Uniswap: Flair will become a new standard for evaluating the competitive metrics of AMM LPs

FLAIR is the fee liquidity adjusted instantaneous yield, used to measure the competitiveness of LPs.

FLAIR is the fee liquidity adjusted instantaneous yield, used to measure the competitiveness of LPs.Title: A Metric to Evaluate LP Competitiveness in AMMs

Authors: Jason Milionis, Austin Adams, Xin Wan, Uniswap Labs

Compiled by: MK, Marsbit

Since its launch in 2018, the Uniswap protocol has processed $1.5 trillion in lifetime trading volume, pioneering the field of automated market makers (AMMs) as a cornerstone of decentralized finance (DeFi). A key feature of AMMs is that anyone can create a market and provide liquidity for any token without permission, ensuring fair competition among all market participants.

The success of these AMMs is critically dependent on the participation of liquidity providers (LPs), who provide liquidity in exchange for trading fees. Today, we are publishing new research that introduces a new metric, the Fee-Adjusted Liquidity Instantaneous Return (FLAIR), to measure LP competitiveness. Economically rational LPs will consider the costs and benefits of becoming an LP. Benefits can be quantified through trading fees, while costs are somewhat complex. In addition to market risk, LPs must also consider the maturity of their counterparts. If a trader has better market information than the LP, the LP risks losing funds in the wrong direction of the trade. A popular metric for measuring LP performance is the Loss Versus Risk (LVR), which quantifies the information imbalance between the LP and their counterpart. However, LVR does not account for a key component of AMMs: the internal competition from other LPs within the same pool.

FLAIR is a new LP competitiveness metric that complements LVR and aims to capture the dynamic behavior of LPs within a pool. FLAIR reflects reasonable economic intuition that LPs enhance competition within the pool by allocating capital to high-fee pools, adjusting liquidity within ranges, and deploying liquidity during high-fee periods. Simply put, LPs that frequently rebalance will generally earn more fees — a factor measured by FLAIR.

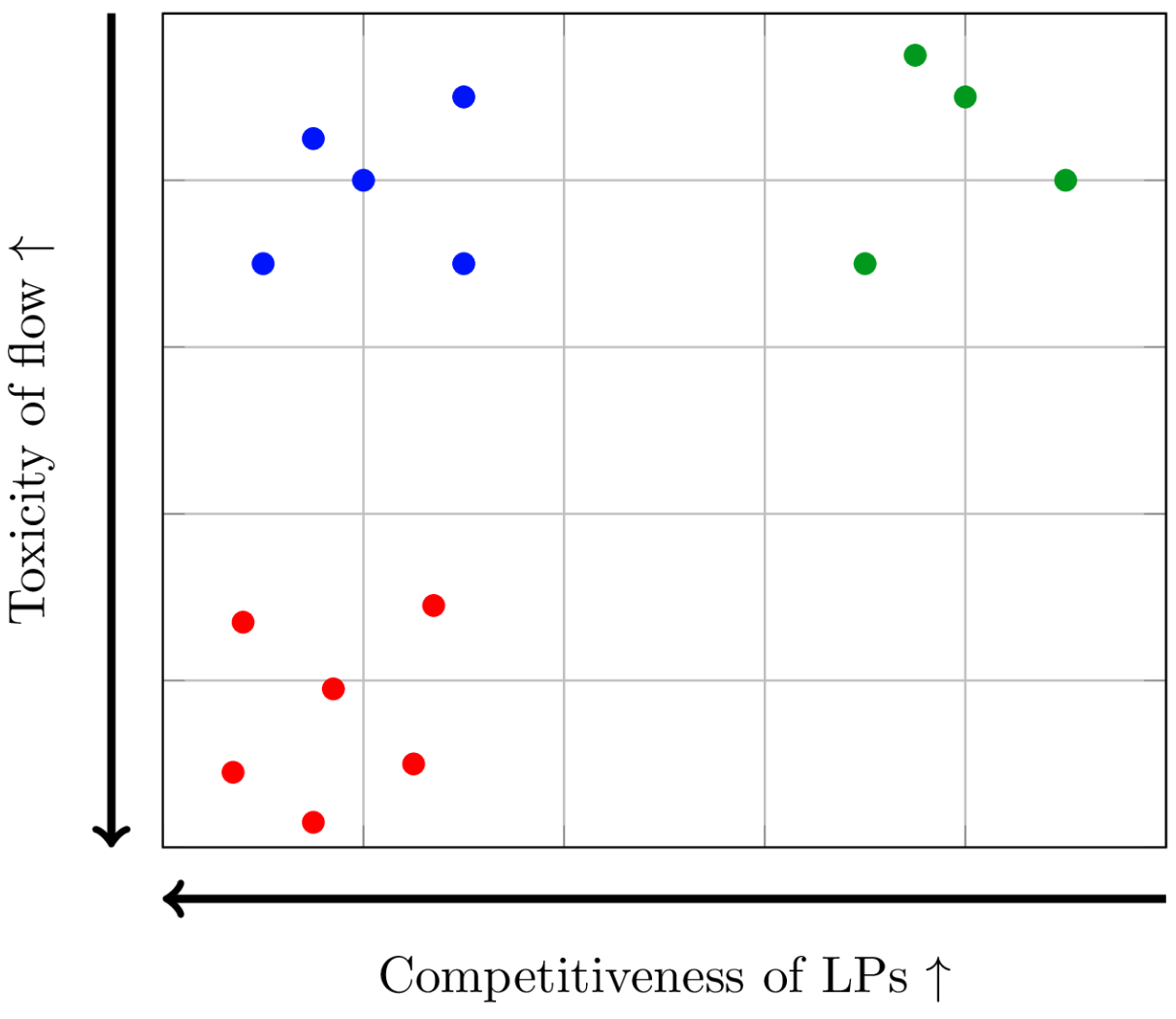

Figure 1: Existing models equate green and blue pools with low costs (LVR). However, FLAIR distinguishes these pools through LP competitiveness, showcasing an important second dimension.

FLAIR is designed to measure any number of LP positions over any time period, including a single point in time. This metric allows existing LPs to measure historical performance and enables potential LPs to optimize future capital deployment through backtesting. Researchers can also categorize different strategies and LPs based on their positions in the quadrant diagram shown in Figure 1. Finding the "optimal frontier" will be a portfolio optimization problem.

Conclusion

FLAIR is applicable not only to Uniswap v2 and v3 style liquidity pools but is also described in our work as a universal formula suitable for most typical AMMs. With some modifications, it can also be applied to traditional exchanges — allowing for comparative studies across different market structures and influencing future market design.

As liquidity supply strategies become increasingly complex, the landscape of DeFi is continuously evolving. We are excited about this future, and our contribution provides a more comprehensive perspective on LP performance. We invite interested readers to read the full paper for a more detailed understanding.

Risk warning

Risk warning Risk warning

Risk warning