How does Ethereum L2 affect value capture on L1? Do we still need L1 competing chains?

The growth and scalability of Ethereum L2 will shake the value proposition of L1 competing chains that adopt similar scalability approaches.

The growth and scalability of Ethereum L2 will shake the value proposition of L1 competing chains that adopt similar scalability approaches.Original Title: Are L2s Complementary to ETH?

Author: Michael Nadeau

Translation: 0x11, Foresight News

During this crypto winter, the growth of Ethereum scaling solutions is one of the few stories that the market continues to pay attention to. Transaction fees are decreasing, applications are migrating to L2, and TVL is growing; meanwhile, user experience is also improving.

L2 has reached a spotlight moment, but how does it affect ETH on L1? Should ETH holders and validators view L2 as a complement to Ethereum? Will value accumulate in the tech stack? What does this mean for other L1 public chains?

This week we have a data-driven update covering the economics of the Web3 tech stack related to L2:

1) L2 business models and recent growth

2) How L2 affects ETH economics

3) Investor mental models/frameworks

4) Do we still need L1 competing chains?

L2 Business Models and Recent Growth

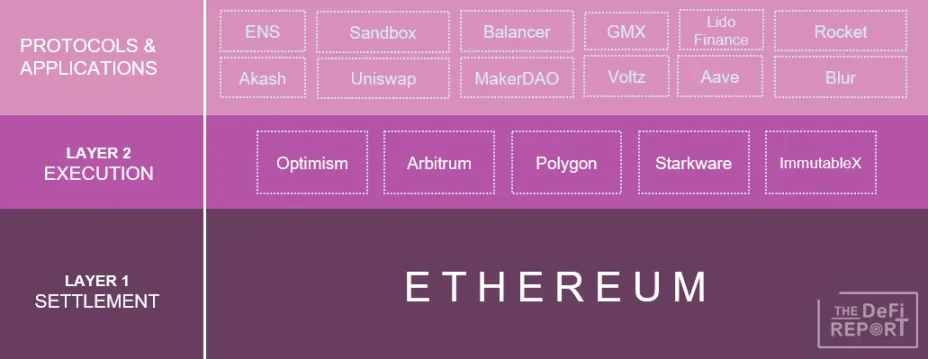

L2 aims to solve the scalability issues of Ethereum L1. They profit by compressing data and "reselling" Ethereum's block space. L1 is slow and expensive, with limited block space. Therefore, we should view Ethereum as the ultimate clearing and settlement layer of the tech stack. The base layer records the final state of everything happening on the execution layer and application layer above it—serving as the sole source of truth.

Execution services that enhance user experience for applications (lower costs, faster transactions) will be handled by Layer 2. These services are executed on another chain outside of Ethereum and then the data is recorded back to L1. Below is a simplified view of the tech stack.

Currently, most computational resources (Gas) are consumed on Ethereum L1, where applications were initially built. Keep in mind that the Web3 stack does not have a centralized party coordinating development activities (neither does the internet), everything is open-source. Builders are rushing in, but not everyone is working on the same timeline or agenda. This is not the well-coordinated agile sprints you see in a well-run tech company. Before the rollout of scaling solutions, both L1 infrastructure and applications were under construction. With the explosion of L2, we expect to see more applications migrate, and future new projects may launch directly on L2.

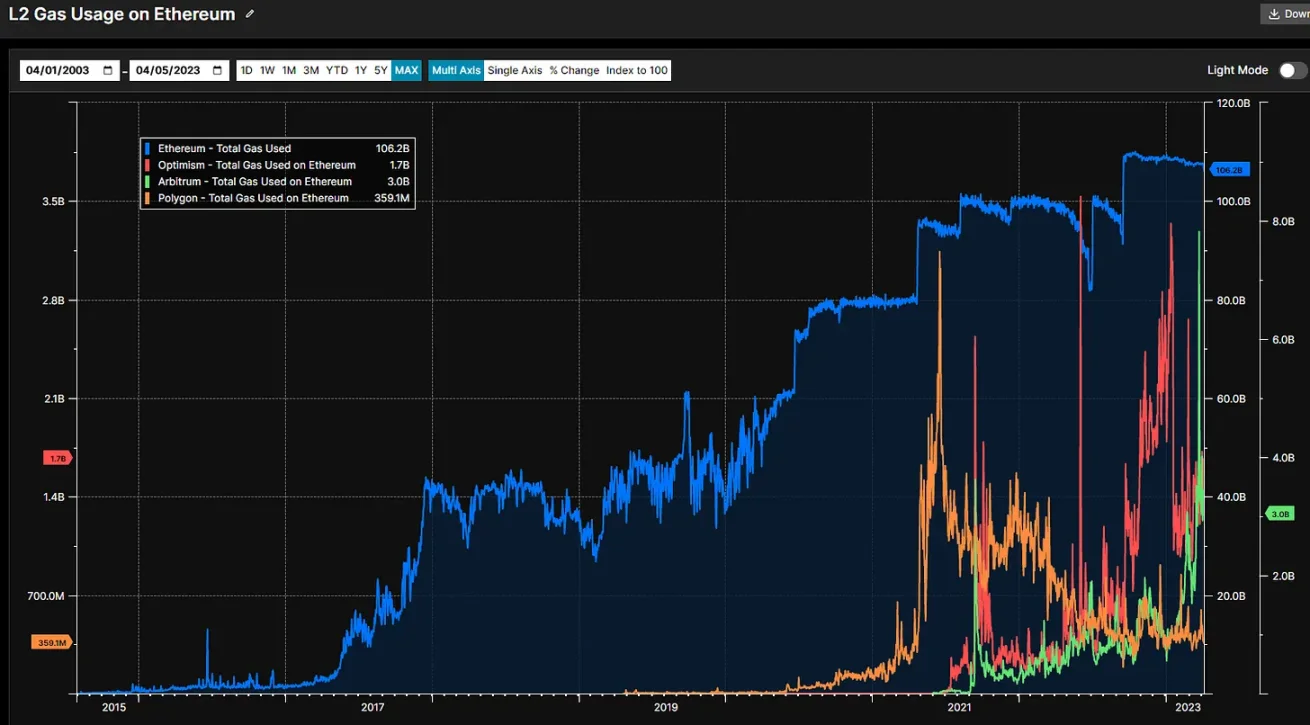

Data reveals this trend; let's quickly look at the total computational resource (Gas) usage on Ethereum, as well as how top L2s are currently consuming resources.

Data Source: Arcana Analytics

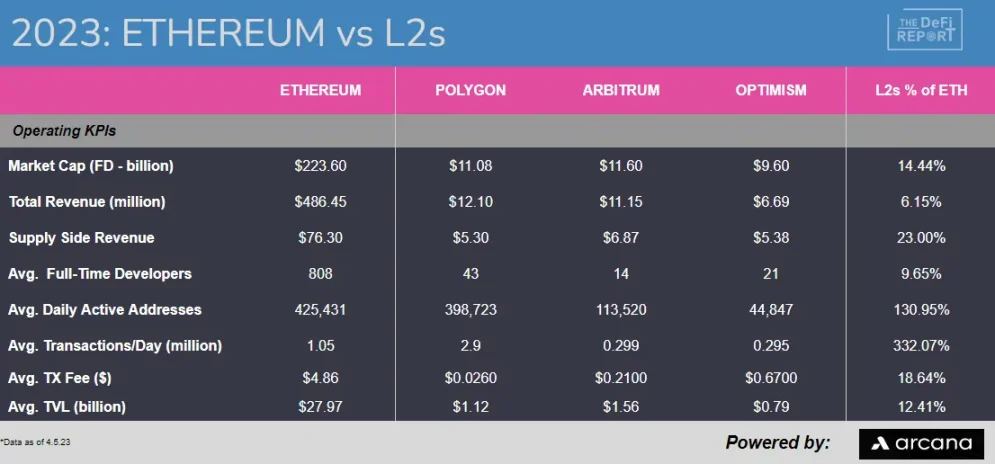

Arbitrum and Optimism now occupy more block space than Polygon. Overall, these three L2s account for about 4.5% of the current Ethereum block space, up from about 3% at the end of 2022.

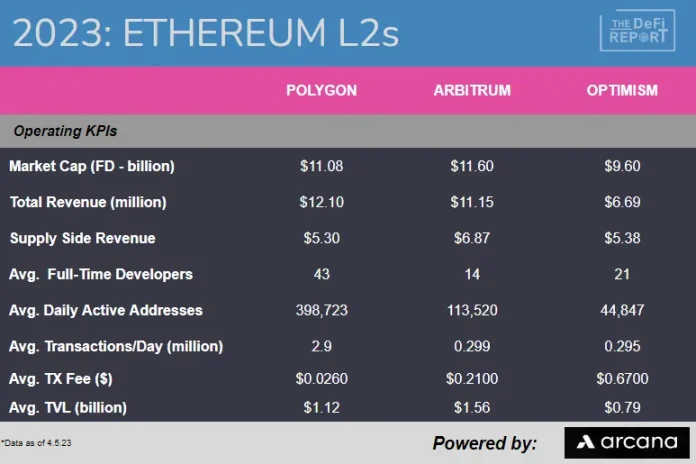

Next, let's look at some other data on L2:

Note: Since the beginning of 2023, the average transaction fee on Ethereum L1 has been $4.84.

As mentioned earlier, L2 serves applications by providing users with a better and cheaper experience. They purchase block space on Ethereum L1, then compress data, package transactions, and ultimately record the data proofs back to Ethereum.

But are all L2s equal? Are they all complements to Ethereum?

L2 and ETH Economics

Before L2, when Ethereum became congested, transaction fees would skyrocket. At one point in 2021, the fee for a single transaction even reached $200. Using Ethereum during the adoption cycle was somewhat like trying to call an Uber after a flight delay—too much demand but not enough supply.

L2 was created to solve this problem. But what exactly happens when users today pay a 21-cent fee on Arbitrum? How much of that fee does Arbitrum capture? How much do validators earn?

When you buy a sandwich at a café, how much value does the baker receive? How much should be paid to the meat producers? To the distributors? How much for toppings and condiments? What makes the sandwich special? What brings the most value? Is everything else a complement?

These are the questions we should consider regarding the economics of L2 and the Ethereum tech stack.

The answer is that as of 2023, about 62% of the fees users pay on Arbitrum go to Ethereum validators. Since its inception in 2021, 64% of all fees have been paid to Ethereum validators.

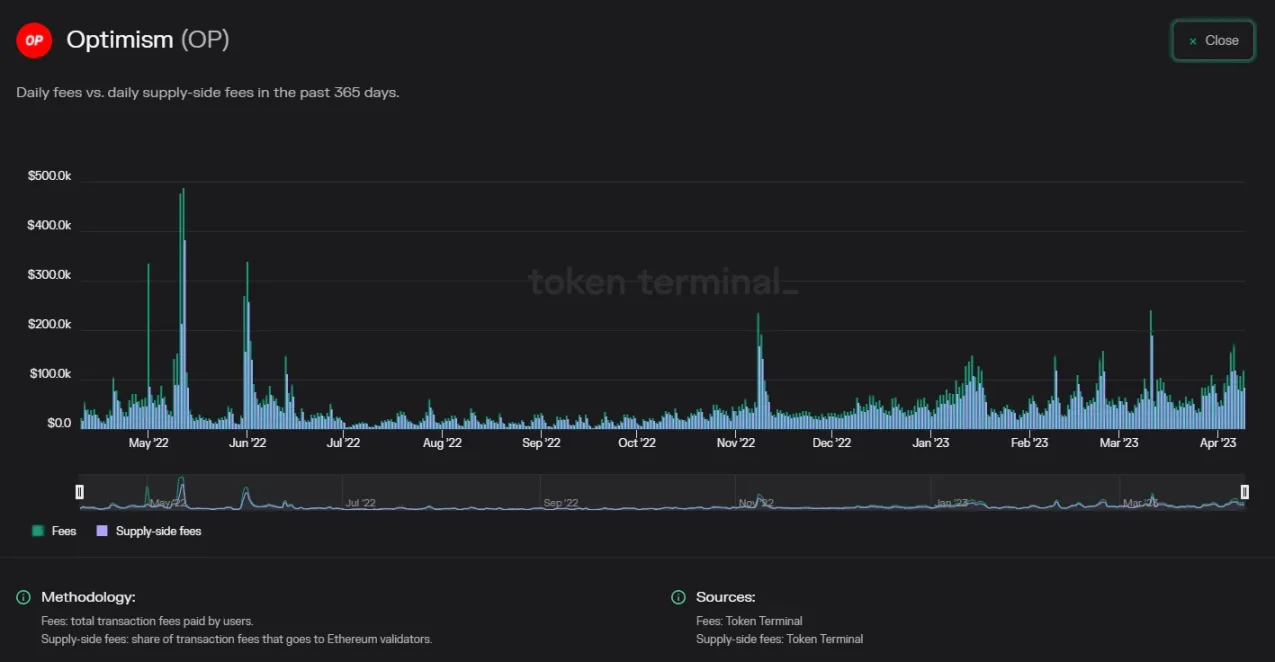

Meanwhile, 80% of the fees generated through Optimism now belong to Ethereum validators. Since 2021, 74% of all fees have been paid to Ethereum L1. Below is data provided by Token Terminal:

This is a win-win situation. Application users receive excellent execution and lower fees, which further drives more use cases, more developers, and ultimately more users. Ethereum validators benefit from transaction fees, while passive holders benefit from increased demand for Ethereum due to higher transaction volumes. At the same time, Optimism and Arbitrum benefit from Ethereum's network effects, essentially outsourcing their consensus and security costs to the base layer.

What about Polygon?

Polygon is a sidechain of Ethereum, which makes it different from Optimism and Arbitrum. As a sidechain, Polygon has its own set of validators. Therefore, it has its own consensus and security, unlike Optimism and Arbitrum, which are "consistent" with Ethereum.

As of 2023, Polygon has paid 44% of user fees to its suppliers/validators, with the remaining fees being burned. Since Polygon's fees are paid in MATIC tokens, Ethereum validators or ETH holders do not receive this value. That said, Polygon regularly submits its state to the Ethereum mainnet, which includes a summary of all transactions on the sidechain since the last checkpoint. The checkpoint is then stored on Ethereum as a Merkle Root, which is a unique hash representing the state of the sidechain at that time. Thus, while Polygon is integrated with Ethereum, its economic impact on L1 is minimal compared to Arbitrum and Optimism, as the checkpoints require minimal data. We can understand this by looking at the main sources of Ethereum's burns. Arbitrum and Optimism rank at the top, while Polygon, despite handling a large volume of transactions, ranks third from the bottom.

In summary, not all L2s are created equal. Sidechains like Polygon operate more like their own L1s while leveraging Ethereum for final security and settlement guarantees. Rollups like Optimism and Arbitrum truly rely on Ethereum for consensus, security, and data availability.

When we analyze the economic impact on Ethereum validators and ETH holders, we believe that Rollups like Optimism and Arbitrum are complements to Ethereum. They can create net new demand for block space by providing application developers with an excellent user experience. Meanwhile, most of the value handled by their solutions ultimately returns to Ethereum validators in the form of transaction fees and to passive ETH holders in the form of fee burns.

Polygon appears to have little complementarity with us. In fact, it seems that Polygon holders and validators benefit more from its close connection with Ethereum.

Investment Perspective: How to Understand Complementarity?

Every product in the market has substitutes and complements. Substitutes are other products you might buy when the first product is too expensive. For example, chicken is a substitute for beef. Complements are products you typically buy together with others, think of gasoline and cars, or bread and hot dogs. All else being equal, when the price of a complement decreases, the demand for that product increases.

Now, if L2 is complementary and they continuously lower costs to achieve an excellent user experience, what does this mean for ETH?

We believe ETH will continue to capture most of the value generated by L2.

An analogy may help highlight our idea: let's compare Ethereum, Google, and the internet. We think owning Ethereum is like owning a part of the internet or running an important protocol on the internet. Now, Google sits on top of internet protocols. Google is great; it solves the search problem on the internet. In this way, Google enhances the utility of the internet, bringing in more users. Now, let's assume that every time someone uses Google search, 6 cents goes to Google and 14 cents goes to the internet protocol. Which would you choose as an investor? What if Google is just one of the thousands of applications running on the internet (Ethereum)?

Similarly, Arbitrum and Optimism are solving important problems. We believe they will drive more users to use Ethereum. But we cannot ignore the fact that today about 70% of the value belongs to ETH validators and holders. The market seems to value the security, decentralization, and settlement guarantees of the execution services provided by L2.

Does this mean investors should avoid L2? There are certainly some nuances. We believe Ethereum could reach a trillion-dollar market cap in the next bull market. If L2 continues to capture 30% of user transaction fees, and all transactions (or the vast majority) are conducted through L2 in the future, one might argue that they could capture 30% of Ethereum's valuation, which would be a projected market cap of $300 billion.

In this line of thinking, L2 still has significant upside potential. Keep in mind that only about 4.5% of the Gas used on Ethereum today runs through L2. That said, the top three L2s combined generate 6% of Ethereum's transaction fees, but their fully diluted market cap reaches 14% of Ethereum's.

Investment Approach

Our current thinking is that a few L2s may capture most of the value of the second layer of the tech stack. This is what we have observed so far and aligns with the power law dynamics we see throughout the Web3 tech stack. We will also focus on the L2, Base, released by Coinbase later this quarter.

Another way to think about it is to compare owning ETH to owning an index fund. Just as new companies rotate into the S&P 500 index, L2s & Apps will rotate in and out of the Ethereum ecosystem. Ethereum validators and ETH holders will benefit from this, just as SPY holders benefit from strong new businesses added to the index fund.

We believe investing in L2 and Apps is more like picking stocks rather than selecting an ETF or index. Of course, in this case, the (ETH) index still represents a bullish option on the future of Web3.

Do We Still Need L1 Competing Chains?

If L2 is solving Ethereum's scalability issues, then what is the value proposition of alternatives like Solana, Avalanche, and Cosmos?

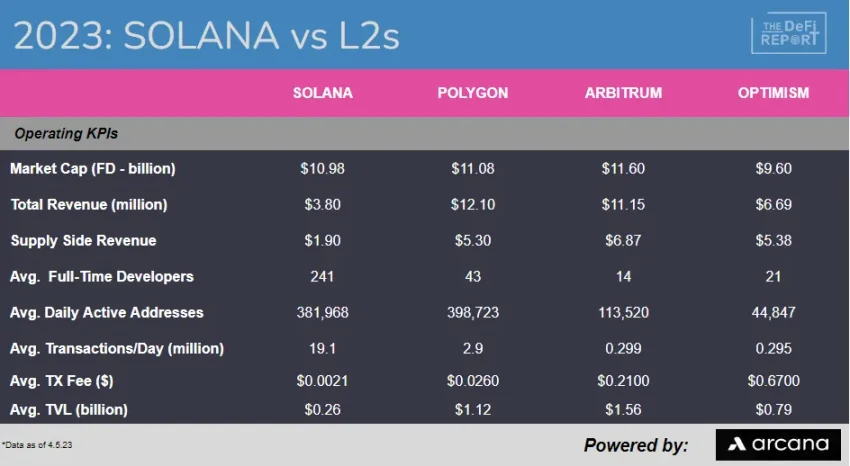

First, let's quickly browse some numbers to compare Solana's performance.

Solana's efficiency is still over 10 times higher than Polygon, which is currently the most scalable L2 (sidechain) on Ethereum. Solana also dominates in terms of developers and has a strong user base, exceeding 380,000 daily users by 2023. That said, TVL reveals the benefits L2 gains from "aligning" with Ethereum. L2 does not have to guide its own TVL like Solana does. I think this is why SOL validators can retain 50% of transaction fees (with 50% being burned), while Arbitrum and Optimism together only retain about 30%.

However, how does Solana's holistic scaling approach compare to Ethereum's modular approach through L2?

Solana bundles settlement and execution services into the same solution, which is unique compared to Ethereum and alternative L1s like Cosmos and Avalanche.

The modular approach adopted by Ethereum, Cosmos, and Avalanche introduces additional complexities related to interoperability, security, centralization, data availability, etc., which Solana does not have to deal with.

We believe Solana is distinctly different from Ethereum and other competitors due to its unique holistic architecture. In fact, Ethereum's approach to scaling through L2 is starting to look very similar to the approaches of Avalanche and Cosmos. Therefore, if developers can deploy on Ethereum Rollup and instantly access Ethereum's liquidity and network effects, why would they choose Avalanche subnets or Cosmos application chains?

In summary, we view Solana as a substitute for Ethereum rather than a complement to Ethereum. We believe this makes Solana the most interesting alternative in the L1 opportunities within the Web3 tech stack—this is also why we built positions in the network during the market dislocation earlier this year. We reported on this project in early January. We also recommended using the network, wallets, applications, staking services, etc. We believe Solana currently offers the best crypto user experience.

In conclusion, as L2 gains traction, we believe the value propositions of alternatives that are not significantly different from Ethereum will be called into question.

Conclusion

1) Ethereum L2 is growing and becoming more efficient. It is still early, but there are signs that Rollups are very complementary to ETH, as validators and holders receive 70% of the fees through them. This is not the case for sidechains like Polygon that run their own validators.

2) The L2 margins of Optimism and Arbitrum need to be monitored. As more competitors enter the space, we expect margins to decline significantly, but we will continue to watch the data. Zero competition could ultimately commoditize the execution layer of the tech stack.

3) Since L2 is complementary to Ethereum, we believe that as L2 costs decrease, the demand for Ethereum-based applications will increase, bringing more value to validators and ETH holders. Note that the transaction volume flowing through L2 ultimately needs to grow faster than the decrease in fees.

4) As solutions like Arbitrum and Optimism mature, the scaling approach of the Ethereum ecosystem seems to be merging with the approaches of Cosmos, Polkadot, and Avalanche. For example, Optimism's "superchain" looks similar to the Cosmos Hub or Avalanche's C-Chain.

5) When configuring a portfolio of Ethereum ecosystem (ETH, L2, oracles, cross-chain bridges, applications/protocols) assets, investors have a range of choices. That said, due to the complementarity of L2 Rollups, ETH seems to offer more attractive returns. Additionally, investors should consider that sidechains like Polygon have lower "consistency" with Ethereum and act more as alternative L1s while leveraging Ethereum's network effects and EVM standards. We believe Polygon has stronger value-add potential compared to Rollups. In some ways, Polygon should be compared more with Solana than with Optimism and Arbitrum.

6) We believe the growth and scalability of Ethereum L2 will shake the value propositions of L1 competing chains that adopt similar scalability approaches—such as Cosmos, Avalanche, and Polkadot. But Solana is distinctly different because it adopts a single scaling approach (bundling settlement and execution).

Risk warning

Risk warning Risk warning

Risk warning