"On-chain Federal Reserve" urgently raises interest rates! Maker launches DAI defense battle?

Why did DSR and multiple core vaults significantly adjust interest rates, and what impacts will Maker and the DeFi market face?

Why did DSR and multiple core vaults significantly adjust interest rates, and what impacts will Maker and the DeFi market face?Written by: ImperiumPaper

Compiled by: Frank, Foresight News

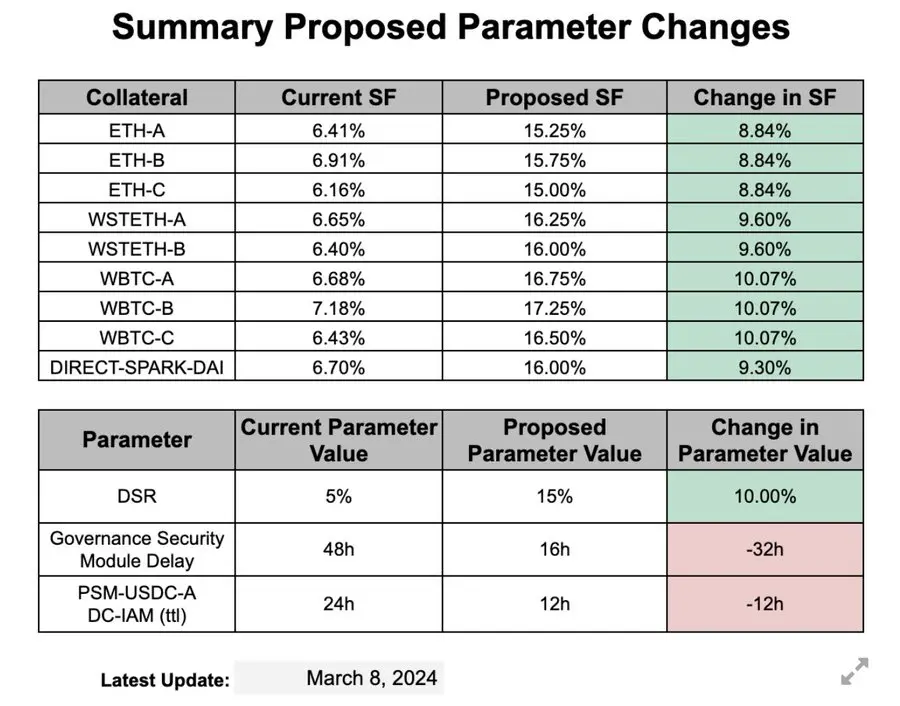

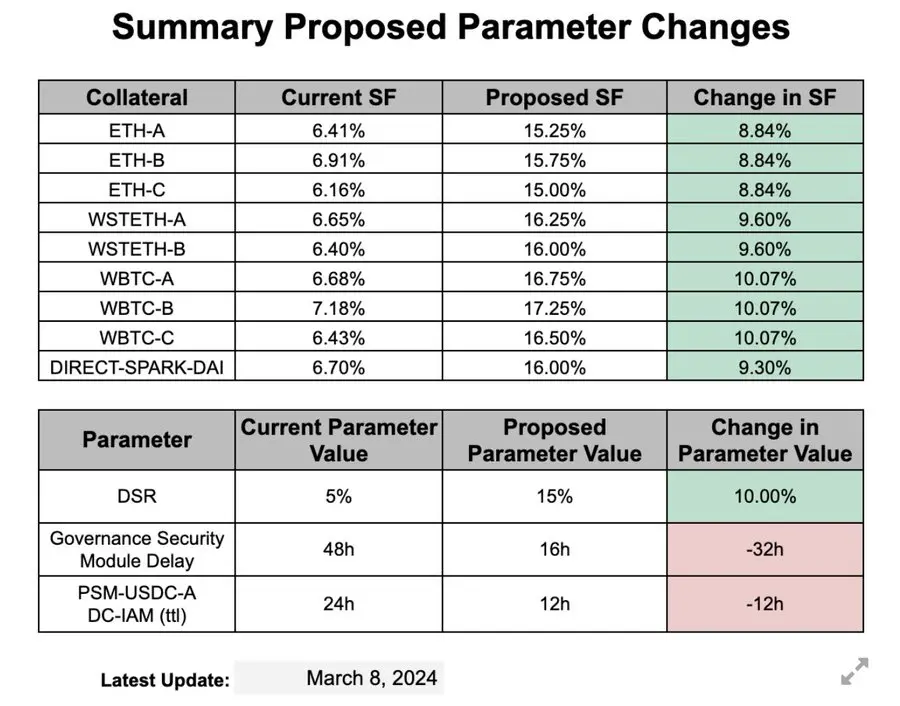

Editor’s Note: On March 11, MakerDAO made a series of adjustments to the stability fees of several core vaults, including DAI savings rates, ETH, and WBTC. This article aims to briefly analyze the reasons behind these changes and their potential impacts.

To get straight to the point, MakerDAO's Peg Stability Module (PSM) experienced a significant outflow of DAI funds last week. Although the outflow is currently at a reasonable level, Maker was forced to liquidate treasury bill reserves (tbills) and withdraw USDC stored in Coinbase Custody cold wallets to respond, with over $900 million injected into the PSM so far.

It is important to note that while MakerDAO did not specifically mention this, it has hinted that treasury bill reserves (tbills) have been gradually reduced over the past three months.

The "Exchange Rate Stability" Dilemma Faced by Maker

Roughly speaking, the reason for the DAI outflow is that MakerDAO and Spark's borrowing rates are lower than their peers.

It should be clarified that the Atlas protocol sets the interest rates of Maker's money market based on different formulas, but these formulas ultimately tie back to the interest rates of 3-month U.S. Treasury bills (T-bills) (Foresight News note: the Atlas protocol is the fundamental rule set governing MakerDAO).

In short, the system interest rates of MakerDAO ultimately depend on the interest rates of 3-month U.S. Treasury bills. For more details, you can search for "Yield Collateral Benchmark."

This further implies that as the overall DeFi market interest rates rise relative to traditional finance (TradFi), MakerDAO's DAI interest rates have not timely reflected the increase in borrowing costs (Foresight News note: that is, DAI's interest rates have not been adjusted upward in a timely manner).

In a floating exchange rate scenario, this misalignment can lead to inflation. However, for a currency that maintains a fixed exchange rate (i.e., DAI), to maintain the 1:1 peg with the U.S. dollar, the system needs to use foreign exchange reserves (USDC) to intervene in the market to ensure the peg.

But the problem is that Maker's hands are tied— as mentioned above, it cannot flexibly adjust because its rates are determined by U.S. Treasury rates. For those unfamiliar with how MakerDAO operates, Maker's "end game" is to strictly adhere to the Atlas protocol while meeting weekly to study the implications of Atlas, making even minor rule changes very difficult, leading to a continuous accumulation of pressure that disconnects it from DeFi market interest rates.

Until last week, the situation took a sharp turn—the USDC reserves in the PSM were only 26 minutes away from depletion at one point. At this time, Richard Heart also sold over 300 million DAI to purchase a large amount of ETH. Although MakerDAO still holds $1 billion in U.S. Treasury reserves, the inability to receive wire transfers over the weekend made the situation unpredictable, putting immense pressure on MakerDAO.

Against this backdrop, the BA Labs team proposed an emergency rate adjustment, and I think they would also acknowledge that this approach is somewhat extreme (Foresight News note: BA Labs submitted a comprehensive proposal on March 9 to increase various rates related to DAI).

But please note that from a political perspective, there is no feasible path to continuously raise interest rates.

How to View the Measures Taken by Maker

Alright, the analysis of the reasons is complete; now let's look at the underlying logic:

- Raise interest rates to encourage DAI repayment - preferably by converting USDC into DAI for repayment;

- Raise the DSR (DAI Savings Rate) to encourage holding DAI - similarly, it is best for users to operate in the PSM;

These measures are relatively straightforward.

We can also analyze the potential consequences; note that the following content is speculative:

Raising borrowing rates is a traditional and correct measure; however, the execution of such a large one-time adjustment to the rates is debatable. At least I believe this move could lead to market volatility, though it might not.

Regarding the DSR rate, I hold reservations because this adjustment feels somewhat rushed. I believe it would be better to wait until both borrowing parties adapt to the new rates and assess the actual yields before making more careful adjustments.

Combining CHAI/sDAI as collateral and features like Blast integration, I think there is no need to set the DSR so high (i.e., 15%), meaning the adjustment of the DSR rate is overly aggressive.

I have been in the crypto space longer than most participants, and from a historical perspective, many currencies that maintain a fixed exchange rate have suffered severe blows for not following market interest rates. Therefore, while MakerDAO correctly corrects by raising borrowing rates, I think they may have made the same mistake regarding the DSR rate.

This overall feels somewhat like Thailand/Indonesia/Philippines in 1997, or Mexico in 1994, as MakerDAO's DSR rate increase feels like an expansionary monetary policy, but unlike the Federal Reserve—because the DSR can easily be re-collateralized, thereby reducing borrowing costs.

Risk warning Risk warning

Risk warning Risk warning