AI infrastructure surged throughout Q1, but by Q2, who can still support the "high valuation"?

In Q1, the market lifted the entire chain of AI infrastructure, and by Q2, it will start reconciling segment by segment, company by company.

In Q1, the market lifted the entire chain of AI infrastructure, and by Q2, it will start reconciling segment by segment, company by company.Written by: DaiDai, MSX

Previously, MSX released a comprehensive preview titled “Oil Prices Soar, Interest Rates Hard to Lower, Seven Sisters at Rest: What Main Lines to Watch for Excess Returns in Q2 U.S. Stocks?”, systematically sorting out the overall market main lines for Q2. Following this framework, it becomes clear that the AI market in U.S. stocks in Q1 is no longer just about whether "the leading chip companies are rising."

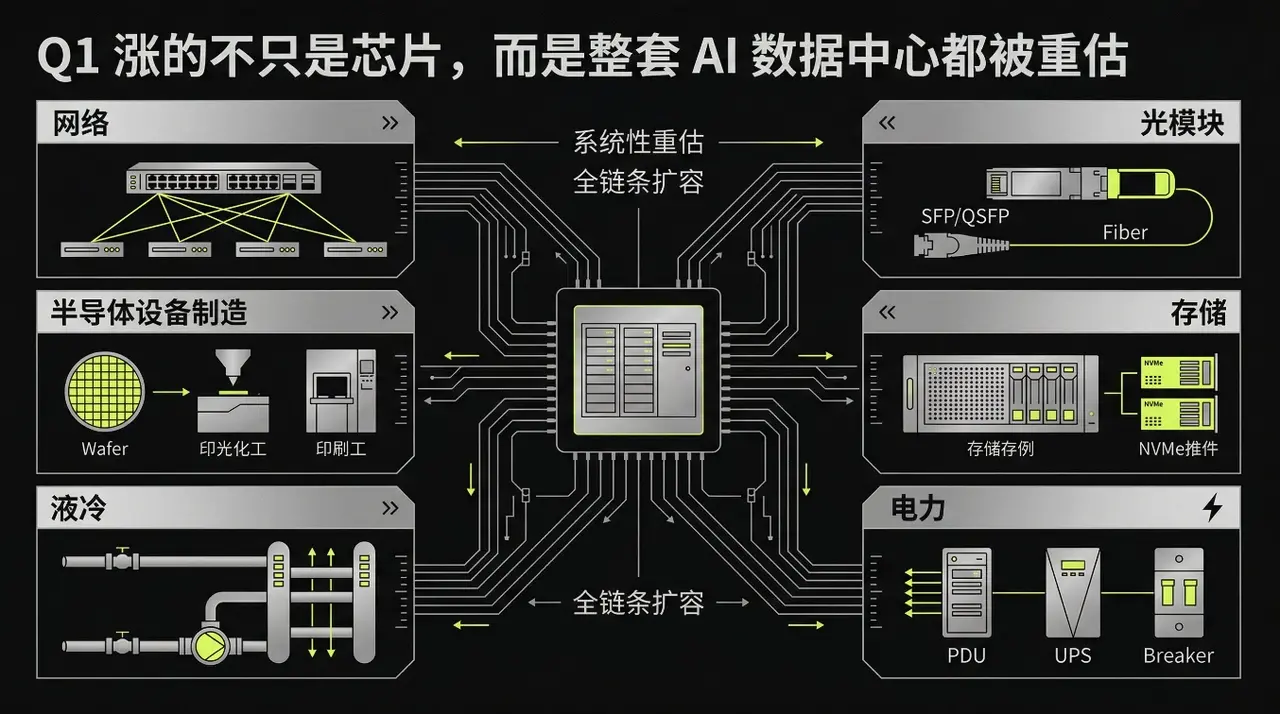

In the view of MSX Research Institute, it is not just a few companies around GPUs that are rising, but the entire data center: there is a need to expand machine rooms, increase bandwidth, supplement power supply, implement liquid cooling, and push production capacity forward.

Therefore, in Q2, the main line remains unchanged, but the market rhythm will change.

Among them, networking, optics, storage, power, and equipment manufacturing are still on the main line, but the subsequent trend will not simply be about raising valuations along the entire "AI infrastructure" chain, but will focus more on whether orders, deliveries, profits, and capex can meet expectations.

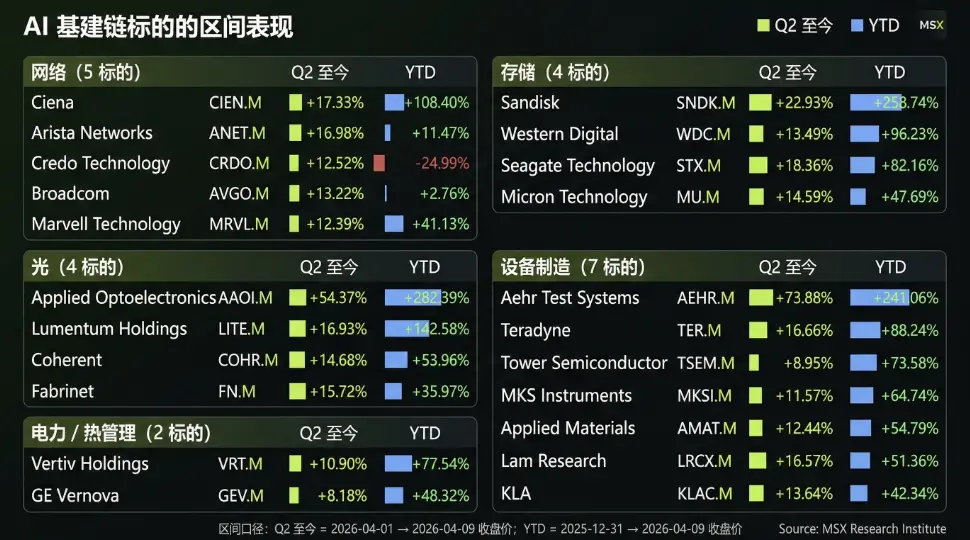

From the performance range, the strongest elasticity since Q2 has been AEHR.M and AAOI.M; in terms of YTD, AAOI.M, SNDK.M, AEHR.M, and LITE.M have seen more significant increases, clearly indicating that there has been a noticeable differentiation within the AI infrastructure chain.

I. In Q1, it was not about buying a specific company, but the entire data center needed expansion

The most obvious point in the Q1 market is that after the funds were invested, they no longer focused on single-point chips. Chips are certainly still the entry point, but what truly consumes capital expenditure is the entire data center. As long as hyperscalers continue to increase capex, money will follow the path of "what is still needed for AI implementation."

From the perspective of the asset pool on the MSX platform, this main line already has a relatively clear trading mapping.

The first to strengthen is networking. AI clusters are not a competition of single-machine computing power; they compete in interconnectivity, bandwidth, and latency. Leaders like ANET.M naturally stand at the forefront, while CRDO.M and MRVL.M focus on key aspects around interconnectivity and accelerators. Names like AVGO.M, which combine chip and connectivity capabilities, will also be lifted by the market; CIEN.M, although more focused on the outer circle of network infrastructure, cannot be completely bypassed as long as cross-machine room transmission and data handling continue to increase. Once the cluster grows larger, networking is no longer a supporting role but a legitimate expenditure item.

Next is optics. As AI training and inference move towards higher density, optical modules and related components are more likely to be brought to the forefront. LITE.M, COHR.M, AAOI.M, and FN.M were repeatedly categorized together in Q1, with a straightforward logic: bandwidth needs to increase, interconnectivity needs to upgrade, and specifications need to move higher. In the previous phase, the market was not in a hurry to distinguish who would win or lose, but first raised the valuation of "specification upgrades." Who is at 800G, who is at 1.6T, and who can achieve higher-end shipments—these differences were initially set aside.

Storage has also been reclassified. MU.M, WDC.M, STX.M, and SNDK.M were previously viewed more as cyclical stocks, but in the Q1 market, funds have begun to push them towards the "AI infrastructure chain." The reason is not hard to understand: as models grow larger, data increases, and training becomes more frequent, memory and storage are no longer just based on the old logic of PCs and smartphones. At least at the trading level, the market is willing to re-evaluate these companies within the framework of "data center expansion."

Following that are power and thermal management. Typical beneficiaries like VRT.M, which focus on "power supply + cabinets + supporting," and names like GEV.M, which are more focused on power equipment and grid direction, may not always be in the hottest positions in Q1, but they have also been lifted by funds. After all, while computing power can be packed into machine rooms, the sources of electricity, how heat dissipates, and whether deliveries keep up all need to be accounted for. Once the density of data centers increases, these issues cannot be avoided.

Equipment manufacturing has also kept pace. LRCX.M, KLAC.M, AMAT.M, MKSI.M, TER.M, TSEM.M, and AEHR.M in this line have more expectations of "expansion will continue to pass down" in Q1. Advanced processes, storage, packaging and testing, yield management, production line automation, and testing verification, once included in the framework of "AI expansion's next step," will see valuations pushed upwards.

Thus, the rise in Q1 was not due to one or two companies surging individually, but rather the entire chain being lifted together. The market first recognized one thing: data centers need expansion. The subsequent networking, optics, storage, power, thermal management, and equipment manufacturing were all put on the table.

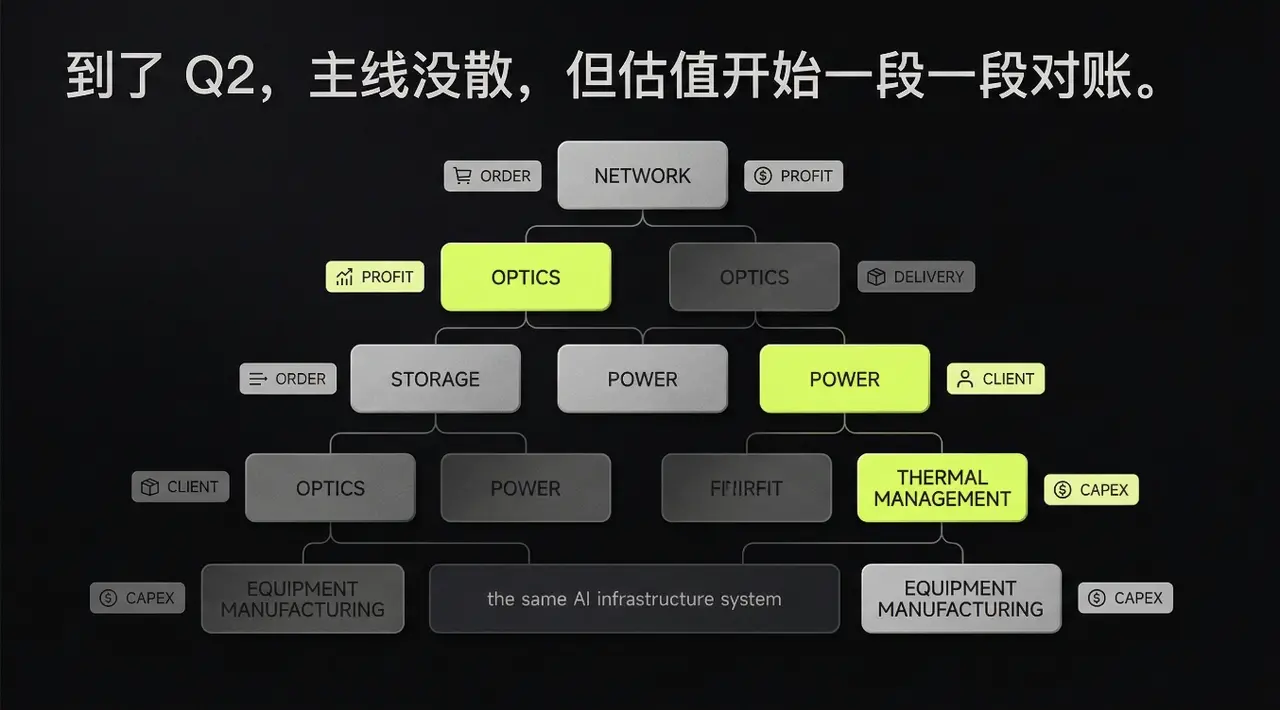

II. By Q2, the main line remains, but valuations begin to reconcile in segments

The issue in Q2 is not that the AI narrative suddenly disappeared, but that the first round of "lifting valuations across the entire chain" has already passed. There will be further increases, but they will not be as orderly as before.

The networking and optics chains in Q1 benefited from expectations of high bandwidth, interconnect upgrades, and cluster expansions. By Q2, these expectations will not disappear but will be broken down for calculation. Names like ANET.M, which have clearer customer bases and steadier product rhythms, will be closely watched for whether order strength can continue; companies like CRDO.M, MRVL.M, and AVGO.M, which are key players in interconnectivity and computing power, will see the market start to inquire about customer structures, shipment rhythms, and revenue recognition; names like CIEN.M, which are more focused on network infrastructure, will see more attention on new orders, delivery cycles, and project advancements in Q2, making it unlikely to continue enjoying premiums along with the entire chain.

The optics chain is more likely to widen the gap. Because while both discuss specification upgrades, the underlying customers, capacities, yields, and price pressures are not the same. LITE.M, COHR.M, AAOI.M, and FN.M could rise together before, but in Q2, the market will start to reconcile: who has more stable customers, who has smoother shipments, and who can retain profits. The previous phase relied on "everyone buying together along the optics chain," while the latter phase will focus on who can sustain the expectations.

The storage side will be more complicated. In Q1, the market was willing to give MU.M, WDC.M, STX.M, and SNDK.M a more "AI-driven" pricing, but by Q2, the focus will shift to questioning: how solid is this round of demand, can profit recovery keep up, or is it just another cyclical rebound in disguise? As long as prices, bit shipments, and profits can rise in sync, funds will continue to support valuations; once the reports are not strong enough, the pullback will be direct. The biggest fear for the storage line is being treated as an AI infrastructure stock and then being pushed back to cyclical stocks.

Power, thermal management, and equipment manufacturing will be easier to assess in Q2 based on fundamentals. They may not always be in the hottest discussions, but when it comes time for reconciliation, delivery, expansion, order visibility, and gross margins become clearer. The order and delivery rhythm of VRT.M and the broader power equipment cycle of GEV.M will be compared against hyperscalers' expansion plans. On the equipment manufacturing side, LRCX.M, KLAC.M, AMAT.M, MKSI.M, TER.M, TSEM.M, and AEHR.M will also be closely watched by the market: can AI expansion continue to pass down, can testing verification, production line rhythms, and final deliveries keep up, or will it only stop at the upstream investments?

Initially, the market bought in segments, but later it will need to look at each company individually. The main line remains, but valuations will no longer move together.

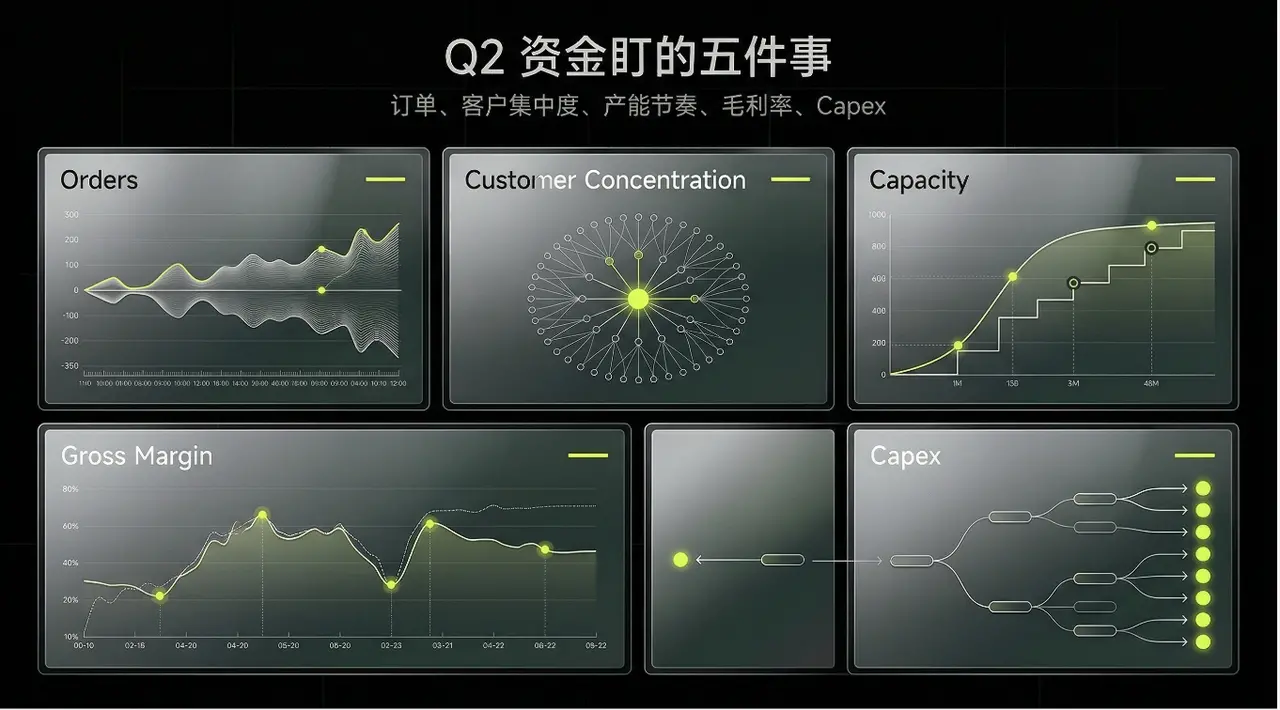

III. In Q2, funds will focus on five things to pin high expectations to the reports

First, look at orders. The networking chain is usually the first to be reconciled: are orders still piling up, is delivery still speeding up, and has customer procurement transitioned from trial orders to regular orders? Typical beneficiaries like ANET.M will be repeatedly monitored for whether order strength can continue; companies like CRDO.M, MRVL.M, and AVGO.M, which are key players in interconnectivity and computing power, will also be watched for more visible projects and clearer shipment guidance.

Next, look at customer concentration. The optics chain especially cannot escape this issue. The more concentrated the customers, the easier it is for Q1 to rise quickly; by Q2, if one major customer slows down, stock prices often react to the financial reports first. For the group of LITE.M, COHR.M, AAOI.M, and FN.M, the market will pay more attention to who the customers are, what their proportions are, and how the rhythm goes, rather than using the phrase "bandwidth upgrade" to smooth out all fluctuations.

Third, look at capacity rhythms. In Q1, many companies talked about "strong demand," but in Q2, funds are more concerned with "can you produce it, can you deliver it." The optics chain will look at the climb, while power and thermal management will look at delivery, and equipment manufacturing will focus on the rhythm of orders turning into shipments. Delivery-oriented targets like VRT.M will often be revalued by the market at this stage: as long as delivery is stable, expectations are not easily dispersed. The same goes for the line of LRCX.M, KLAC.M, AMAT.M, MKSI.M, TER.M, TSEM.M, and AEHR.M: demand must truly pass down, and ultimately it all falls on production lines, testing verification, and delivery.

Fourth, look at gross margins. When raising valuations in Q1, the market was willing to set aside the profit statement; by Q2, it will start to be picky. The line of MU.M, WDC.M, STX.M, and SNDK.M is the most typical: strong demand is one thing, but whether profits can keep up is another. Prices have risen, but costs have also increased, or competition has pushed profits back down, and valuations will drop accordingly. The optics and networking chains are the same; specification upgrades do not automatically mean profit upgrades. Those who can turn higher-end shipments into higher gross margins will be more stable.

Finally, still look at hyperscalers' capital expenditures. In Q1, the market assumed "large companies will continue to invest," but in Q2, it will be more concerned with "where to invest, what to invest in first, and whether budgets have shifted." As long as capex remains high, there is still work to be done along this chain; but once the structure of capex changes, the order of beneficiaries will also change, and differentiation will come quickly. If training shifts towards inference, the rhythm of networking and optics will change; if the pace of data center expansions changes, the ordering of power, thermal management, and equipment manufacturing will also shift.

Overall, when capturing opportunities in these sector rotations, the core is not in prediction, but in being able to act quickly when signals appear. Currently, the market is focusing on the aerospace sector, and the ongoing Commercial Aerospace Trading Week by MSX provides a good entry point. For traders interested in participating in the 10,000 USDT prize pool incentive and the sector, it is also a practical opportunity to reduce friction costs.

Conclusion

In Q1, the entire chain rose first, but by Q2, the market will start to reconcile in segments. Networking, optics, storage, power, and equipment manufacturing will no longer move together; those whose orders land first, whose deliveries keep up, and whose profits materialize first will be more likely to maintain their valuations.

Reflected in the tradable targets on the MSX platform, this main line already has a relatively complete observation framework, and MSX will continue to track the evolution of this main line and the rhythm of related targets.

Risk warning

Risk warning

Popular articles