DeFi Economic Model Explained: Four Incentive Models from the Perspective of Value Flow

Value Flow is not all of Tokenomics, but rather the product value flow itself based on the design of Tokenomics.

Value Flow is not all of Tokenomics, but rather the product value flow itself based on the design of Tokenomics.Source: DODO Research

I. Incentive Compatibility in Token Economics

Cryptographically-based decentralized P2P systems were not new when Bitcoin was introduced in 2009.

You may have heard of the BitTorrent protocol, commonly known as BT download, which is a P2P-based file-sharing protocol primarily used to distribute large amounts of data to users on the Internet. It utilizes some form of economic incentive; for example, "seeds" (users who upload the complete file) can achieve faster download speeds. However, this early decentralized system, launched in 2001, still lacked a well-designed economic incentive structure.

The lack of economic incentives stifled these early P2P systems, making it difficult for them to thrive over time.

(Coincidentally, in 2019, the developers of the BitTorrent protocol launched BitTorrent Token (BTT), which was later acquired by TRON. They chose to utilize cryptocurrency to provide economic incentives to improve the performance and interaction of the BitTorrent protocol. For example, users can spend BTT to increase their download speeds or earn BTT by sharing files.)

In 2009, when Satoshi Nakamoto created Bitcoin, he introduced economic incentives into P2P systems.

From DigiCash to Bit Gold, multiple experiments aimed at creating decentralized digital cash systems had not fully resolved the Byzantine Generals Problem. However, Nakamoto implemented a Proof-of-Work consensus mechanism combined with economic incentives, solving this seemingly unsolvable problem of how to achieve consensus among nodes. Bitcoin not only provided a means of value storage for those wanting to replace the existing financial system; it also combined cryptocurrency with incentives to offer a new, universal design and development approach, ultimately forming the powerful and vibrant P2P payment network we see today.

From Nakamoto's "Galileo Era," cryptoeconomics has evolved into Vitalik's "Einstein Era."

More expressive scripting languages have enabled the implementation of complex transaction types, giving birth to a more universal decentralized computing platform. After Ethereum switched to Proof-of-Stake (PoS), token holders became validators of the network and earned more tokens in this way. Beyond the controversy, compared to Bitcoin's current ASIC mining method, this is indeed a "more inclusive token distribution method."

Designing a token economic model (Tokenomics) is essentially designing an "incentive-compatible" game mechanism. - Hank, BuilderDAO

Incentive Compatibility is an important concept in game theory, first introduced by economist Roger Myerson in his classic work "The Theory of Cooperative Games," published in 1991, which has become a significant reference in the field of game theory. In this book, Myerson elaborates on the concept of incentive compatibility and its importance in game theory.

Its academic definition can be understood as: a mechanism or rule design in which participants act according to their true interests and preferences without resorting to fraud, cheating, or dishonest behavior to pursue better outcomes. This game structure allows individuals to maximize their personal interests while collectively achieving maximum benefits. For example, in Bitcoin's design, when expected income > input costs, miners will continue to invest computing power to maintain the network, and users can continue to conduct secure transactions on the Bitcoin ledger—this trust machine now stores over $40 billion in value and processes transactions worth over $600 million daily.

In Tokenomics, using token incentives and rules to guide the behavior of multiple participants, achieving better incentive compatibility in design, and expanding the scale and limits of decentralized structures or economic benefits is an eternal proposition.

Tokenomics plays a decisive role in the success or failure of cryptocurrency projects. How to design incentives to achieve incentive compatibility is crucial in the success or failure of Tokenomics.

This is similar to how monetary policy and fiscal policy relate to national governments.

When a protocol acts as a nation, it needs to formulate monetary policy, such as token issuance rates (inflation rates), and decide under what conditions to mint new tokens. It needs to regulate fiscal policy to adjust taxes and government spending, usually manifested as transaction fees and treasury funds.

This is complex. As proven by humanity's economic experiments and governance constructions over the past few thousand years, designing a model to coordinate human nature and economics is incredibly challenging. There have been errors, wars, and even regressions. In less than twenty years, Crypto also needs to create better models through these iterative trial-and-error processes (e.g., the Terra incident) to welcome a long-term successful and resilient ecosystem. This is clearly a reset of thinking that the market needs during the long crypto winter.

II. Different Categories, Goals, and Designs of Economic Models

When designing economic models, we need to clarify the target of token design. Public chains, DeFi (Decentralized Finance), GameFi (Gamified Finance), and NFTs (Non-Fungible Tokens) are different categories of projects in the blockchain field, and they have some differences in designing economic models.

Public chain token design is more like macroeconomics, while others are closer to microeconomics; the former needs to focus on the overall supply-demand dynamic balance within the entire system and ecosystem, while the latter focuses on the supply-demand relationship between products and users/markets.

Different categories of projects have entirely different design goals and core points for their economic models. Specifically:

Public Chain Economic Model: Different consensus mechanisms determine the different economic models of public chains. However, the common goal of their economic model design is to ensure the stability, security, and sustainability of the public chain. Therefore, the core lies in using token incentives to validate participants, attract enough nodes to participate, and maintain the network. This usually involves the issuance of cryptocurrencies, incentive mechanisms, and rewards and governance for nodes to keep the economic system continuously stable.

DeFi Economic Model: Tokenomics originated from public chains but has developed and matured in DeFi projects, which will be analyzed in detail later. The economic model of DeFi projects typically involves lending, liquidity provision, trading, and asset management. The design goal of the economic model is to encourage users to provide liquidity, participate in lending and trading activities, and offer corresponding interest, rewards, and returns to participants. In DeFi economic models, the design of the incentive layer is core, such as how to guide token holders to hold tokens instead of selling them, and how to coordinate the distribution of interests between LPs and governance token holders.

GameFi Economic Model: GameFi is the concept of combining gaming and financial elements, aiming to provide financial rewards and economic incentives for gamers. The economic model of GameFi projects typically includes the issuance, trading, and profit distribution of in-game virtual assets. Compared to DeFi projects, the model design of GameFi is more complex, with transaction fees as the core of revenue determining how to increase users' reinvestment demand becoming the primary focus of economic model design, but it naturally poses design challenges for the playability of game mechanics. This makes most projects inevitably exhibit Ponzi structures and spiral effects.

NFT Economic Model: The economic model of NFT projects typically involves the issuance, trading, and rights of NFT holders. The design goal of the economic model is to provide NFT holders with opportunities to create value, trade value, and earn profits, encouraging more creators and collectors to participate. This can be further subdivided into NFT platform economic models and project economic models. The former's competitive point lies in royalty fees, while the latter focuses on how to solve economic scalability, such as increasing repeat sales revenue and fundraising in different fields (refer to Yuga Labs).

Although these projects have their unique economic model designs, they may also have overlapping and intersecting aspects. For example, DeFi projects can integrate NFTs as collateral, and GameFi projects can use DeFi mechanisms for fund management. In the evolution of economic model design, whether at the business level or incentive level, the development of DeFi projects is richer, and many models of DeFi are also widely used in GameFi, SocialFi, and other projects. Therefore, the design of DeFi's economic model is undoubtedly a field worth in-depth study.

III. Analyzing DeFi Economic Models from the Perspective of Incentive Patterns

If we categorize DeFi economic models based on different project business logics, we can roughly divide them into three main categories: DEX, Lending, and Derivatives. If we categorize them based on the characteristics of the incentive layer of the economic model, we can further divide them into four patterns: Governance Model, Staking/Cash Flow Model, Vote Escrow "including ve and ve(3,3) models," and es Mining Model.

Among them, the governance model and staking/cash flow model are relatively simple, represented by projects such as Uniswap and SushiSwap. A brief summary is as follows:

Governance Model: Tokens only have governance functions over the protocol; for example, UNI represents governance rights over the protocol. The Uniswap DAO is the decision-making body of Uniswap, where UNI holders can propose and vote on decisions that affect the protocol. Major governance matters include managing the UNI community treasury, adjusting fee rates, etc.

Staking/Cash Flow Model: Tokens can bring continuous cash flow; for example, when Sushiswap launched, it quickly attracted liquidity by distributing its token SUSHI to early LPs, completing a "vampire attack" on Uniswap. Moreover, in addition to transaction fees, SUSHI tokens also enjoy the right to distribute 0.05% of protocol revenue.

They each have their advantages and imperfections. UNI's governance function has been criticized for failing to bring value realization and not rewarding early LPs and users who took on significant risks; while Sushi's excessive issuance has led to a price drop, with some liquidity being migrated back from Sushiswap to Uniswap.

In the early development of DeFi projects, these two were relatively common economic models. Later economic models iterated on this foundation. Next, we will focus on analyzing the Vote Escrow and es Mining models in conjunction with Token Value Flow.

This article primarily employs the Value Flow method to study projects, aiming to abstract the value flow of projects, including the real income of the protocol, the redistribution paths of income within the protocol, the incentive links, and the flow of tokens. All of this constitutes the core business model of the protocol and is continuously adjusted and optimized through Value Flow. Although Value Flow does not encompass all of Tokenomics, it is the product value flow based on Tokenomics design. On this basis, when combined with factors such as the initial distribution and unlocking of tokens, it can comprehensively present the Tokenomics of a protocol. In this process, the supply and demand relationship of tokens is adjusted, thereby achieving value capture.

IV. Vote Escrow

The birth of Vote Escrow (vote escrow) stems from the dilemmas faced by early DeFi projects regarding mining and withdrawals, with the solution focusing on how to stimulate users' motivation to hold tokens and how to coordinate multiple interests to contribute to the long-term development of the protocol. After Curve first proposed the ve model, subsequent protocols iterated and innovated on the economic model based on Curve, primarily still revolving around the ve model and ve(3,3) model.

ve Model: The core mechanism of ve is that users obtain veToken by locking tokens. veToken is a non-transferable and non-circulating governance token; the longer the lock-up period chosen (usually with a maximum lock-up time), the more veToken can be obtained. Based on the weight of their veToken, users can acquire corresponding voting rights. The voting rights are reflected in the ability to determine the allocation of liquidity pool rewards for newly issued tokens, thereby having a substantial impact on users' personal gains and enhancing their motivation to hold tokens.

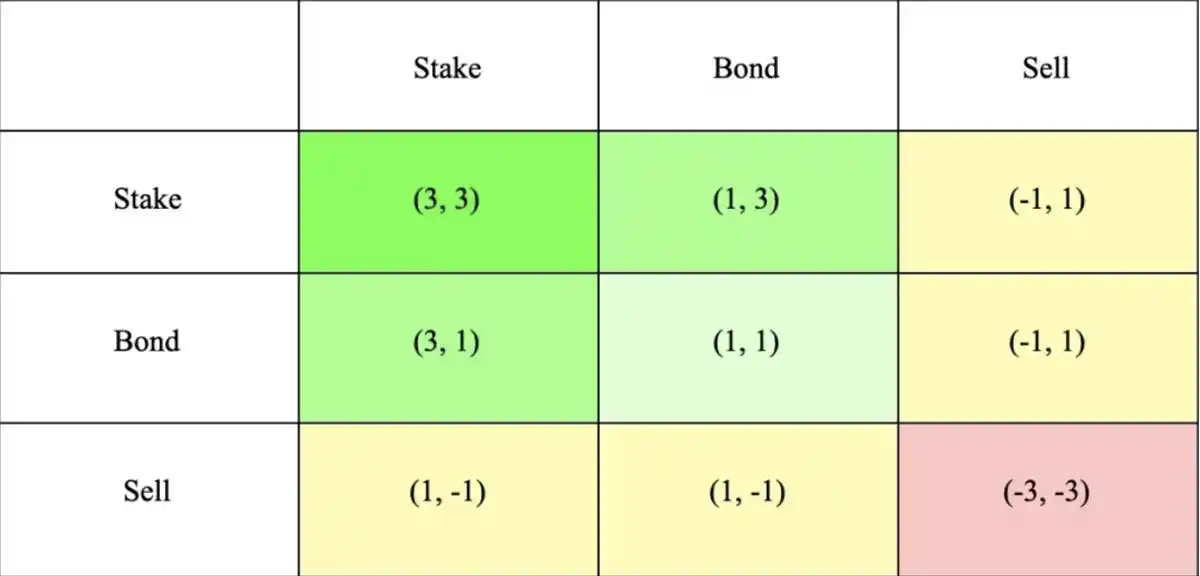

ve(3,3) Model: The VE(3,3) model combines Curve's ve model with OlympusDAO's (3,3) game theory. (3,3) refers to the game outcomes based on different behavioral choices of investors. The simplest Olympus model includes two investors who can choose among three actions: staking, bonding, or selling. As shown in the table below, when both investors choose to stake, the joint profit is maximized, reaching (3,3), which aims to encourage cooperation and staking.

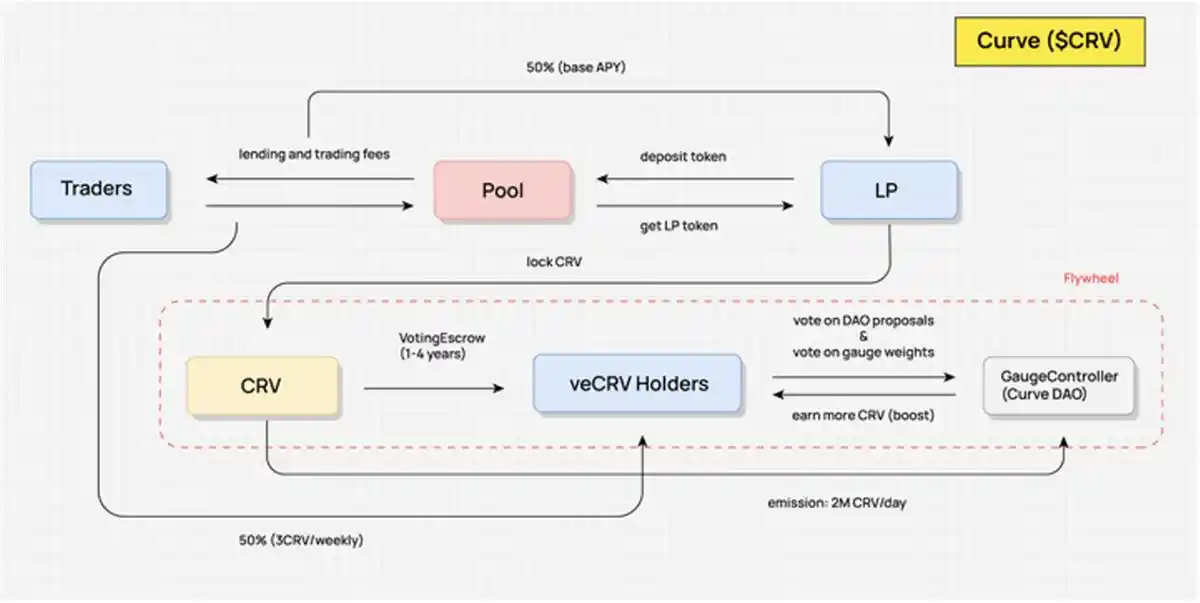

Curve - The Pioneer of the ve Model

In the diagram below regarding Curve's value flow, we can see that CRV holders cannot share any related benefits of the protocol; only when LP locks their CRV to obtain veCRV can they capture the value of the protocol, which is reflected in: transaction fees, accelerated market-making rewards, and governance voting rights of the protocol.

Transaction Fees: After users lock CRV tokens, they receive 0.04% of the transaction fee share from most trading pools based on the number of veCRV staked, with the share rate being 50% of the total fees (the other 50% goes to liquidity providers), and the share is distributed through the 3CRV token.

Market-Making Reward Acceleration: Curve liquidity providers can increase their CRV reward earnings through the Boost feature after locking CRV, thereby enhancing their overall APR from market-making; the CRV required for Boost is determined by the pool and the amount of funds from LP.

Governance Voting Rights of the Protocol: Curve's governance also requires veCRV to be realized, with governance scope including protocol parameter modifications, voting on new liquidity pools for Curve, and the weight distribution of CRV liquidity incentives among various trading pools, etc.

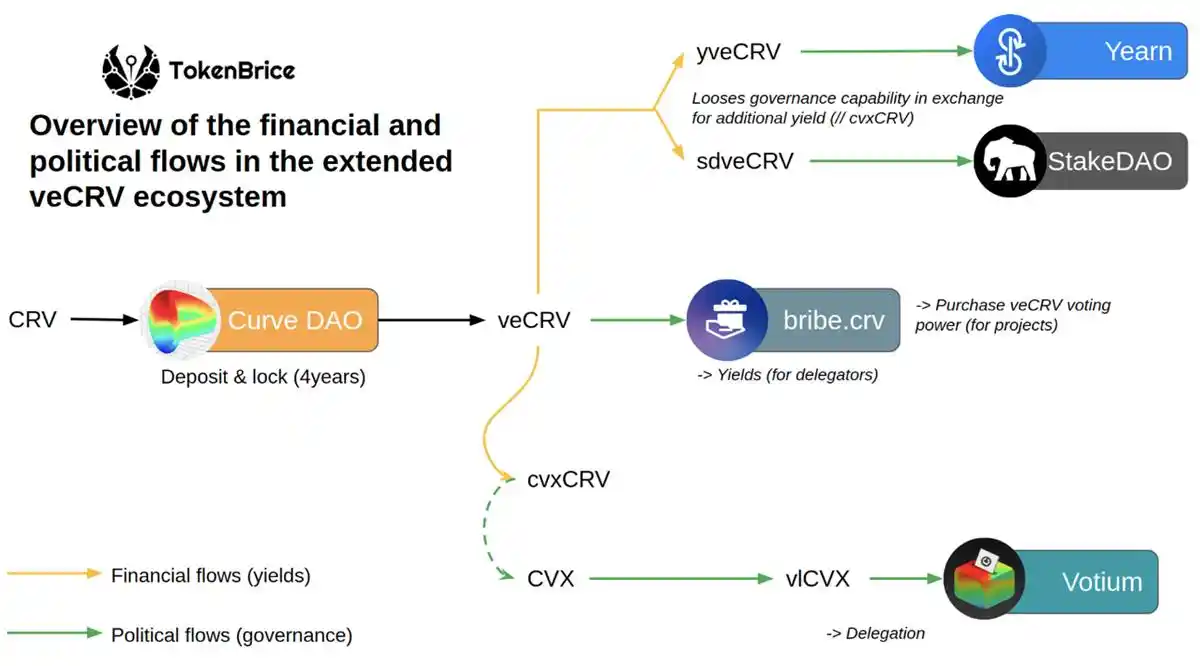

Additionally, holding veCRV can also yield the potential airdrop of tokens from other projects supported and partnered with Curve, such as the token CVX from the liquidity and CRV staking management platform Convex, which will airdrop 1% of the total supply to veCRV users.

It can be seen that CRV and veCRV capture the overall value of the protocol quite effectively, not only allowing for the sharing of protocol fee distributions and accelerated market-making rewards but also playing a significant role in governance, which creates enormous demand and stable buying pressure for CRV.

Due to the strong demand for anchoring and liquidity from stable asset operators for their issued assets, establishing liquidity pools on Curve and obtaining CRV liquidity mining incentives to maintain sufficient trading depth has almost become their inevitable choice. The competition for CRV produced daily for liquidity mining incentives is determined by Curve's DAO core module "Gauge Weight Voting." Users can vote in "Gauge Weight Voting" with their veCRV to decide the distribution ratio of CRV among various liquidity pools for the next week; pools with higher distribution ratios are more likely to attract sufficient liquidity.

This war without gunpowder is a competition for "the right to list tokens" and "the right to allocate liquidity incentives." Of course, by obtaining governance rights through CRV, these projects will also receive stable dividends from the Curve platform as a source of cash flow. The competition and internal strife among various projects on Curve have generated continuous demand for CRV, stabilizing its price under massive issuance and supporting Curve's market-making APY, attracting liquidity, and achieving a cycle. Thus, the war for CRV has given rise to a complex bribery ecosystem based on veCRV. As it stands, as long as Curve continues to dominate the stable asset exchange field, this war will not end.

We can briefly summarize the obvious advantages and disadvantages of the veCRV mechanism:

1. Advantages

Locking reduces liquidity, decreases selling pressure, and helps stabilize the token price (currently, 45% of CRV is locked for voting, with an average lock-up duration of 3.56 years);

Aligns the long-term interests of all parties (veCRV holders also enjoy fee sharing, meaning the interests of liquidity providers, traders, token holders, and the protocol are coordinated together);

Time and quantity weighting allows for better governance possibilities.

2. Disadvantages

Over half of the governance rights on Curve are concentrated in Convex (53.65%), leading to a significant concentration of governance power;

Liquidity within Curve has not been fully utilized (the boost mining rewards and governance voting rights obtained from locking CRV are limited to that address and cannot be transferred; the high subsidies attracted a large amount of liquidity, but this liquidity has not utilized its high liquidity functionality, thus failing to generate external revenue);

The rigid lock-up period is not friendly enough for investors; four years is too long for the crypto industry.

Innovations on the veToken Mechanism

In a previous article by DODO Research, we detailed the five innovations in incentive design of the veToken model. Each protocol has made different adjustments at key levels of the mechanism based on its needs and focus. Specifically categorized as:

Designing veNFT to improve the liquidity issue of vetokens

How to better allocate token releases to vetoken holders

Incentivizing the healthy development of liquidity pool trading volume

Layering the revenue structure to provide users with choices

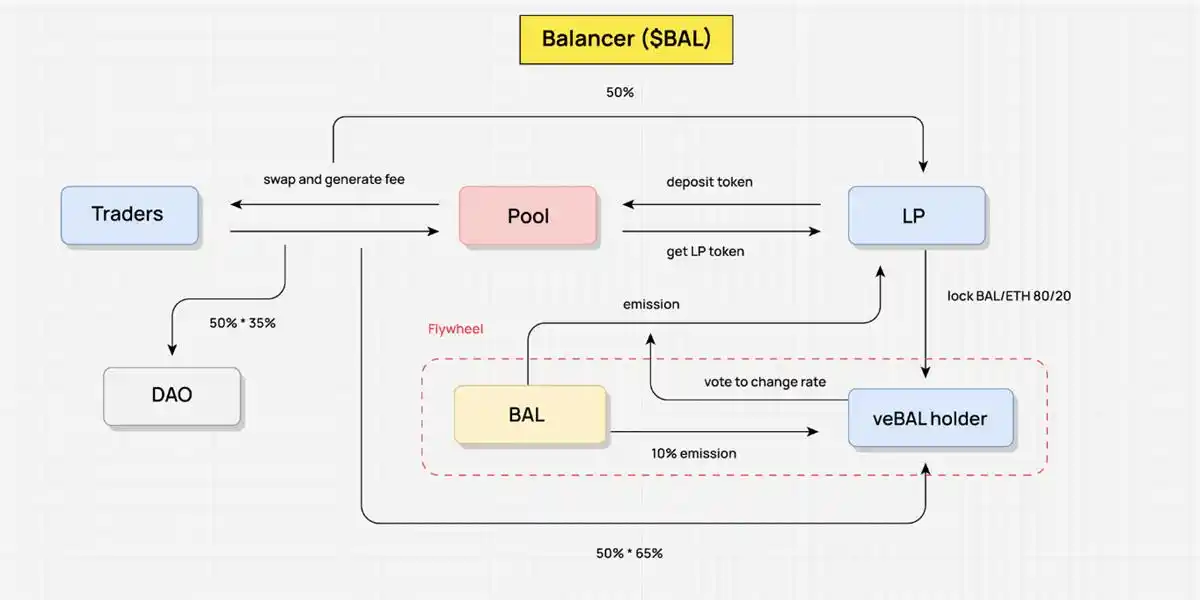

Taking Balancer as an example. In March 2022, Balancer launched version V2, modifying its original economic model. Users can lock BPT (Balancer Pool Token) of the 80/20 BAL/WETH pool to obtain veBAL, thereby deeply binding Balancer V2's governance rights and protocol dividend rights with veBAL.

Users must lock BAL and WETH tokens in an 80:20 ratio, rather than just locking BAL—using locked LP tokens instead of single token locks can increase market liquidity and reduce volatility. Compared to Curve's veCRV, veBAL has a maximum lock-up period of one year and a minimum lock-up period of one week. This significantly reduces the lock-up duration.

Regarding fee sharing, 50% of the protocol fees obtained by Balancer will be distributed to veBAL holders in the form of bbaUSD. The remaining Boost, Voting, and governance rights are not much different from Curve.

It is worth mentioning that to address the "liquidity waste—unable to generate external revenue for the product" issue present in the vetoken model, Balancer utilizes the Yield-bearing Trading Pool Boosted Pool mechanism to increase LP earnings (the LP tokens issued by the LP pool are called bb-a-USD, which can be paired with various assets in AMM pools, achieving asset leverage through the issuance of LP tokens, thereby increasing LP earnings).

Later, Core Pools were proposed (to improve the original Boosted Pools, which only benefited LPs), where the official bribed veBAL holders to vote for Core Pools, resulting in a significant amount of $BAL shifting towards Core Pools, increasing external yield asset revenue and altering the revenue structure of the Balancer protocol itself.

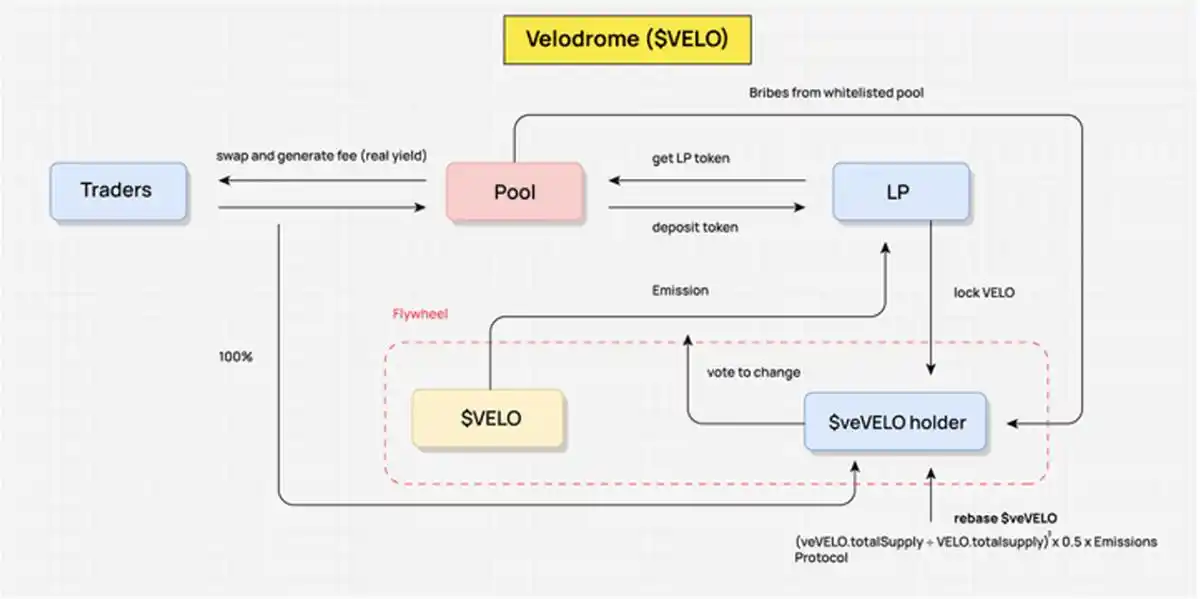

Velodrome: The Most Representative ve(3,3)

Before discussing Velodrome, let's briefly define ve(3,3): Curve's veCRV economic structure + Olympus's (3,3) game theory.

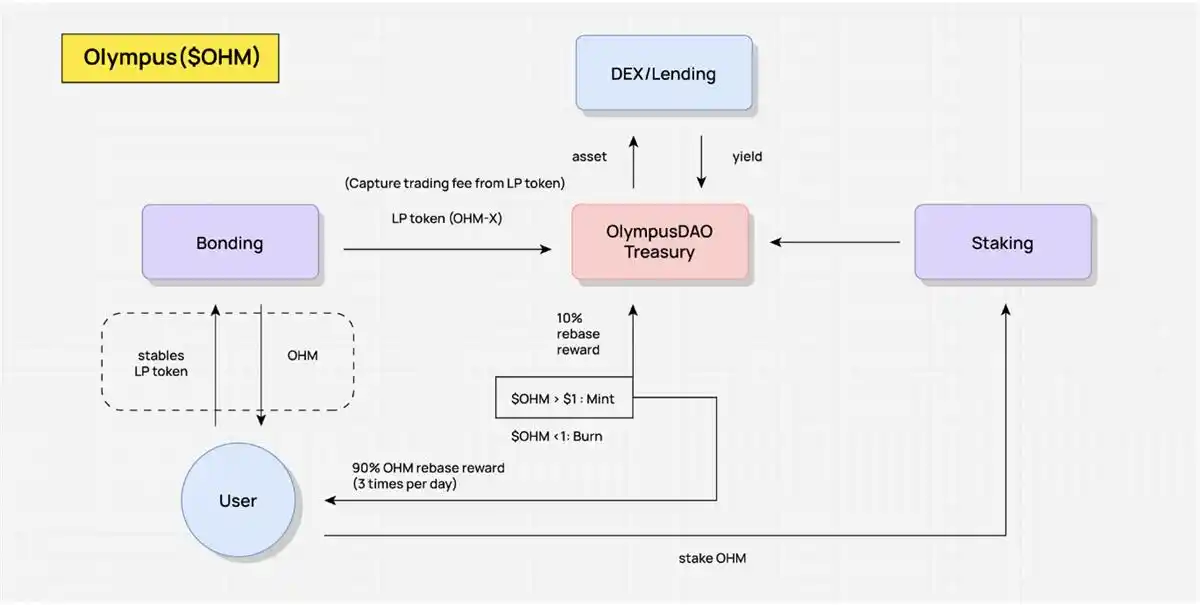

As shown in the diagram below, the incentives in Olympus mainly come in two forms: one is the bonding mechanism, and the other is the staking mechanism. Olympus officially sells OHM below market price to users in the form of bonds, obtaining assets such as USDC and ETH from users, which supports the treasury with valuable assets and generates OHM distributed to OHM stakers through the Rebase mechanism. Ideally, as long as users choose to stake long-term, known as (Stake, Stake)—that is (3,3), the OHM balance in their positions can continuously compound, creating a positive feedback loop for stakers with high APR. However, if there is significant selling pressure on OHM in the secondary market, this flywheel cannot sustain. This is, of course, a game of strategy, with the ideal state being Nash equilibrium, achieving a win-win situation.

At the beginning of 2022, Andre Cronje launched Solidly on Fantom, with its core being veNFT and voting rights optimization. The veSOLID position is represented by veNFT, which seems to liberate liquidity; even if users transfer NFTs, any NFT holder has voting rights to decide on reward distribution; veSOLID holders will receive a certain base amount proportional to the weekly emission, allowing them to maintain voting shares even without locking new tokens; at the same time, stakers receive 100% of transaction fees but can only earn rewards from pools they voted for, avoiding situations where Curve voters vote for pools just to receive bribes.

AC announced on Twitter that the issuance of Solidly's token ROCK would be directly airdropped to the top 20 protocols with the highest lock-up amounts on the Fantom protocol, igniting vampire attacks among protocols on the Fantom chain, leading to the emergence of 0xDAO and veDAO, and initiating a TVL war. A few months later, the veDAO team incubated another project of ve(3,3), Velodrome.

So why did Velodrome Solidly become the standard fork template on layer 2s like Arbitrum or zkSync?

In the initial design, Solidly had some key weaknesses, such as high inflation and completely permissionless—allowing any pool to receive SOLID rewards, leading to a proliferation of air tokens. Rebase or "anti-dilution" did not bring any value to the entire system.

What changes did Velodrome make?

The Pool for Velo token incentive distribution adopts a whitelist mechanism, which is currently open for applications without going through on-chain governance processes (avoiding voting to decide token incentives);

For liquidity bribery rewards for Pools, they can only be claimed in the next cycle;

*(veVELO.totalSupply VELO.totalsupply)³ 0.5 emission rate—* reduced the issuance reward ratio for ve token holders, under the adjusted model of Velo, veVELO users will only receive 1/4 of the total emissions compared to the traditional model. This improvement has significantly weakened the (3,3) part of the ve(3,3) mechanism;

The LP Boost mechanism has been removed;

3% of Velo's emissions will be allocated as operational expenses;

Exploration of extensions to the veNFT mechanism: including trading veNFT even during staking/voting, veNFT can be split, and veNFT lending, etc.;

More reasonable token distribution and issuance rhythm: Velodrome distributed 60% of the initial supply to the community on the first day of the project launch, bundling with the Optimism team to assist in cold start, and airdropped several protocols with veVELO NFTs without additional conditions, greatly helping attract initial voting and bribery activities.

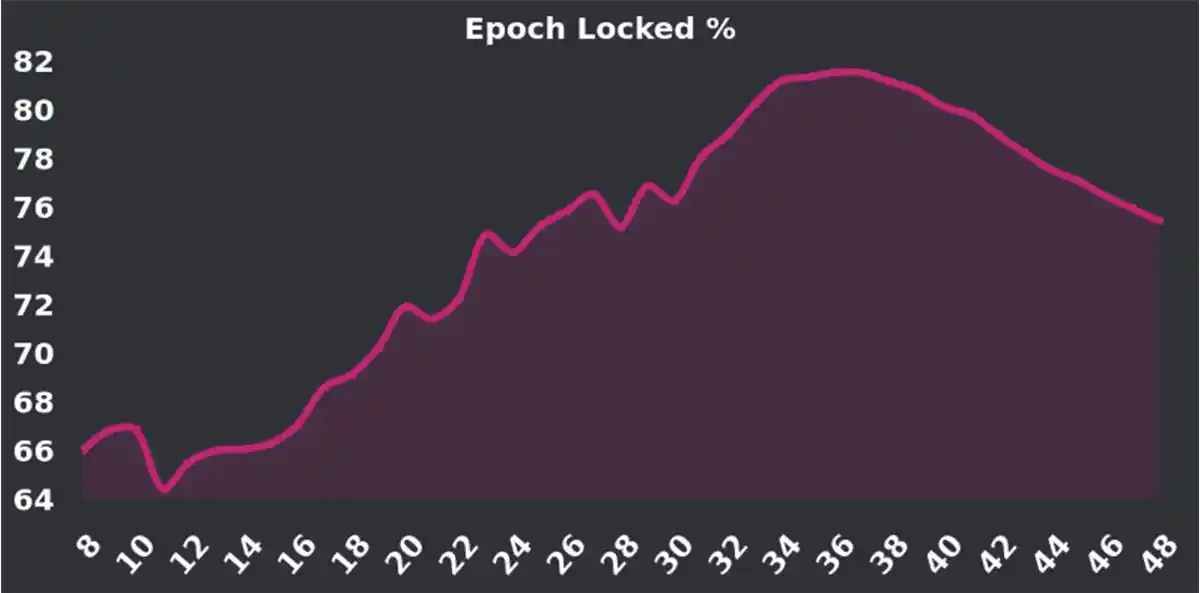

After launch, Velo's staking rate has been on the rise, with a peak of 70%-80% being a high lock-up ratio (the current staking rate of Curve, which also uses the ve model, is 38.8%). Many people questioned whether the incentive for lock-up would further decline as the "Tour de OP" plan that started in November last year came to an end, potentially creating selling pressure. However, Velo's staking rate still maintains a good level (~70%). The upcoming V2 upgrade also aims to encourage more holders to lock their tokens, which is worth keeping an eye on.

V. ES Mining Model

ES: A Game of Real Returns, Incentivizing Loyal Users to Participate

The ES mining model is an engaging and challenging new Tokenomics mechanism, with its core idea being to lower the cost of protocol subsidies by reducing unlocking thresholds and enhancing its appeal and inclusivity through incentivizing real user participation.

In the ES model, users can earn ES Tokens as rewards by staking or locking their tokens. Although this reward makes the yield appear higher, in reality, due to the existence of unlocking thresholds, users cannot immediately cash out these earnings, complicating and making real yield calculations unpredictable. This aspect both increases the challenge of the ES model and enhances its attractiveness.

Compared to traditional ve models, the ES model has a clear advantage in terms of the cost of protocol subsidies, as its design reduces the subsidy costs due to the unlocking thresholds. This makes the ES model closer to reality in the game of distributing real returns, thus being more universal and inclusive, potentially attracting more users to participate.

The essence of the ES model lies in its ability to incentivize real user participation. If users leave the system, they will forfeit the rewards of ES Tokens, meaning the protocol does not need to pay additional token incentives. As long as users remain within this system, they can receive ES Token rewards, even though these rewards cannot be quickly realized. This design encourages the participation of real users, maintains user activity and loyalty, while not imposing excessive incentives on users. By controlling the ratio of spot staking or locking and the unlocking cycle, the project itself can achieve more interesting and attractive token unlocking curves.

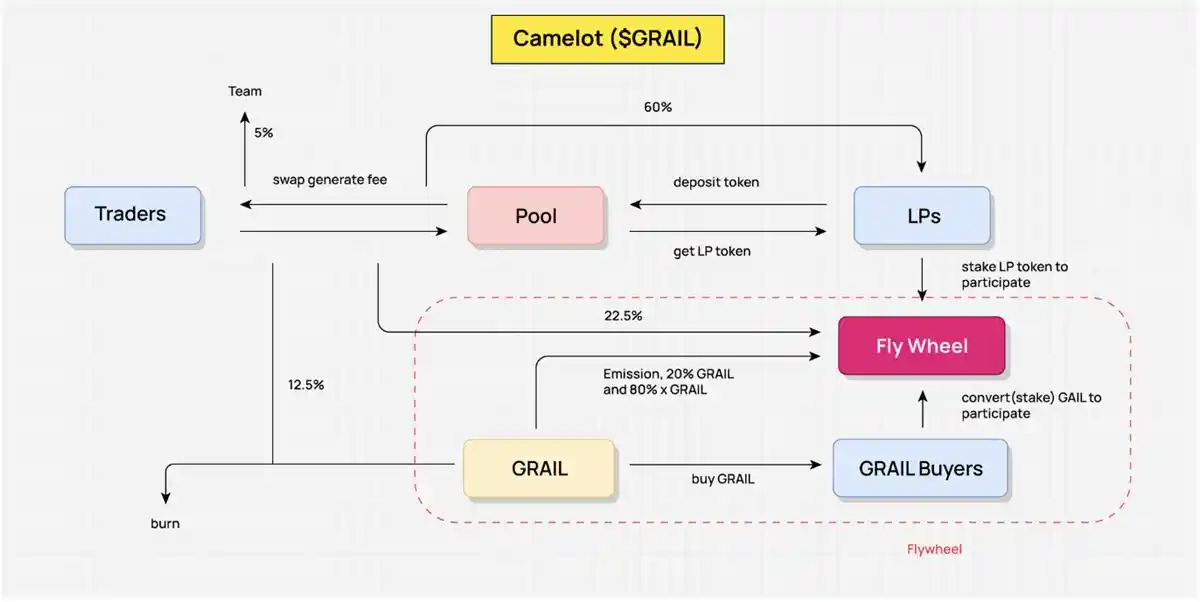

Camelot - Introducing Partial ES Mining Incentives

In exploring Camelot's value flow, abstracting Camelot's value flow clearly demonstrates how Camelot's tokenomics works. Here, we do not elaborate on every link in detail but abstractly showcase the main parts of value flow for a better understanding of its overall framework.

The core incentive goal of Camelot is to encourage liquidity providers (LPs) to continuously provide liquidity, ensuring that traders can enjoy a smooth trading experience and sufficient liquidity. This design ensures the smoothness of transactions through incentive mechanisms and helps LPs and traders share the generated profits.

The real income of the Camelot protocol comes from the fees generated by the interaction between traders and pools. This is the protocol's real revenue and the main source for redistributing income. In this way, Camelot ensures the sustainability of its economic model.

Regarding income redistribution, 60% of the fees will be distributed to LPs, 22.5% will be redistributed to the flywheel, 12.5% will be used to purchase GRAIL and burn it, while the remaining 5% will be allocated to the team. This redistribution mechanism ensures the fairness of the protocol while providing motivation for continuous operation.

Additionally, this income distribution also encourages and drives the operation of the flywheel. To obtain redistributed income, LPs must stake LP tokens, which indirectly incentivizes them to provide liquidity for a longer time. Besides the 22.5% of real income from fees, Camelot also allocates 20% of GRAIL tokens and xGRAIL (ES tokens) as incentives. This strategy not only incentivizes LPs but also encourages ordinary users to participate in income distribution by staking GRAIL, enhancing the overall activity and attractiveness of the protocol.

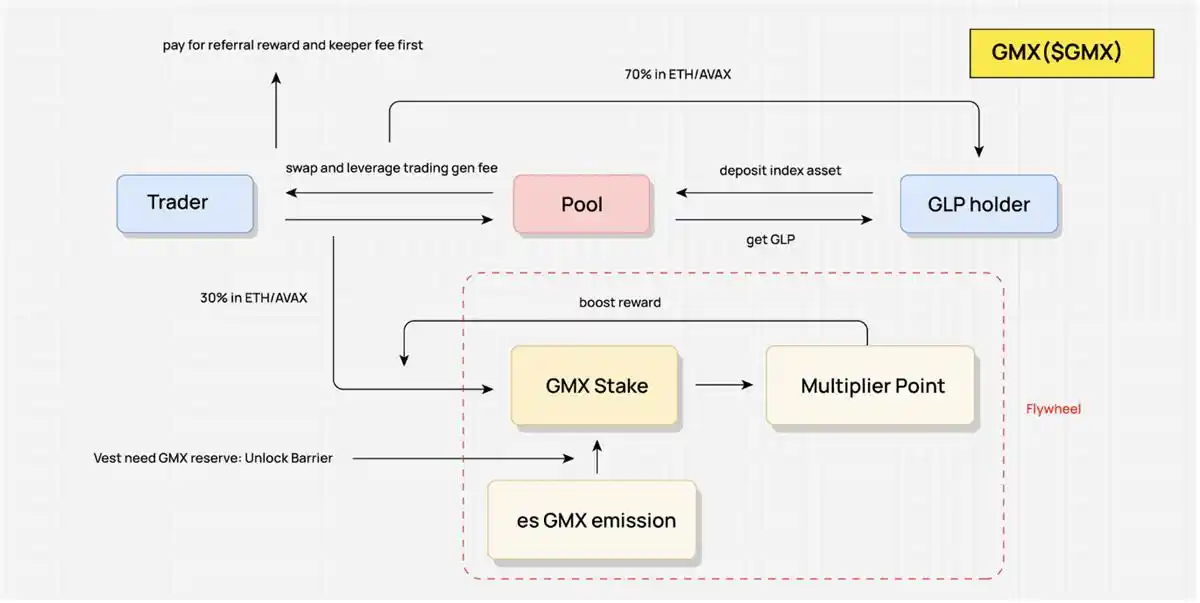

GMX - Encouraging Competition for Real Income Distribution

GMX's token economic model (tokenomics) is a highly interesting and interactive design, with its core goal being to achieve a continuous supply of liquidity and encourage traders and liquidity providers (LPs) to keep trading. This design aims to ensure the liquidity and trading volume of the protocol while incentivizing the continuous locking of GMX.

The real income of this model comes from the fees generated by traders conducting swaps and leveraged trades, which is the main source of income for the protocol. To ensure fair income distribution, the revenue is first used to deduct referral fees and keeper fees. The remaining portion, 70%, is allocated to GLP holders (essentially LPs), while the remaining 30% is redistributed. GMX uses a game mechanism to distribute this portion of income, which is also the core mechanism of this model.

GMX's core game mechanism is designed to redistribute 30% of the real income. This ratio is fixed, but GMX holders can influence the proportion of income they can receive through different strategies. For example, users can stake GMX to earn esGMX rewards, while unlocking esGMX requires GMX spot staking and meeting certain unlocking periods. Additionally, staking GMX will also earn Multiplier Points; although this part of the reward cannot be directly realized, it can increase the user's profit-sharing ratio.

In this game mechanism, GMX, esGMX, and Multiplier Points all have weight in profit-sharing. The only difference is that Multiplier Points cannot be realized; esGMX requires gradual unlocking through GMX staking; while GMX can be quickly realized but will clear Multiplier Points and forfeit esGMX rewards.

This design allows users to formulate strategies based on their needs. For example, users seeking long-term returns can choose to continue locking to gain maximum weight and achieve higher relative returns. Conversely, if users want to quickly exit the protocol, they can choose to withdraw and realize all staked GMX, leaving unrealized esGMX rewards within the protocol, meaning the protocol does not need to issue actual subsidies but instead distributes the real income generated during this period to users.

GMX's token economic model encourages GLP holders to continuously provide liquidity and fully utilizes the value of real income redistribution. This makes the continuous locking of GMX possible, further strengthening the stability and attractiveness of its economic model.

VI. Core Elements in DeFi Economic Model Design from the Perspective of Value Flow

In DeFi economic model design, core elements include fundamental value, token supply, demand, and utility. These constituent elements are relatively discrete and have not been intuitively combined in previous analyses. The Value Flow method used in this article abstracts the value flow within the protocol by studying the Tokenomics mechanism of projects, combined with product logic, to comprehensively analyze the value flow of a project, including the composition of the flywheel, the direction of income distribution, the incentive links, and combined with the distribution of tokens and unlocking cycles, etc., providing a clear understanding of a project's Tokenomics.

Below is the Value Flow that was not detailed in the previous text due to space constraints:

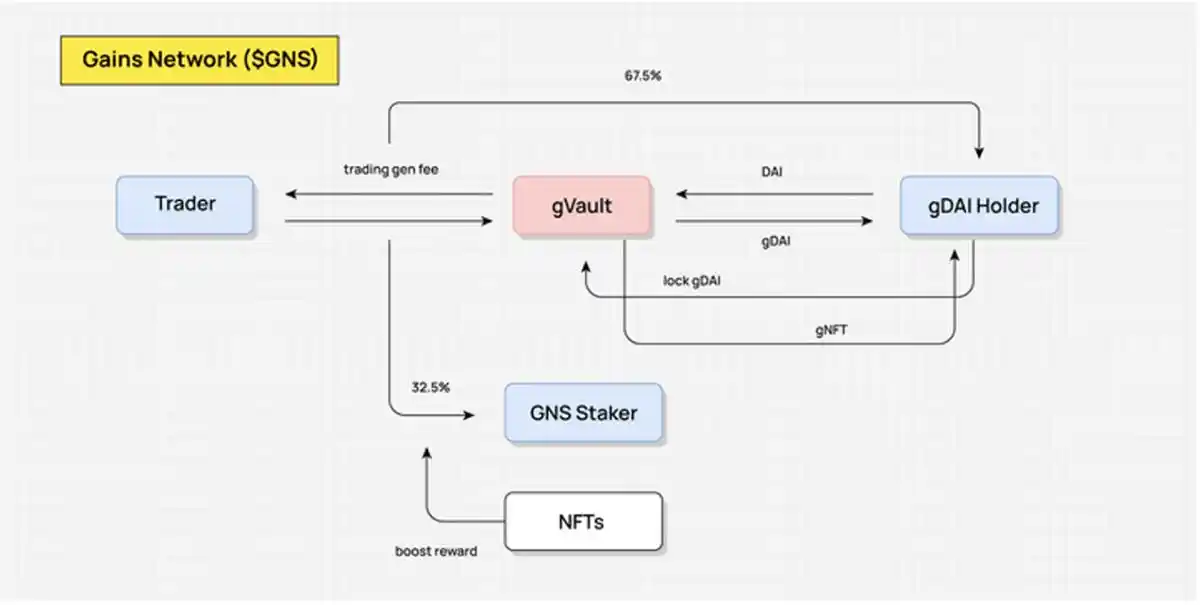

GNS Value Flow (realizing membership mechanisms through NFTs to redistribute income) diagram: DODO Research

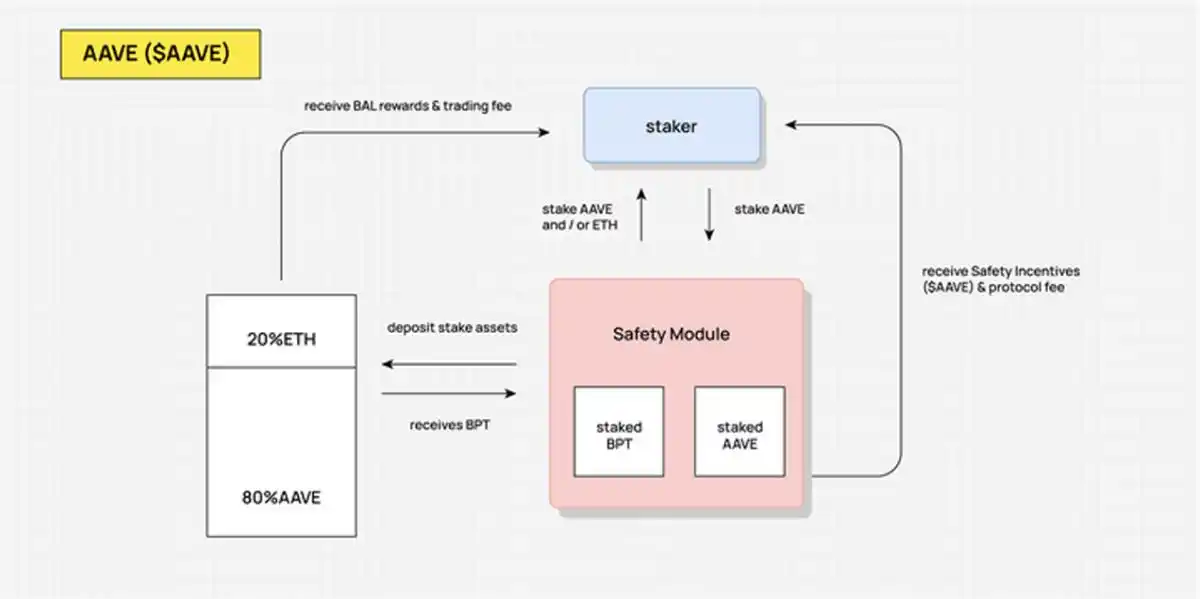

AAVE Value Flow (users staking AAVE to share part of the protocol income) diagram: DODO Research

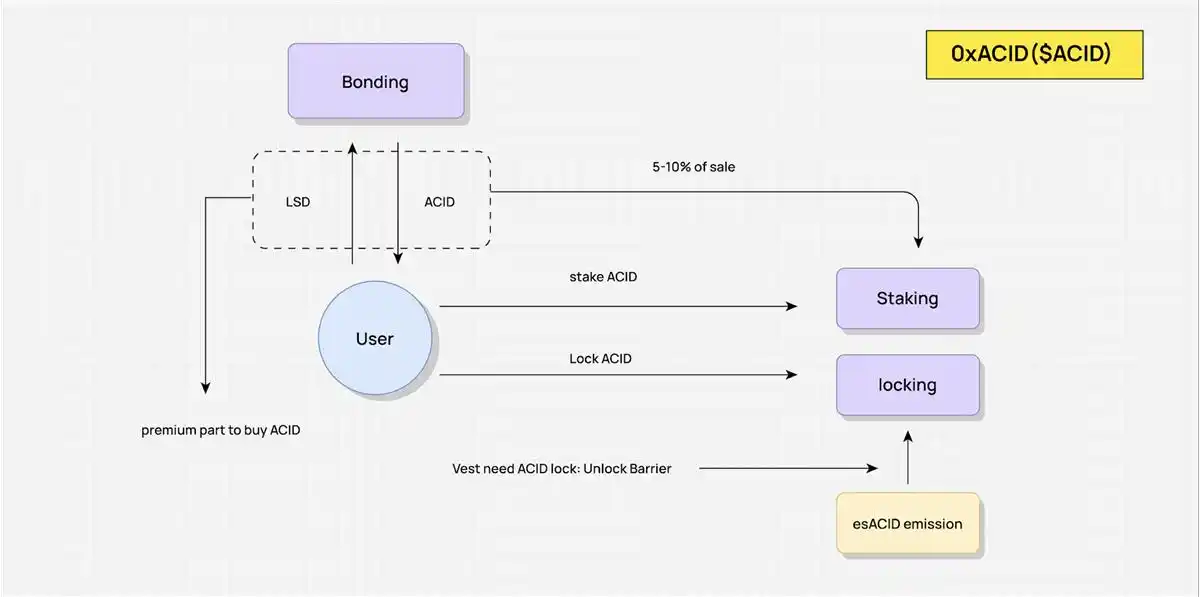

ACID Value Flow (combining es mechanism and Olympus DAO mechanism to realize the flywheel) diagram: DODO Research

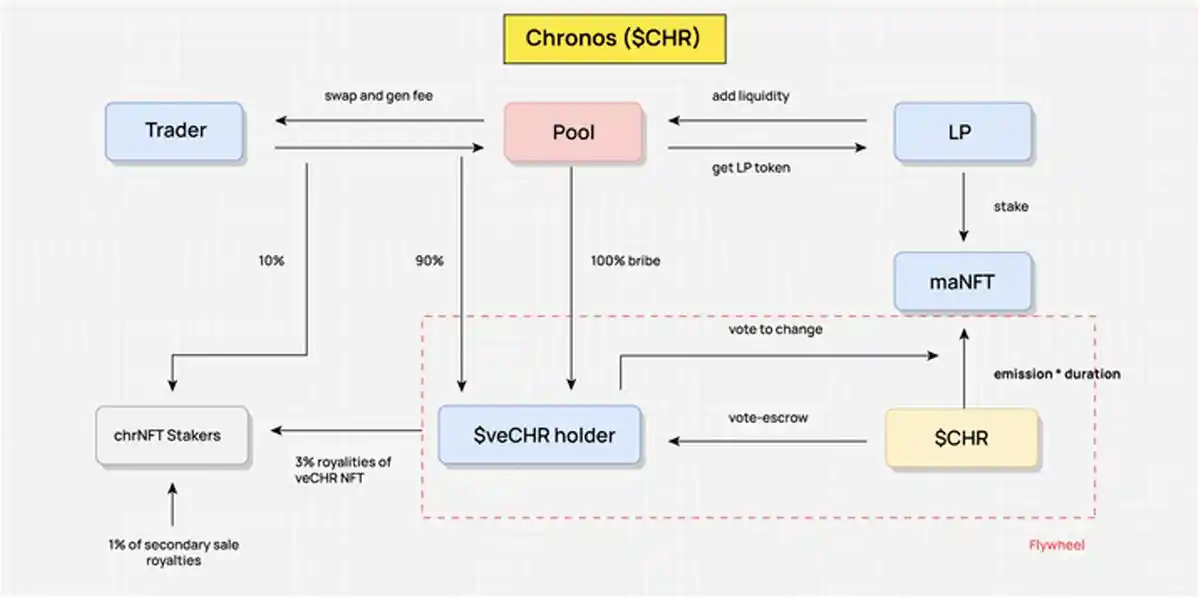

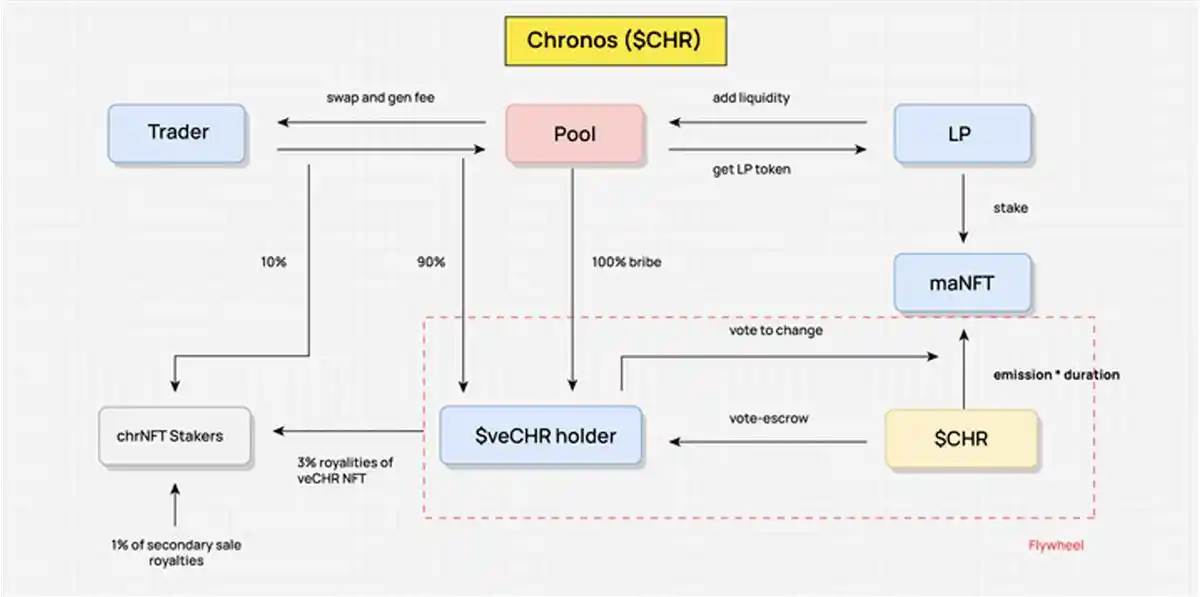

CHR Value Flow (ve(3,3) without rebase mechanism to prevent concentration of voting rights) diagram: DODO Research

Composition of Value Flow

DeFi protocols generate real income to varying degrees, with real money flowing within the protocol, thus generating value.

Value Flow abstracts the value flow of the protocol itself. First, starting from real income, it depicts the redistribution of the protocol's real income; secondly, it abstracts the flow and acquisition conditions of token incentives, allowing for a clear view of token value capture, incentive links, and token flow. These value flows constitute the entire business model, and the release of tokens will be redistributed through Value Flow as the protocol continues to operate.

Taking Chronos as an example, when abstracting its Value Flow, we first need to abstract key stakeholders, such as Traders, LPs, and veCHR holders. Key stakeholders are participants in the redistribution and nodes of value flow, with value flowing between these stakeholders and being redistributed according to the mechanism design.

The key to abstracting Value Flow lies in abstracting the direction and mechanism of income distribution; it does not require specificity for every link but rather integrates various small flow branches, abstracting and consolidating them when necessary to form a cohesive flow. For example, the source of real income is the transaction fees generated by Trader trades, with 90% of this portion allocated to veCHR holders through the ve mechanism for redistribution, thereby incentivizing the native token. Once Value Flow is abstracted, we can clearly see how value flows within the protocol and how income distribution evolves over time.

Value Flow is not the entirety of Tokenomics, but it is the product value flow based on Tokenomics design. When combined with factors such as the initial distribution and unlocking of tokens, it presents a complete picture of a protocol's Tokenomics.

Tokenomics Reshaping Value Flow

Why are early mining and withdrawal selling-type economic models becoming less visible?

In the early days, Tokenomics design was relatively crude, with tokens viewed as tools to incentivize users and short-term profit-making instruments. However, this incentive method was simple and direct, lacking effective redistribution mechanisms. Taking DEX as an example, when emissions and all transaction fees are directly allocated to LPs, there is a lack of long-term incentives for LPs. This model can easily collapse when the token price has no other sources of value, as the migration cost for LPs is too low, leading to the collapse of mining pools.

Over time, DeFi protocols have refined their Tokenomics designs, becoming increasingly sophisticated. To achieve incentive goals and regulate token supply and demand, various game mechanisms and income redistribution models have been introduced. Tokenomics is tightly coupled with the product logic and income distribution of the protocol itself. By reshaping Value Flow through Tokenomics, redistributing real income has become the primary function of Tokenomics, allowing for the regulation of token supply and demand and enabling tokens to achieve value capture.

Key Mechanisms of DeFi Tokenomics: Games and Value Redistribution

In the later stages of DeFi summer, many protocols have improved their economic models, essentially by introducing game mechanisms to redistribute a portion of profits, thereby strengthening user stickiness across the entire chain. Curve has reallocated token rewards through a mechanism of voting to redistribute emission rewards, even giving rise to bribery value and various combinatorial platforms. Additionally, another core aspect of Tokenomics is to drive the entire flywheel by introducing additional token rewards, capturing more traffic and funds.

In summary, under such mechanisms, tokens are no longer just a simple medium of value exchange; they also become tools for capturing users and creating value. This process of redistributing profits not only enhances user activity and stickiness but also stimulates user participation through token rewards, driving the overall development of the system.

Risk warning Risk warning

Risk warning Risk warning