Extinction, Survival, and Evolution: Reflections After the November Crypto Market

For the cryptocurrency market, 2022 is destined to be an extraordinary year. In the first bear market following the large-scale entry of traditional institutions, we witnessed countless top crypto institutions and projects that, after rising, quickly became a page in history; we also saw many projects that survived the bull market continuously iterating on technology and innovating during the bear market, driving the resilient development of the crypto industry. The cryptocurrency market will not perish; it is merely evolving.

For the cryptocurrency market, 2022 is destined to be an extraordinary year. In the first bear market following the large-scale entry of traditional institutions, we witnessed countless top crypto institutions and projects that, after rising, quickly became a page in history; we also saw many projects that survived the bull market continuously iterating on technology and innovating during the bear market, driving the resilient development of the crypto industry. The cryptocurrency market will not perish; it is merely evolving.Author: Matt CEO @Blofin

Source: TokenInsight

Extinction

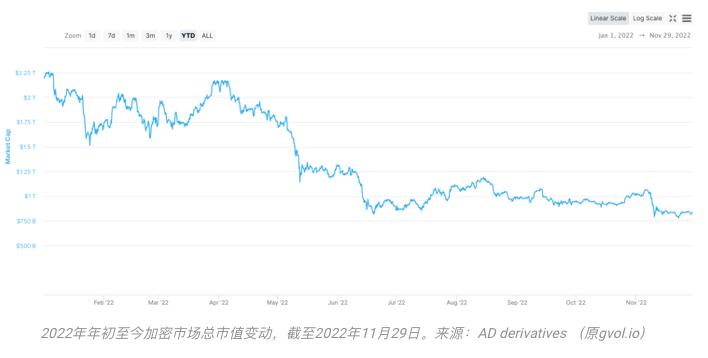

In 2022, some institutions left an indelible mark on the history of the crypto market: the collapses of Luna, 3AC Capital, and FTX drove the market capitalization of the crypto market down from around $1.8 trillion to below $850 billion, forming three significant peaks in the volatility chart of the crypto market. However, many more institutions and projects only appeared in the news once, or not at all; they simply went bankrupt or collapsed, "vanishing into thin air."

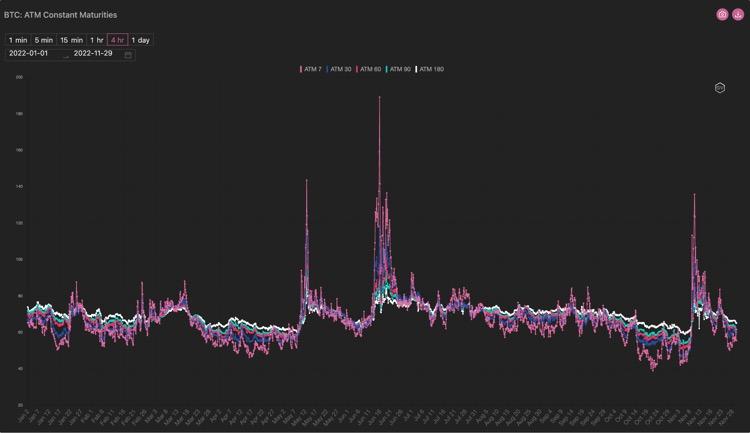

BTC implied volatility changes from the beginning of 2022 to November 30, 2022. Source: AD derivatives (originally gvol.io)

BTC implied volatility changes from the beginning of 2022 to November 30, 2022. Source: AD derivatives (originally gvol.io)

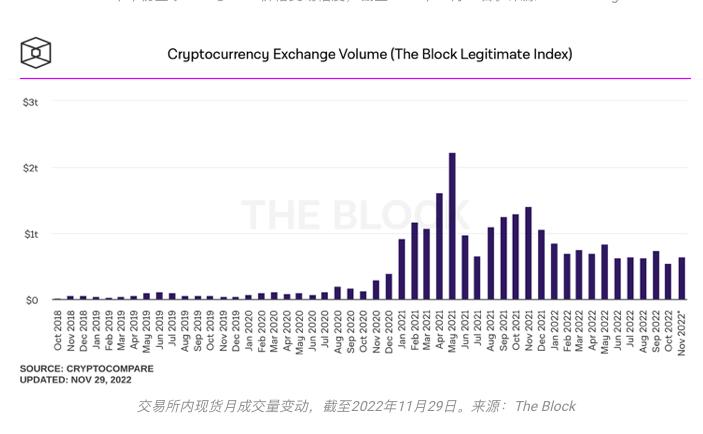

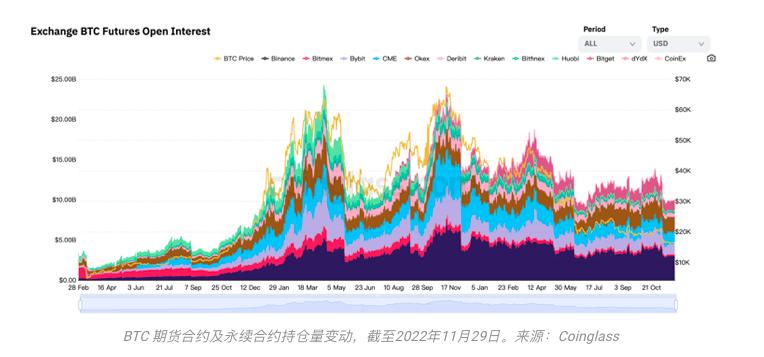

For individual investors and believers in the crypto market, the decline of crypto assets and a series of events gradually pushed them towards exiting or waiting on the sidelines—this directly led to a decline in trading volume and a decrease in market depth. At present, with the prices of BTC and ETH down more than 60% from the beginning of the year, the trading volume in the spot market has fallen to its lowest level since January 2021; in the derivatives market, the open interest of BTC perpetual contracts and futures contracts has also dropped to levels seen in December 2020.

From the data, many investors may believe that we are indeed close to the bottom. The institutions and projects that have collapsed are now in the past; the dollar has begun to decline from its highs, and the Federal Reserve has indicated it may reduce the rate of interest rate hikes. However, this seems a bit overly optimistic.

From the data, many investors may believe that we are indeed close to the bottom. The institutions and projects that have collapsed are now in the past; the dollar has begun to decline from its highs, and the Federal Reserve has indicated it may reduce the rate of interest rate hikes. However, this seems a bit overly optimistic.

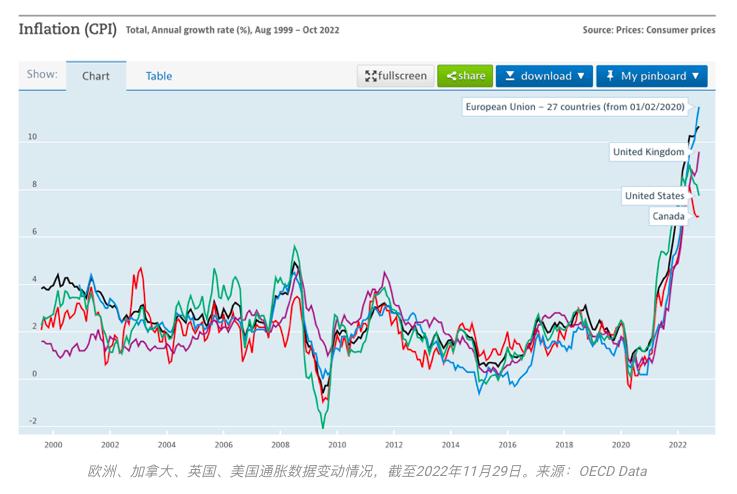

From a macroeconomic perspective, the crypto market still faces increasing liquidity pressure. During the pandemic, countries released a large amount of liquidity through multiple interest rate cuts and relief policies to support economic stability. As most countries enter the post-pandemic era, the inflation issues caused by the previously released liquidity need to be addressed. Although major central banks, represented by the Federal Reserve, have raised interest rates to relatively high levels, inflation remains at a relatively high level:

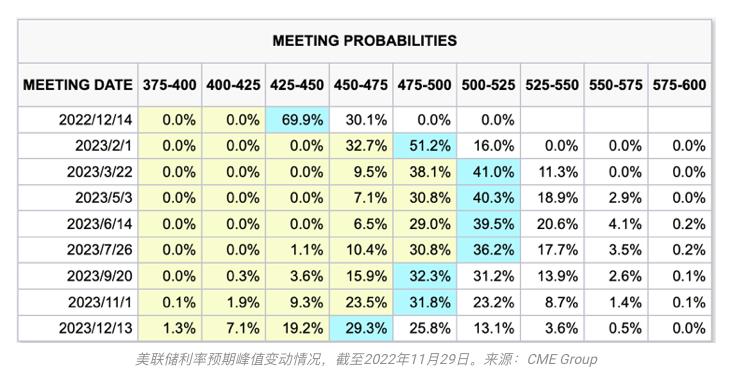

Therefore, to curb inflation, interest rate hikes must continue. Both Federal Reserve officials and the President of the European Central Bank emphasize the necessity of continued rate hikes and high interest rates. In the interest rate market, traders have priced the Federal Reserve's terminal rate at 5%-5.25%; but this may not be enough. In summary, investors need to prepare for higher interest rate peaks.

One of the direct consequences of significant interest rate hikes and high interest rate peaks is economic recession. Since suppressing inflation is the core goal of major central banks, from the statements of central bank officials, it seems that despite the potential for deflation and recession, they ultimately choose to ensure the achievement of inflation targets in the "inflation target or economic stability" dilemma. The yield curve spread between 2-year and 10-year U.S. Treasury bonds has reached its highest level since 1980, and investors' implied recession expectations are even higher than during the bursting of the dot-com bubble in 2000 and the 2008 financial crisis.

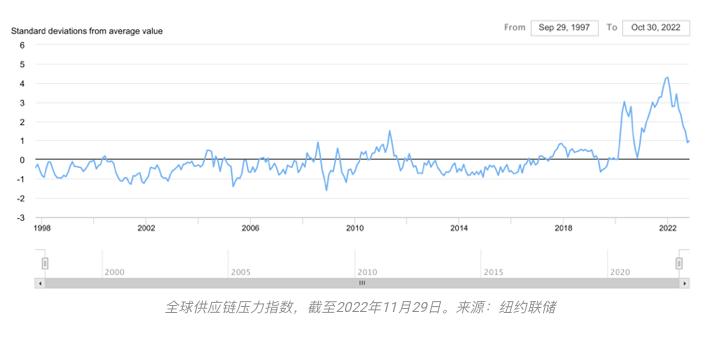

In addition to pressure from central banks, the impacts of the pandemic and war cannot be ignored. The New York Fed produces a Supply Chain Pressure Index every month based on the global supply chain's operational status. As the Northern Hemisphere enters winter, COVID-19 peaks in China, while the Russia-Ukraine war continues to exert ongoing pressure on commodities such as energy. Under the combined influence of both factors, the alleviation of supply chain pressure that had lasted for five months has temporarily stopped; this means that inflationary pressures from the supply side may once again impact the market.

The above situations are already quite unfavorable for the crypto market, which is at the end of the liquidity spectrum for risk assets. With the return of liquidity still far off, risks within the crypto market are also continuously rising: bankruptcies of projects and institutions, even the collapse of leading exchanges, have left many investors feeling disappointed about the future of the crypto market, choosing to exit at low levels. Regulatory authorities have also accelerated legislation on the crypto market due to the massive losses caused by various fraudulent activities and excessive leveraged trading, further pushing investors and funds out of the crypto market.

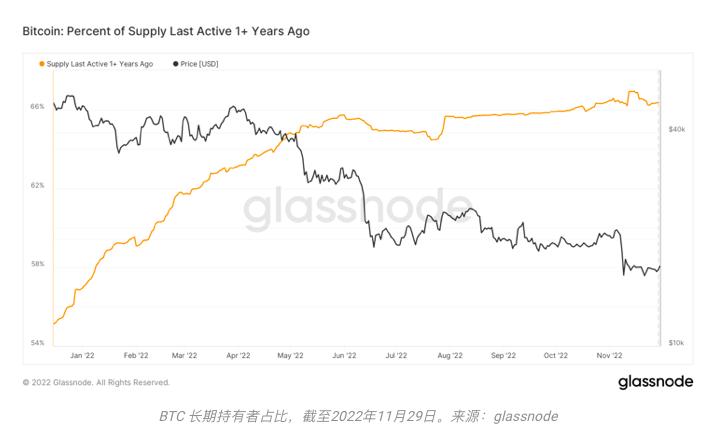

Taking BTC as an example. Generally speaking, long-term holders tend to accumulate coins during bear markets and sell during bull markets. Therefore, during bear markets, the proportion of long-term holders steadily increases, while in bull markets, this proportion decreases. However, from May to July, the proportion of long-term holders saw a significant decline, and a similar situation occurred in November. Disappointed investors threw their chips to others and left the market.

In summary, the bear market cycle of the crypto market is far from over. In a series of shocks in 2022, some institutions were fortunate enough to survive, while some large institutions are teetering on the brink, waiting for rescue. No one knows who will be next; the market tells us that in the "great extinction" of the bear market, those who survive are often not the strongest, but the luckiest and those who were prepared early.

Survivors

Although the crypto market has become frigid, it is certain that the bear market of 2022 is far from the end of the crypto market. Beneath the ice, developers and participants in the crypto market continue to remain active. Technological iterations are ongoing; VCs and angel investors are still searching for projects that may explode in the next bull market; and the results of the DeFi Summer before the last bull market and the NFT Summer of 2021 are still active in the crypto industry.

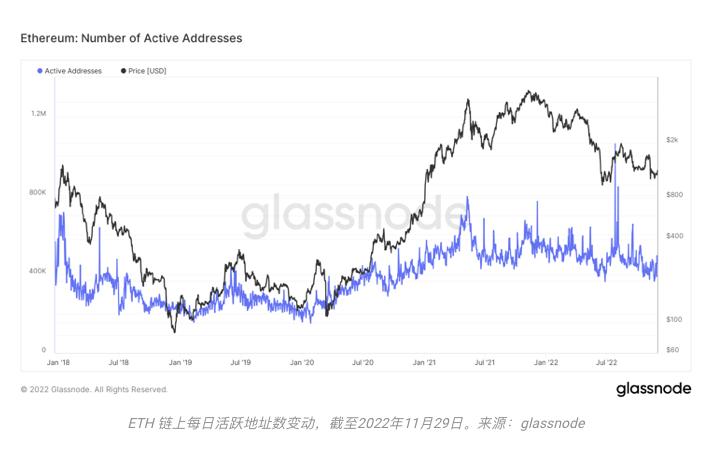

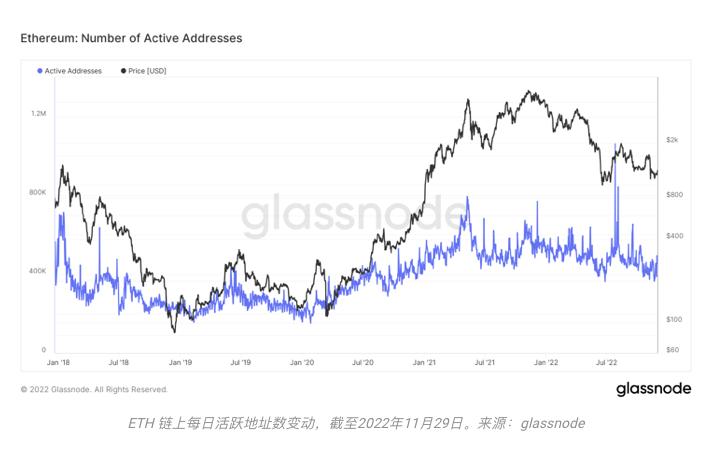

As one of the core infrastructures of DeFi and NFTs, the on-chain data of ETH somewhat confirms the resilience of the crypto industry: although the number of active addresses has dropped to its lowest level since December 2020, the proportion of ETH tokens active in smart contracts compared to the total token supply has only decreased by about 3% compared to its peak, still comparable to the average level during bull markets.

At the same time, even after the shocks of May and June, the proportion of ETH active in smart contracts has not declined much, and the gap caused by the ETH Merge has been quickly filled.

For various projects in the crypto industry, the series of shocks during the bear market did not make them yield. Even in a harsh market environment like 2022, the DeFi market and NFT market still maintain a certain vitality.

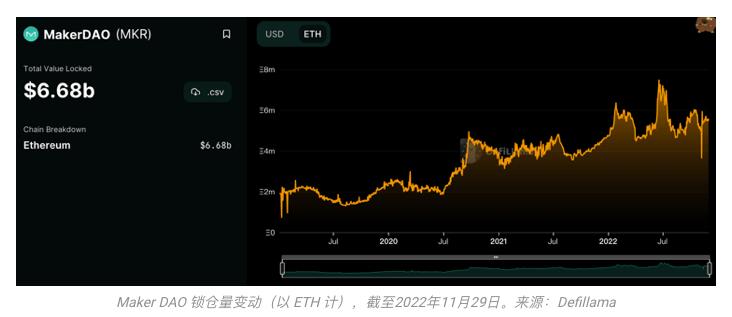

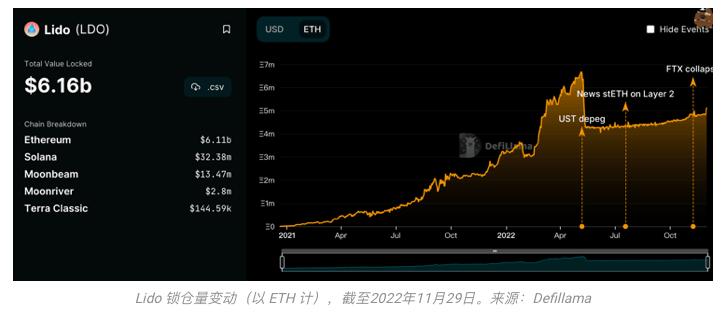

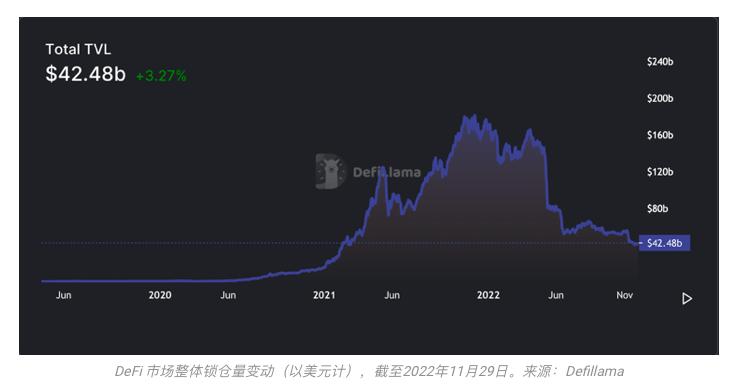

From the perspective of locked assets, if we consider the native asset of the crypto market, ETH, rather than USD, the locked assets of leading projects like Maker DAO and Lido still achieved positive growth in 2022; even when measured in USD, the DeFi market still maintains over $40 billion in locked assets, comparable to 2021, and far better than before 2021—this means that the DeFi market has become an indispensable part of the crypto market.

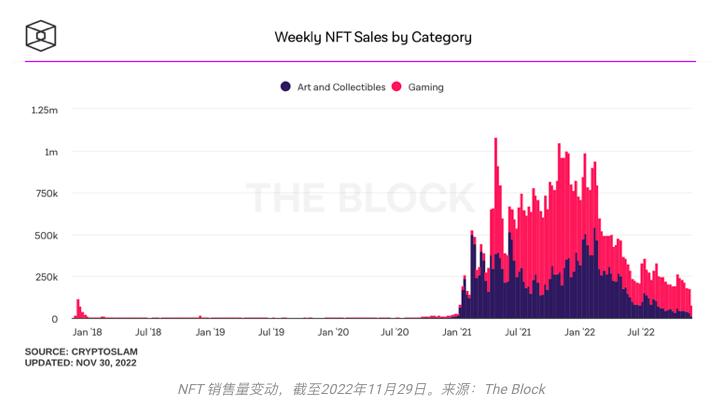

The NFT market is no different. The winter of the crypto market has not dampened the trading enthusiasm of NFT investors: although it cannot be compared to previous peaks, in November 2021, the weekly sales of NFTs were still on par with the first quarter of 2021, far exceeding levels before 2020; and trading among investors continues to take place—though not very active, the monthly trading volume of leading projects still exceeds 20,000 ETH, which was unimaginable in the last crypto market cycle.

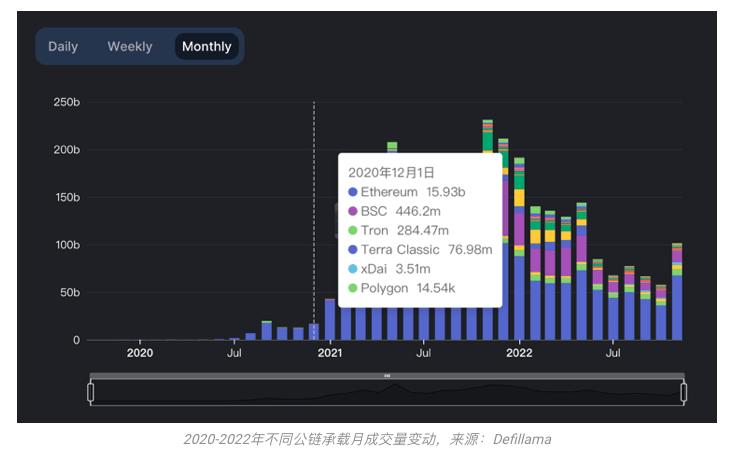

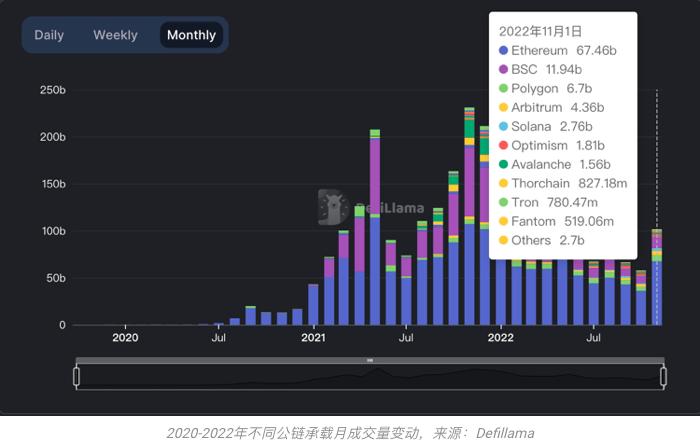

It is worth noting that, aside from ETH, other underlying public chains supporting the crypto market have also maintained good development momentum during the bear market. Unlike December 2020, when ETH held absolute dominance, by the end of November 2022, there were at least 10 mature public chains available for developers and users to choose from. Among them, mature Layer 2 solutions like Arbitrum and Optimism, as well as public chains like Avalanche and Polygon that rose during the last bull market, still have relatively mature user and developer communities, handling monthly trading volumes exceeding $10 billion. Undoubtedly, this lays a solid foundation for the resurgence of the crypto market in the next bull market.

Stablecoins are also driving the crypto market towards maturity. Unlike the "completely wild" crypto market of 2018, as a channel and liquidity vehicle between traditional finance and the crypto market, the total supply of stablecoins surpassed $150 billion in 2022; even in the market environment of November 2022, the supply of stablecoins remained stable above $140 billion.

The number of traders holding stablecoins is also continuously rising. As of November 2022, the number of addresses holding stablecoins has easily surpassed 6 million, with countless retail and institutional investors linked to them. These stablecoins are widely used for on-chain trading, spot trading, and derivatives trading. Crypto investors have not stopped their steps due to the bear market.

Evolution

After experiencing the collapse of "quality projects," institutional bankruptcies, and the closure of leading exchanges, although the crypto market has survived, the remaining investors will still participate in trading, but they will no longer trust project teams, institutions, and exchanges; what investors believe in now is only their wallets.

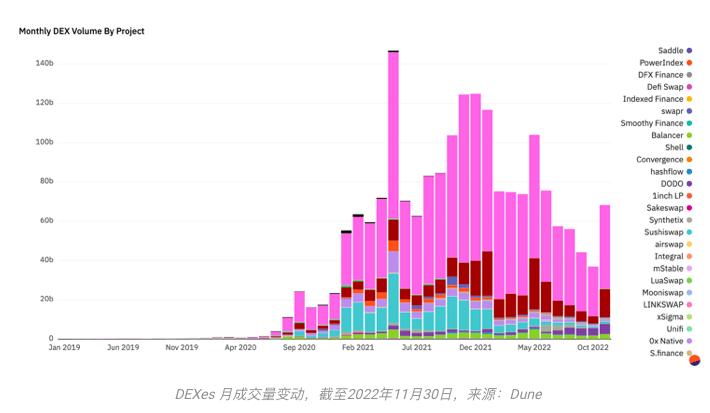

As investors gradually reach a consensus from the historical lessons of the crypto market, their focus has shifted back to DEXs. Compared to October 2022, just one month later, the outbreak of the FTX incident pushed the total trading volume of DEXs back up to nearly $70 billion—almost doubling. The importance of wallets has gradually become prominent, and wallet projects have begun to receive hundreds of millions of dollars in investments from leading institutions, becoming a new trend at the end of 2022.

However, the current use of wallets is not convenient. Frequent interactions lead to high transaction costs, and the limited application scenarios for wallets restrict user usage.

Consider the following scenario: when investors see a desirable asset or NFT, they find that the application does not support the wallet they hold. In a bull market, they need to find alternative paths, and congested public chains bring disastrous experiences and "impressive" transaction costs to investors.

In a bear market, traders have ample motivation to abandon trading:

- If they store funds in certain centralized exchanges for convenience, their principal may be directly taken away by unscrupulous operators lacking compliance and professional ethics; aside from an announcement, nothing will remain.

- If they choose to take a detour, investors typically are not interested in spending too much time and cost. "Just a glance is enough"—they might say.

For crypto market builders, the above situations open up new evolutionary paths for them:

- Build a better exchange, good enough to regain investors' confidence and favor.

- Or, create a sufficiently good wallet.

Creating a wallet is not easy, but evolving towards an exchange is even more challenging: rebuilding the trust that has been destroyed takes time. Investors have had enough of endless survival games and hide-and-seek; they just want exchanges to do what exchanges are supposed to do. Matching, trading, clearing, risk control—this is enough.

Public asset proof and Merkle trees are just the first step. We have witnessed the disastrous consequences of chaotic audits and custody, and regulators will not allow similar situations to occur again. Therefore, compliant custody and auditing of assets are challenges that every old and new exchange must face; investors do not want to lose everything again. Complete licenses, qualified audit reports, and comprehensive custody are prerequisites for regaining user trust.

Rating of underlying assets is also an important aspect for the future. In the crypto market, ordinary investors often lack awareness of the assets they are trading; they rush into the market with dreams of getting rich, only to lose part or all of their principal. Ratings can solve this problem: under a sound rating mechanism, investors can understand the risks and potential returns of the underlying assets before trading and make the most suitable choices after consideration.

For centralized exchanges, since investors trust their wallets more, with the public chain system gradually improving, the plan to "expand exchanges onto the chain" becomes feasible: investors can trade with low or even no trust. The open interest of BTC and ETH perpetual contracts on dYdX has already exceeded $100 million, surpassing many small and medium-sized centralized exchanges. Large exchanges have also begun to explore development towards the chain: exchanges like Bybit have launched self-operated wallet services, and in the future, we may see large exchanges further launch their own spot and derivatives trading divisions on-chain.

Regardless of bull or bear, the history of the crypto market has never been interrupted. Institutions lacking risk awareness and exchanges lacking compliance awareness have disappeared in the bear market, providing sufficient space and new ecological niches for survivors. At the same time, in this "time of rebuilding," survivors now possess the most comprehensive and diverse construction foundation to date: a mature spot market and derivatives market, a complete public chain system, and a resiliently growing DeFi and NFT market provide developers and builders with "almost infinite" directions and possibilities for evolution. Let's BUIDL now and wait for the next bull together.

Risk warning

Risk warning Risk warning

Risk warning