A Brief Analysis of Short Selling Costs and Market Impact on the CRV Chain

In last year's CRV bull-bear battle, how was the short-selling operation carried out?

In last year's CRV bull-bear battle, how was the short-selling operation carried out?Original: 《Curve Short Selling History and Current Potential Short Selling Costs》

Author: Yilan, LD Capital

Recently, the cashing out behavior of Curve's founder and the ongoing collateralization of CRV for borrowing stablecoins have become a focal point of market attention, especially as market liquidity is affected by SEC events. To analyze the on-chain short selling costs, possibilities, and related impacts of CRV, let's first review last year's CRV long-short battle and see how past short selling operations were conducted.

Shortly after the FTX collapse last year, when market confidence was lacking and liquidity had severely shrunk, a whale borrowed a large amount of CRV tokens from Aave and transferred them to the OKX exchange, borrowing a total of 47 million CRV. Under the impact of the whale's dumping and short selling, the price of CRV dropped from $0.545 to $0.424, a decline of 21.88%, reaching a low of $0.4. This operation involved repeatedly borrowing and transferring tokens on-chain to suppress the price for large-scale short selling.

Subsequently, founder Michael purchased CRV to raise the price. Although the Aave account bore liquidation risk, the shorts still had profit potential. One way to profit was to engage in high-leverage short trades on exchanges like OKX, taking advantage of the market's lack of liquidity and absence of strong bullish interference to secure high-probability profit opportunities. Another way to profit was to convert short positions into long positions. When market liquidity was exhausted, shorts could close their positions and switch to long.

After the CRV long-short battle, Aave canceled CRV borrowing (i.e., it was no longer possible to continuously increase leverage for short selling through the same on-chain circular lending).

In addition, centralized exchanges also provided opportunities for borrowing tokens to short.

Currently, the distribution of CRV tokens is as follows: 116 million held in Curve dex, 65.47 million held by Binance, 12.56 million held by OKX, and a total of 53.29 million held by other centralized exchanges.

It can be seen that centralized exchanges hold a large amount of CRV tokens, accounting for 15% of the total circulating supply. However, due to the lack of data from centralized exchanges, it is impossible to calculate the potential costs of short selling.

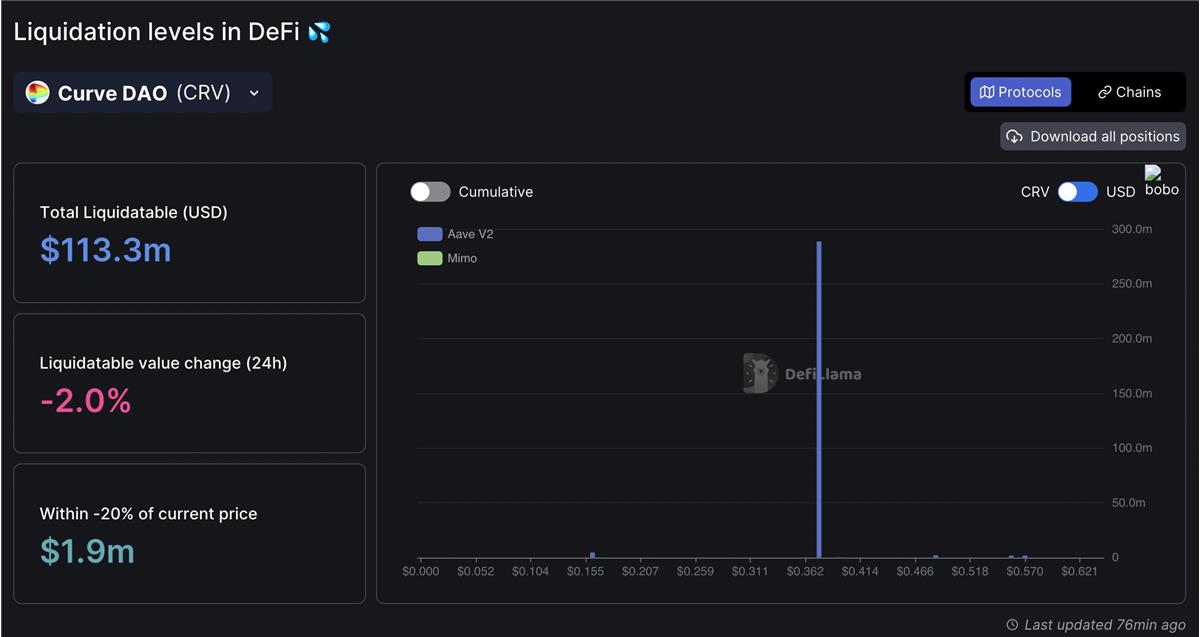

At present, the total on-chain liquidatable amount of CRV is $113 million, of which 99% (289 million CRV) is concentrated around the price of $0.375. ------ This means that borrowing tokens to short may be sufficient to push the price down to the liquidation price, but the Curve founder has the ability to add margin to continue lowering the liquidation price, making the pure short selling costs very high.

Aave starts CRV "and CRV liquidation levels

But in fact, no one can liquidate this volume of CRV, so if Aave hopes for Michael to repay his loan, lowering the LTV of the CRV lending pool is the correct risk control measure, but it should not suddenly change the LTV to 0, as this would greatly increase Aave's bad debt risk.

Although there are few ways to borrow CRV on-chain, there is significant selling pressure on on-chain CRV spot, and in the past 6 hours, short selling activities on centralized exchanges have increased significantly (190%+ APY on BN to short CRV), with OI increasing by 5 million in two hours and 14 million in 24 hours.

The founder of CRV has currently borrowed over $44 million in stablecoins from AAVE, Abracadabra, Fraxlend, Curve, and Inverse Finance. If liquidation occurs (for specific information regarding liquidation prices, see the previous thread), these lending platforms face potential bad debt risks.

However, in fact, this volume of CRV will be liquidated under conditions of significant slippage, so lowering the LTV of the CRV lending pool is the correct risk control measure, but it should be done gradually rather than suddenly changing the LTV to 0, as this would greatly increase Aave's bad debt risk.

In the past day, founder Michael withdrew over 700 wCRV (25%+) from Fraxlend and deposited it into Inverse Finance (fixed borrow rate 6.84%) at the address 0x73f8af, which was created by Inverse Finance FiRM CRV market. The founder has at least collateralized over 600 wCRV at this address, and currently, there is over 900 w TVL in the Inverse Finance CRV pool, most of which is collateralized by the CRV founder.

Additionally, 400 wCRV has also been continuously collateralized in Abracadabra, with nearly 8 million CRV in the Abracadabra CDP.

Risk warning

Risk warning Risk warning

Risk warning