of the first and second points to the economic model of the U.S. and even the global economy. It is widely believed that if either of these scenarios occurs, the Fed may restart the money printing machine against the political will of the ruling party. What is less discussed is the corporate credit sector, mainly because everyone believes that the Fed solved this issue when it nationalized the market in March 2020.

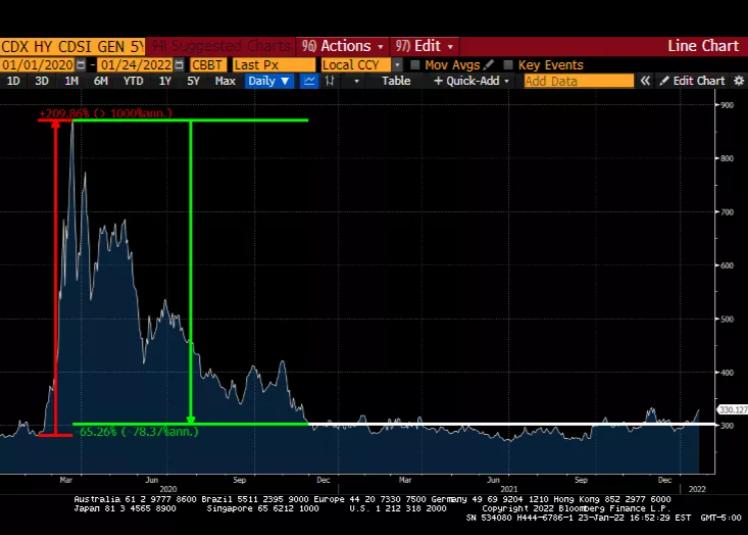

The Fed nationalized the U.S. corporate bond market by supporting all investment-grade bonds and stating that it could purchase speculative-grade bonds. The following two charts show how nationalization has squeezed CDS spreads. CDS spreads are a good indicator of how much interest a company with a certain rating must pay to issue bonds.

Speculative-grade basis points

Investment-grade basis points

Faced with a pandemic of unknown severity (the red shaded area), the market began to demand high interest rates from corporate borrowers. The Fed said "no, no, no, no," the market's level is wrong — let’s nationalize it by providing infinite money printing. Thus, spreads decreased, and large companies maintained loose borrowing conditions. Unfortunately, for small businesses, they cannot access the institutional credit market, so they are left out. It was only recently that the market began to consolidate.

If the Fed publicly states it will reduce the size of its balance sheet, how can it maintain its commitment to support corporate bond issuance? This support must involve purchasing or threatening to purchase all eligible corporate bonds as defined by the Fed. The market has become aware of this inconsistency, and yields have begun to rise slightly.

This is a problem because by 2022, approximately $332.42 billion worth of non-financial U.S. corporate bonds will mature (source: Bloomberg). Companies must either use cash on hand to repay investors or issue new debt to repay old debt. Based on 2021's issuance statistics (source: SIFMA), the total amount of debt that must be rolled over accounts for 17% of the annual total debt.

Few companies have pricing power to offset the negative effects of wage and commodity inflation, which will inevitably lead to margin contraction. Therefore, as inflation continues to ravage the U.S. and the world, the free cash flow used to repay bondholders will decrease. If the Fed does not actively suppress spreads by expanding its balance sheet, the market will demand higher rates for newly issued bonds.

For the Fed, the most terrifying scenario is that the market anticipates tightening monetary policy and demands increasingly higher rates for corporate bonds. If companies cannot finance themselves, they will reduce activity, which means unemployment at a politically very inconvenient time. Inflation does not necessarily mean someone will lose their job, but if a company cannot finance itself due to market-required rates, it will lay off employees.

I believe that politically, a 7% unemployment rate is worse than a 7% inflation rate. The Fed and their political brokers may soon be forced to choose between continuing inflation or facing a wave of unemployment after a credit market collapse. I bet that loose monetary policy will return, which, as we know, is positive for the crypto market. Market conditions change very quickly; if the market believes the Fed will not support corporate bond issuance, spreads will widen rapidly.

This strategy is not to wait for the Fed to publicly announce a change of heart, but to use the signals provided by these indices as signs of an impending turn. Crypto assets will capture these signals and rise before the Fed publicly announces its policy changes.

Support levels: Bitcoin $28,500, Ethereum $1,700.

I believe the market will not bottom out before these levels are retested. If the support levels hold, that would be great; the issue would be resolved. If not, then I believe Bitcoin and Ethereum could drop to $20,000 and $1,300 due to liquidation. As for Bitcoin and Ethereum breaking below the 2017 ATH (which are $20,000 and $1,400 respectively), I don't even want to consider that scenario.

It is also possible that Bitcoin and Ethereum will not drop below $30,000 and $2,000 again, and the market will never develop as expected. In that case, the market would not have explicitly tested previous lows, which could become tricky. Depending on your ideological perspective on capital markets, you might look at one or more statistics such as: total open interest in contracts, net inflows of stablecoins to exchanges, asset sizes on specific exchanges, implied volatility versus actual volatility, etc.

One can imagine a scenario where Bitcoin and Ethereum hold the current trend channel's bottom when the Fed turns on the tap, but I am sure that is impossible. We must think more flexibly about which signals will instill confidence in us so that we can buy, buy, buy.

But as I write this article, the market is bottomless. The traditional market has not yet scared the Fed enough to stop inflation. In terms of price action, in my years of experience as a participant in the crypto capital market, sell-offs come in waves. Although this past weekend was brutal, it did not break the spirit of the bull market.

Remember, marginal sellers determine price. If their bond and stock portfolios are hit, those institutions holding a small amount of crypto assets will not hesitate to dump them. They have not yet started selling (they are off work on weekends), and the negative headlines from mainstream financial media have not provided the confirmation bias these sellers need to cope with the downside volatility of crypto assets. Correlation is coming, but it has not yet arrived. If the S&P 500 and Nasdaq continue to decline at the end of the quarter, be careful; is it tied to a pillar with an Hermès tie, or nailed to the ground with Louboutin high heels…

Sell the soaring assets to avoid further declines.

Risk warning

Risk warning Risk warning

Risk warning