The tokenomics design based on reflexivity is unsustainable; DeFi needs structural changes

The lack of patience and long-term commitment is one of the most obvious problems in DeFi, and the current bear market is an excellent opportunity to reflect on existing flaws and propose new designs.

The lack of patience and long-term commitment is one of the most obvious problems in DeFi, and the current bear market is an excellent opportunity to reflect on existing flaws and propose new designs.Author: Cristiano

Compiled by: Beichen, Chain Teahouse

Do you enjoy staying up late to ponder the dilemmas of causality?

For example, the grandfather paradox. Suppose you travel back in time and kill your grandfather before your father is born; without your grandfather, there would be no father, and without a father, there would be no you. So who killed your grandfather? Or does your existence imply that your grandfather did not die because of you, so how could you kill your grandfather?

If you also enjoy DeFi, then you must love thinking about how the causal relationship between token prices and protocol revenues unfolds.

So please grab a cup of coffee, sit back comfortably, and let me explain the intricate reflexivity in DeFi.

What is Reflexivity?

According to Wikipedia, "Reflexivity refers to the circular relationship between cause and effect." Furthermore, "The reflexive relationship is bidirectional, meaning that causes and effects influence each other, so it is impossible to designate a cause or an effect."

The concept of "reflexivity" captures a well-known phenomenon in science and human behavior, with the most exquisite examples found in the works of the Dutch artist Escher, who was obsessed with geometry and paradoxes.

The image titled "Drawing Hands" clearly illustrates how reflexivity works: it is impossible to determine which hand is drawing the other. The causal relationship is so tight that it cannot be distinguished.

Speaking of art and reflexivity, the DeFi community has also created some powerful memes to express the concept of reflexivity within the community.

How to Identify Reflexivity in Projects?

In DeFi, reflexivity is also known as circularity or the famous flywheel effect. When conducting due diligence on projects, we can assess the degree of reflexivity by asking the following questions:

What determines the appreciation/depreciation of the native token price?

What does the appreciation/depreciation of the native token price mean for the operation of the project?

If the answers to these questions are the same (or largely overlap), then reflexivity exists.

To some extent, reflexivity exists in every good business model, but the way it propagates from one event to another makes the world different. We can categorize it into "indirect" and "direct" reflexivity.

Indirect Reflexivity

Indirect reflexivity can be seen as the appreciation of the native token price due to the accumulation of protocol revenues.

The "indirect" aspect lies in the governance capability of the native token: if token holders can decide how to manage the protocol's funds, they can benefit from accrued revenues. Therefore, the price of the token, which represents the claim on the protocol's funds, should increase with rising revenues.

The problem is that the impact of revenues on token prices is not direct, as it involves governance voting.

We all know that governance systems have flaws that can be maliciously attacked and tend to favor whales. This is why the "governance" function of tokens is often underestimated by retail investors but appreciated by whales.

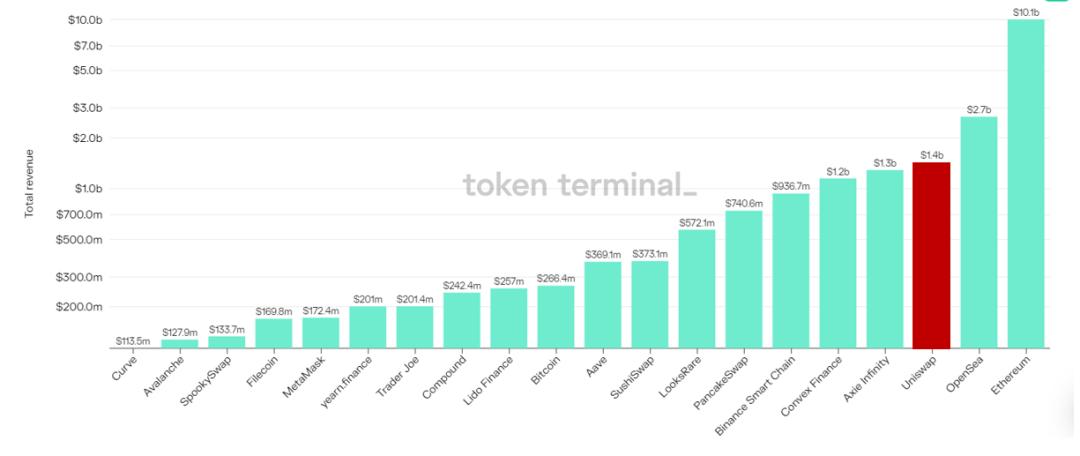

Take Uniswap as an example.

In September 2020, the UNI token, which had no utility other than governance, launched with a market cap of $16 billion, while Uniswap's treasury held $4.7 billion in funds—almost a 4x premium.

It's hard to say whether this premium is fair, but Uniswap generated $1.7 billion in revenue over the past 12 months (ranking just behind Ethereum and OpenSea).

The 82 governance proposals put forth this year undoubtedly contributed to this, although quantifying this contribution is more of an art than a science. One thing is more certain: retail investors are not interested in governance (perhaps because all of Uniswap's revenues have been returned to LPs so far).

How do we know? Look at the average participation rate in governance voting. For Uniswap, it is only 1.9% of the total number of token holders.

Direct Reflexivity

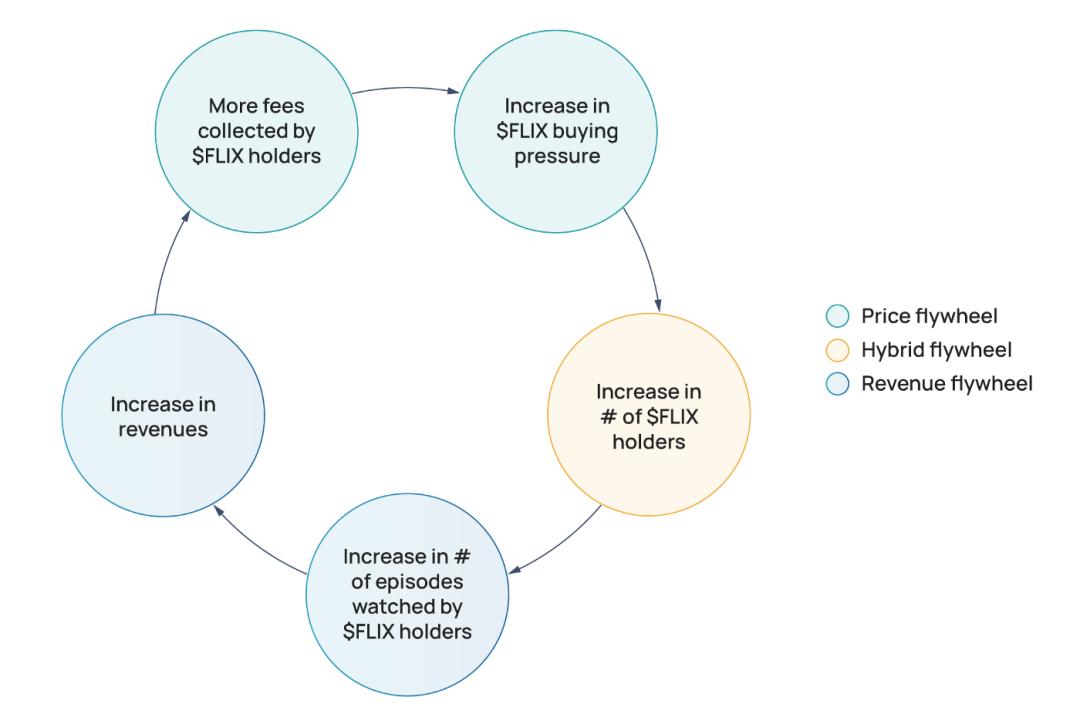

Suppose Netflix launches its own token, FLIX, with the following pricing and revenue-sharing features:

Non-token holders must pay 1 dollar of FLIX to watch an episode, while token holders only pay 0.5 dollars of FLIX.

50% of the FLIX collected by Netflix will be automatically proportionally credited to each token holder's wallet.

This would create buying pressure for FLIX, as investors would want to receive half of the protocol's revenue, while the 50% discount would also incentivize token holders to become users.

By doing so, future revenues would be positively correlated with the number of token holders, and due to the revenue-sharing mechanism, the number of token holders would also be positively correlated with protocol revenues.

We have just designed a structure of direct reflexivity. Now let's answer:

What determines the appreciation/depreciation of the native token price? Increased revenue.

What does the appreciation/depreciation of the native token price mean for the operation of the project? Increased revenue.

Everything seems great… until revenue stops growing. So what will happen?

As revenues decline, the 50% profit will not be enough to compensate token holders, who will sell their $FLIX tokens to profit from the previous price increase.

This will put downward pressure on the FLIX price and reduce future revenues, as fewer token holders mean fewer users. The decline in FLIX price will also reduce the dollar value of Netflix's revenues, starting a vicious cycle.

Is Reflexivity Good or Bad?

In absolute terms, reflexivity is neither good nor bad. It's like riding a roller coaster: it's fun, but it should be done in moderation.

Reflexivity should be a pillar of the business model, not the business model itself. Any protocol should be able to return a portion of the value generated to token holders while allowing them to contribute to further development either as users or indirectly through governance. In the early stages of a protocol's lifecycle, reflexivity can attract interest and activity.

However, as we saw in the Netflix example, good times do not last forever. In bear markets, reflexivity becomes a double-edged sword. This is why during bear markets, protocols that are unremarkable except for reflexivity tend to suffer much greater losses than others, and a significant portion never recovers from the lows.

Reflexivity Case in DeFi: Olympus DAO

The project aims to create a community-owned decentralized and censorship-resistant reserve currency backed by a large amount of assets supporting this currency. Each native token OHM can be exchanged for 1 DAI.

Olympus DAO has a rich and diverse treasury composed of stablecoins and volatile assets, so the market value of OHM far exceeds the corresponding DAI.

How does Olympus DAO accumulate these assets?

Through a so-called bonding mechanism: users deposit assets worth X dollars (such as DAI, ETH, etc.), and after a certain period (bonding term), they receive X + premium OHM.

This means that the premium amount of user profits depends on the difference between the OHM price and the dollar value supported by each OHM. If the OHM price exceeds the dollar value supported by each OHM, a portion of that difference can be paid as a premium to bondholders.

Therefore, the higher the OHM price, the higher the premium paid to bondholders, and the greater the expected future bond volume.

How do bondholders handle their OHM? Why don’t they simply dump OHM to cash out? Because Olympus DAO once offered astonishing APYs to incentivize token holders to stake their OHM.

Staking rewards are paid in inflationary OHM, which causes dilution. Nevertheless, if the dilution is offset by an increase in treasury assets, the combined effect of higher treasury assets and higher buying pressure for OHM should increase.

Now we have all the elements to answer these two decisive questions:

What determines the appreciation/depreciation of the native token price? Increased bond trading volume.

What does the appreciation/depreciation of the native token price mean for the operation of the project? Increased bond trading volume.

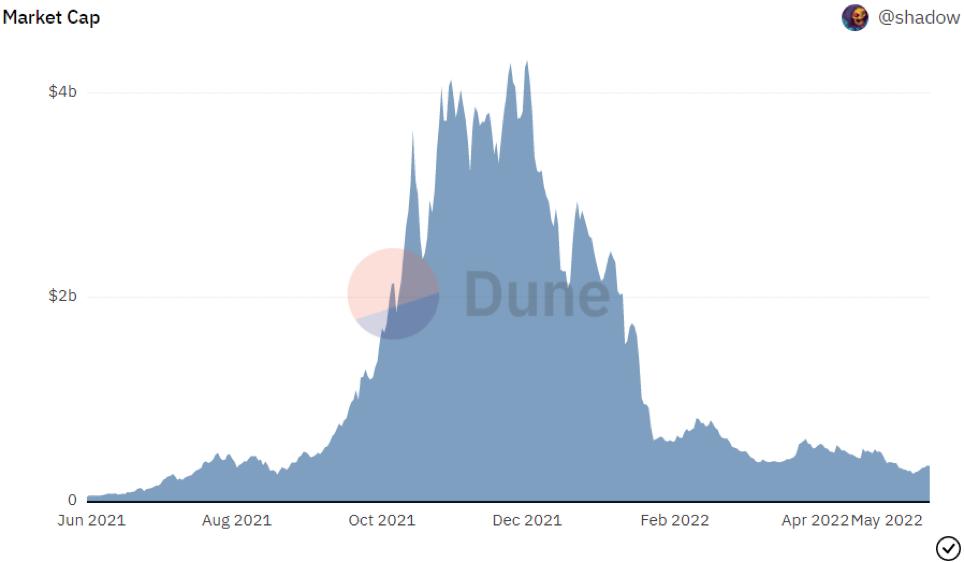

Olympus DAO launched in March 2021 and achieved astonishing growth before December 2021, peaking at a market cap of over $4 billion, with a treasury market cap exceeding $800 million. But since then, the entire market has started to decline, and OHM's drop has far outpaced most peers.

The poor performance of OHM is attributed to various factors, but reflexivity played a significant role.

In fact, during periods when the OHM price was below its supported value, the team paused regular bonds because there was no room to pay a premium for tokens that were severely below their supported value.

They introduced so-called "reverse bonds." These bonds allow investors to deposit OHM (which will be burned) and receive premium treasury assets. Although reverse bonds reduce the size of the Olympus DAO treasury, they increase the support for each OHM.

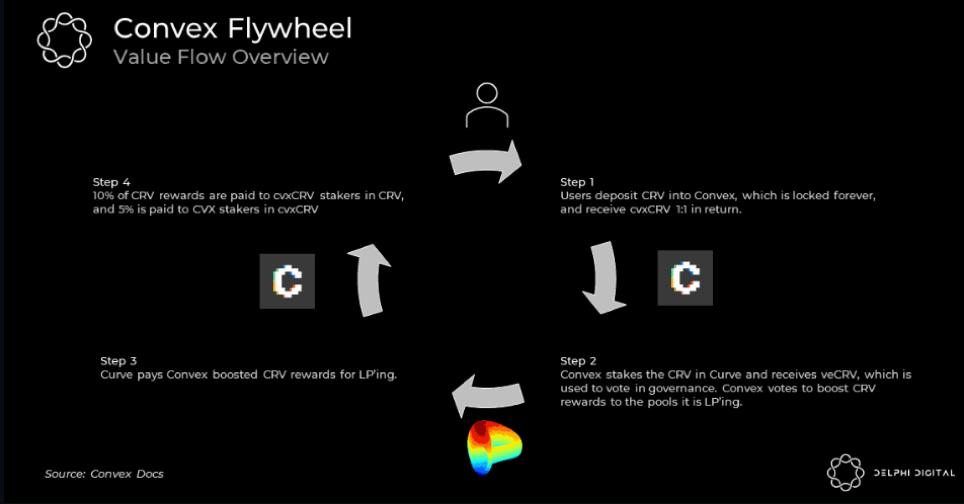

Reflexivity Case in DeFi: Convex Finance

The project aims to enhance the liquidity and yields for liquidity providers on Curve. To understand why this model is successful, let's revisit the role of Curve and how users earn yields on Curve.

Curve is a decentralized exchange specializing in stablecoin swaps. Since the risk of swapping one stablecoin for another is relatively low, the exchange fees are much lower than traditional exchange fees for volatile assets (averaging 5 basis points, compared to 25-30 basis points for volatile assets).

Low fees are not the huge incentive for investors to provide liquidity in the pools. Since stablecoins require very high liquidity to affect swaps at lower prices, Curve uses its native token CRV to incentivize LPs.

Receiving CRV tokens is good, but staking them is even better. CRV stakers lock their tokens for a period (up to 4 years) and receive veCRV tokens as receipts. The longer they lock their CRV tokens, the greater their governance power in deciding which pools should receive the most rewards.

Curve Stakers and LPs can now deposit their CRV or their LP tokens into Convex and earn additional yields paid in CVX tokens.

What does Convex gain? Power!!!

Convex accumulates CRV, and CVX holders can lock their tokens to vote on where to direct Curve incentives.

This is the role of reflexivity: the higher the CVX price, the higher the yields for those staking CRV or Curve LP tokens on Convex. The higher the yield, the larger the share of CRV and LP tokens deposited in Convex.

In turn, this will increase the number of CRV that CVX holders own and the chances of directing CRV incentives to specific pools. Higher incentives mean easier staking of CRV or providing liquidity to Curve pools. Higher liquidity on Curve means a better trading experience, leading to more trading volume, more fees… and then the cycle starts again.

Let's complete these questions:

What determines the appreciation/depreciation of the native token price? Increased yield in Curve liquidity pools.

What does the appreciation/depreciation of the native token price mean for the operation of the project? Increased yield in Curve liquidity pools.

Convex Finance generated $1.2 billion in revenue over the past 12 months, peaking at a market cap of $2.2 billion. Quite a decent number, comparable to Uniswap's data.

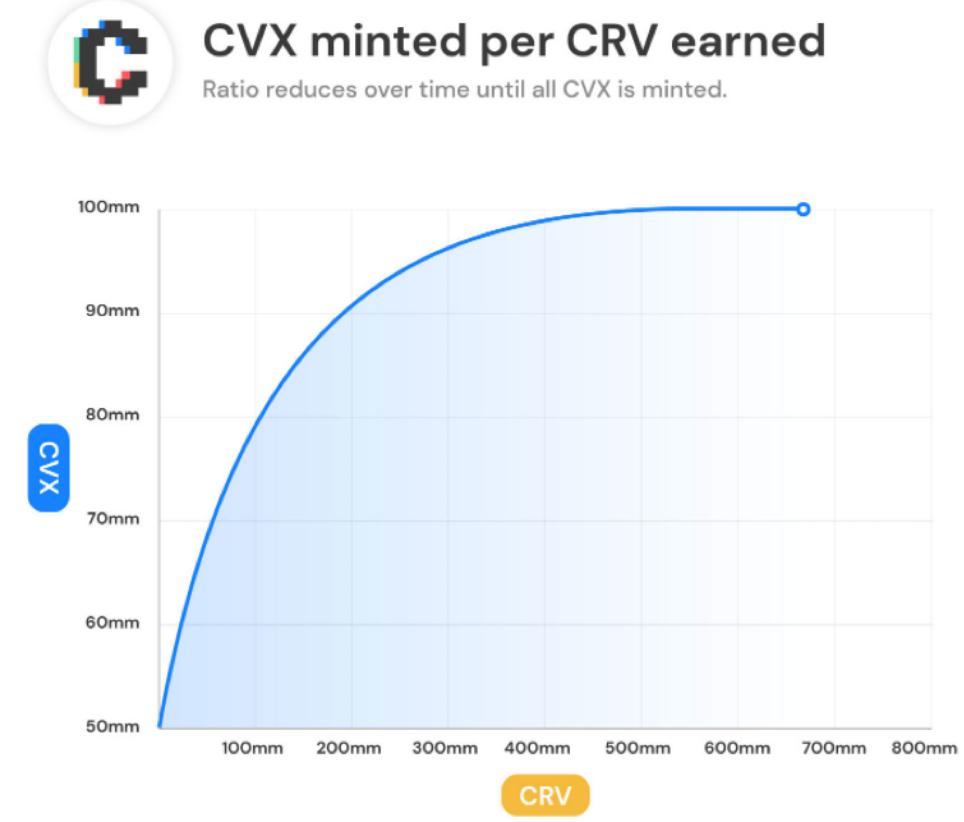

However, for Olympus DAO, reflexivity often means maintaining a rapid token issuance rate to reward token holders.

Convex launched about a year ago and has already issued over two-thirds of the total supply of CVX, while Uniswap launched the UNI token in September 2020, with a circulation of less than 50% of its total supply.

Convex needs Curve to operate at full speed 24/7/365 to maintain its market cap. In particular, Convex needs projects interested in listing their tokens on Curve and paying hefty fees to gain CRV incentives in such pools.

The 4pool is a significant catalyst for the CVX token, as Do Kwon allegedly reached agreements with multiple projects holding over 62% of the CVX owned by the DAO.

The collapse of Terra caused the CVX price to drop by 50% within days, and if the market loses confidence in algorithmic stablecoins like FRAX (the first CVX holder), the negative spillover effects may be far from over.

Conclusion

Most critics of the current state of DeFi believe that the repeated entanglement with reflexivity is one of the main factors hindering its development. This may be because the vast majority of DeFi investors either do not understand how reflexivity works or believe it can last forever.

Moreover, the ve(3,3) trend initiated by Andre Cronje's Solidly project has led a long list of protocols to adopt reflexivity-based tokenomics designs that fit only a few other dApps in Curve and DeFi, but the results have not been ideal for other protocols either.

A lack of patience and long-term commitment is one of the most apparent issues in DeFi, a problem that can be temporarily patched with incentives, over-collateralization, reflexivity, and other elegant mechanisms, but requires more structural changes in mindset for a lasting solution.

The current bear market is an excellent opportunity to reflect on existing flaws and propose new designs, where investor awareness is foundational, and all the fancy flywheels are valuable auxiliary functions.

Risk warning

Risk warning Risk warning

Risk warning