DeFi Beginner's Guide (Part 1): How AAVE Whales Use 10 Million USD to Achieve 100% APR through Arbitrage

The author hopes to start a new series of articles to help friends quickly get started with DeFi, and to analyze the returns and risks of different strategies using the real data of DeFi whales. I hope everyone will support this. For the first issue, the author intends to begin with the recently popular interest rate arbitrage strategy and analyze the opportunities and risks of this strategy in conjunction with the capital allocation of AAVE whales.

The author hopes to start a new series of articles to help friends quickly get started with DeFi, and to analyze the returns and risks of different strategies using the real data of DeFi whales. I hope everyone will support this. For the first issue, the author intends to begin with the recently popular interest rate arbitrage strategy and analyze the opportunities and risks of this strategy in conjunction with the capital allocation of AAVE whales.Author: @Web3Mario

Abstract: Recently, with changes in the regulatory environment, DeFi protocols have achieved significantly higher interest rates than traditional financial wealth management scenarios, thanks to on-chain traders' enthusiasm for crypto assets. This has positive implications for two groups of users. Firstly, for some traders, after the prices of most blue-chip crypto assets break historical highs, appropriately reducing leverage and seeking low-alpha risk wealth management scenarios is a good choice. At the same time, as we enter a macro interest rate reduction cycle, many non-crypto office workers can also enjoy higher returns by allocating idle assets in DeFi. Therefore, the author hopes to start a new series of articles to help friends quickly get started with DeFi, and analyze the returns and risks of different strategies based on the real trading data of DeFi whales. I hope everyone supports this. In the first issue, the author wishes to start with the recently popular interest rate arbitrage strategy and analyze the opportunity points and risks of this strategy in conjunction with the capital allocation of AAVE whales.

What is Interest Rate Arbitrage in the DeFi World?

First, let’s introduce what interest rate arbitrage is for those unfamiliar with finance. Interest Rate Arbitrage, also known as Carry Trade, is a financial arbitrage strategy that aims to profit from the interest rate differences between different markets, currencies, or debt instruments. In simple terms, this business follows a path: borrow at low interest, invest at high interest, and earn the interest spread. In other words, arbitrageurs borrow low-cost funds and then invest in higher-yielding assets to earn the spread profit.

Taking the most favored strategy by hedge funds in the traditional financial market as an example, that is the USD/JPY Carry Trade. We know that Japan has maintained extremely low bond yields under the YCC policy, with real interest rates even at negative levels. Meanwhile, the USD remains in a high-interest environment, creating a spread between the two different financing markets. Hedge funds choose to use high-yielding US Treasury bonds as collateral to borrow Japanese yen from various financing channels, and then either purchase high-dividend assets from Japan's five major trading companies or exchange back to USD to buy other high-return assets (PS: one of Buffett's favorite strategies). The advantage of this strategy is that it can increase the efficiency of capital leverage. Just this arbitrage path can scale enough to influence global risk asset prices, which is why every rate hike after the Bank of Japan abandoned YCC in the past year has greatly impacted risk asset prices.

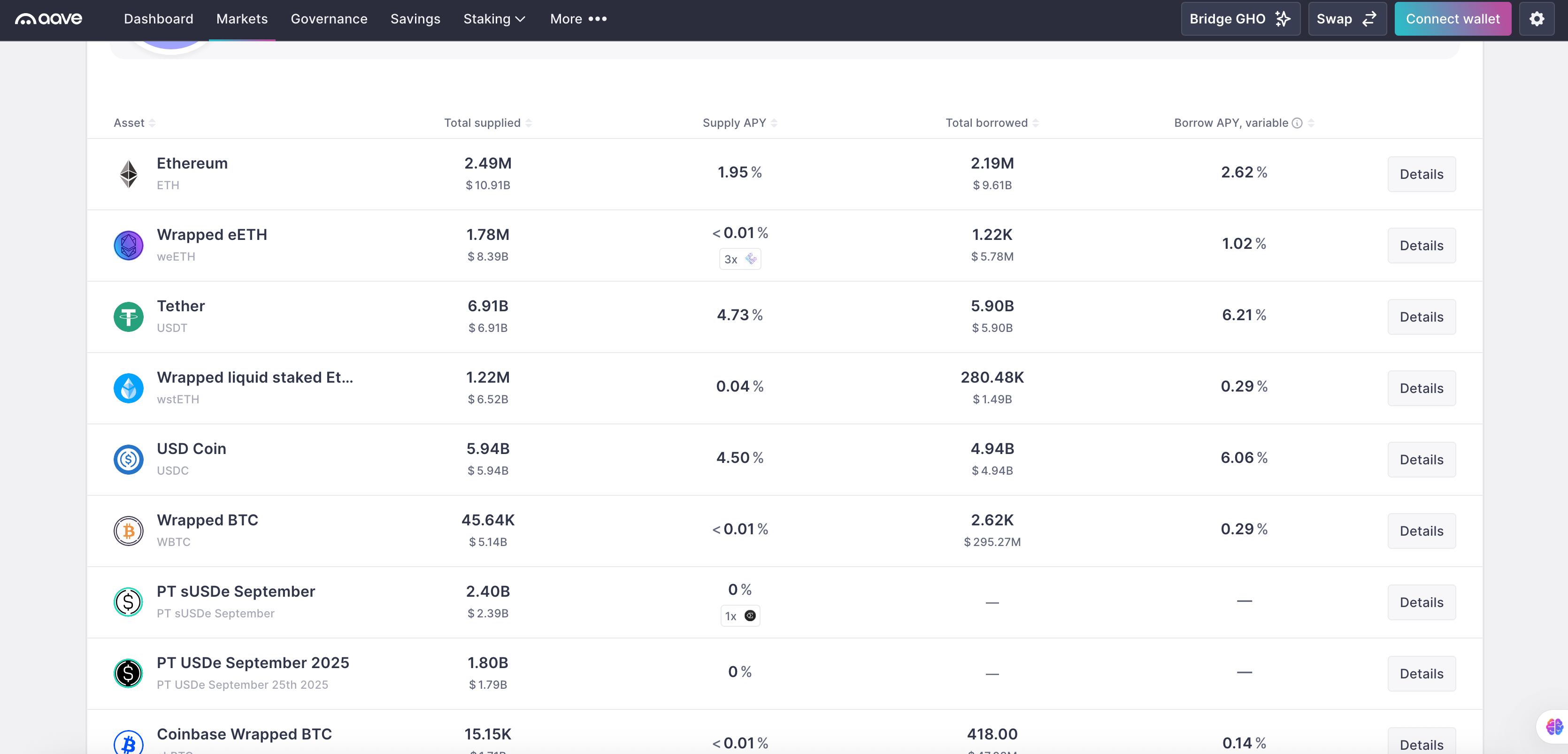

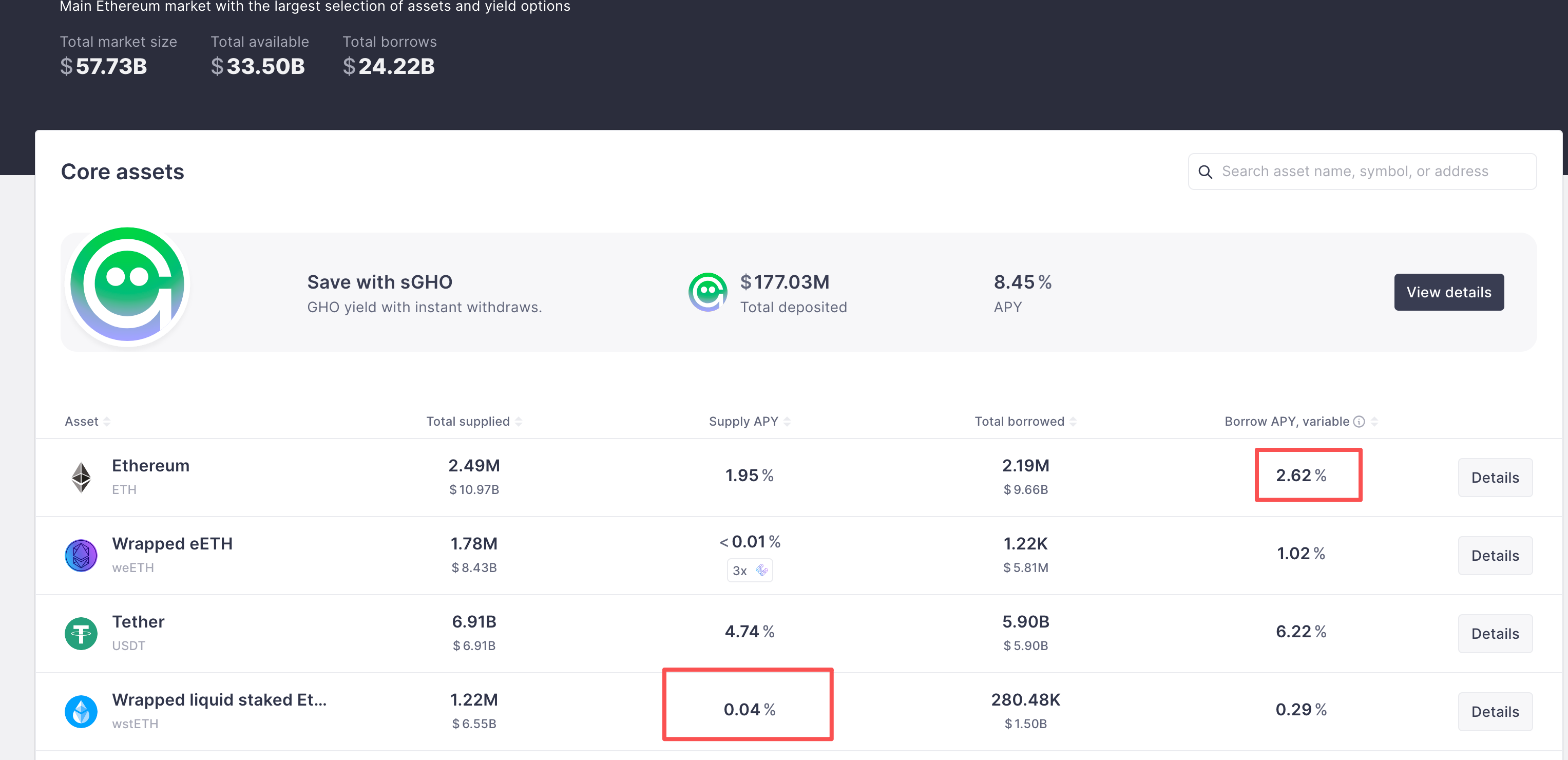

In the DeFi world, the two core innovations fall into two major categories: the first is decentralized exchanges (DEX), and the second is decentralized lending protocols (Lending). The former guides "price difference arbitrage strategies," which we will not discuss in this article, while the latter is the main source of "interest rate arbitrage strategies." Decentralized lending protocols allow users to borrow one type of crypto asset using another type as collateral. The specific subdivisions will vary based on liquidation mechanisms, collateral ratio requirements, and interest rate determination methods. However, we will focus on the currently most mainstream "over-collateralized lending protocols" to introduce this strategy. Taking AAVE as an example, you can use any supported crypto asset as collateral to borrow another crypto asset. In this process, your collateral still enjoys native yields and the platform's lending yields, represented by the Supply APY. This is because most lending protocols adopt a Peer To Pool model, where your collateral automatically enters a unified liquidity pool, serving as the source of lending funds for the platform. Therefore, borrowers who need your collateral type will pay interest to this liquidity pool, which is the source of lending income. What you need to pay is the borrowing interest corresponding to the asset you borrowed, represented by the Borrow APY.

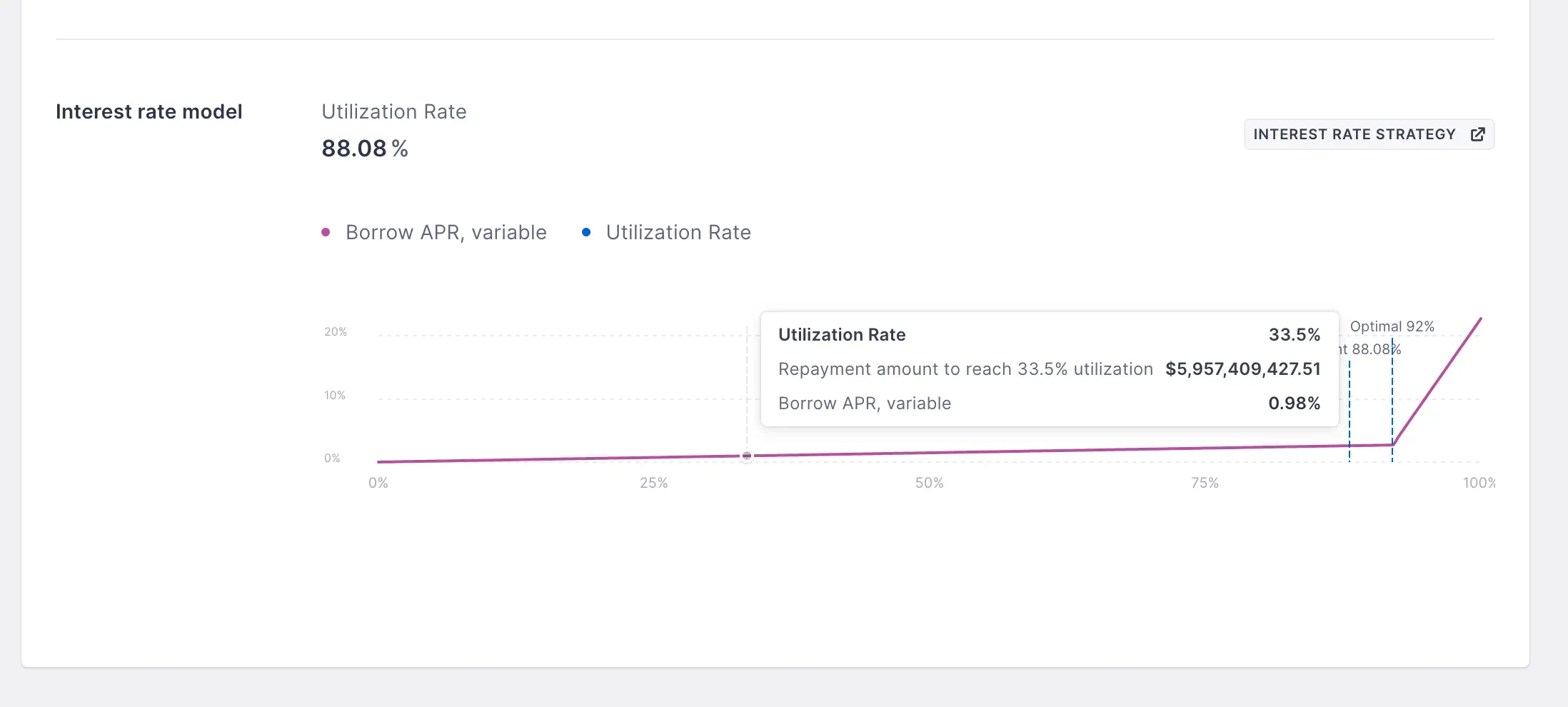

These two interest rates are variable and are determined by the interest rate curve in AAVE. In simple terms, the higher the utilization rate of the liquidity pool, the higher the corresponding interest rate level. The reason for this design is that in Peer To Pool lending protocols, borrowing does not have the concept of a maturity date like in traditional financial markets. This simplifies the complexity of the protocol and allows for higher liquidity for lenders, as they do not need to wait until the debt matures to retrieve their principal. However, to ensure sufficient constraints on borrowers' repayments, the protocol requires that once the remaining liquidity in the pool decreases, the borrowing interest rate increases, compelling borrowers to repay and ensuring that the remaining liquidity in the pool remains in a dynamic balance, reflecting the true market demand as much as possible.

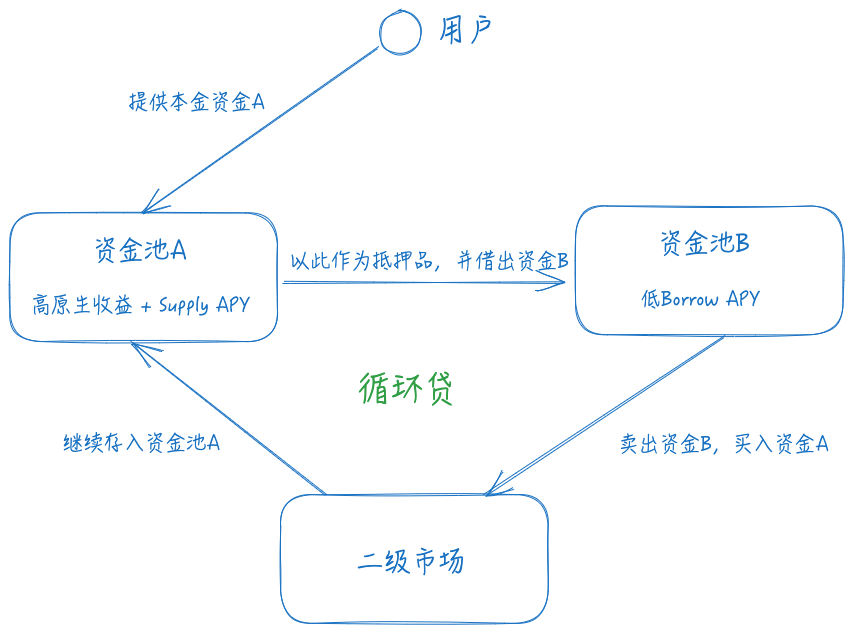

After understanding these basics, let's introduce how interest rate arbitrage is achieved. First, you need to find native asset yields + high Supply APY assets as collateral. Next, find a suitable borrowing path with low Borrow APY to lend out assets. Finally, use the borrowed funds to repurchase collateral in the secondary market and repeat the above operations to increase capital leverage.

Those with financial knowledge can easily identify two risks in this path:

l Exchange Rate Risk: If asset A depreciates relative to asset B, it can easily lead to liquidation risk. For example, if your collateral is ETH and the borrowed funds are USDT, when the price of ETH falls, your collateral ratio may become insufficient, leading to liquidation.

l Interest Rate Risk: If the Borrow APY of liquidity pool B exceeds the total yield of liquidity pool A, the strategy is in a loss state.

l Liquidity Risk: The exchange liquidity of assets A and B determines the establishment and exit costs of this arbitrage strategy. If liquidity decreases significantly, the impact can still be considerable.

To mitigate exchange rate risk, we see that most DeFi interest rate arbitrage designs require the two types of funds to have a certain correlation in price, avoiding large deviations. Therefore, the main asset choices in this space are two: LSD paths and Yield Bearing Stablecoin paths. The difference depends on what the managed funds are based on. If it is based on risk assets, besides interest rate arbitrage, it can still retain the ability to earn native asset alpha returns, such as using Lido's stETH as collateral to borrow ETH. This arbitrage path was very popular during the LSDFi Summer period. Additionally, choosing correlated assets has the benefit of allowing for higher maximum leverage, as AAVE sets a higher Max LTV for correlated assets, known as E-Mode. With a setting of 93%, the theoretical maximum leverage is 14 times. Therefore, based on the current yield rates, taking AAVE as an example, the lending yield rate for wsthETH is 2.7% (ETH native yield) + 0.04% (Supply APY), while the Borrow APY for ETH is 2.62%. This means there is a 0.12% interest rate spread, and the potential yield of this strategy is 2.74% + 13 * 0.12% = 4.3%.

For interest rate risk and liquidity risk, they can only be mitigated through continuous monitoring of bilateral interest rates and related liquidity. Fortunately, this risk does not involve immediate liquidation, so timely liquidation is sufficient.

How AAVE Whales Earn 100% APR Through Interest Rate Arbitrage with $10 Million

Next, let's take a look at how DeFi whales utilize interest rate arbitrage to achieve excess returns. In previous articles, it was mentioned that AAVE accepted PT-USDe issued by Pendle as collateral a few months ago. This has completely stimulated the profitability of interest rate arbitrage. We can find that PT-USDe has always been in a supply cap state on the AAVE official site, indicating the popularity of this strategy.

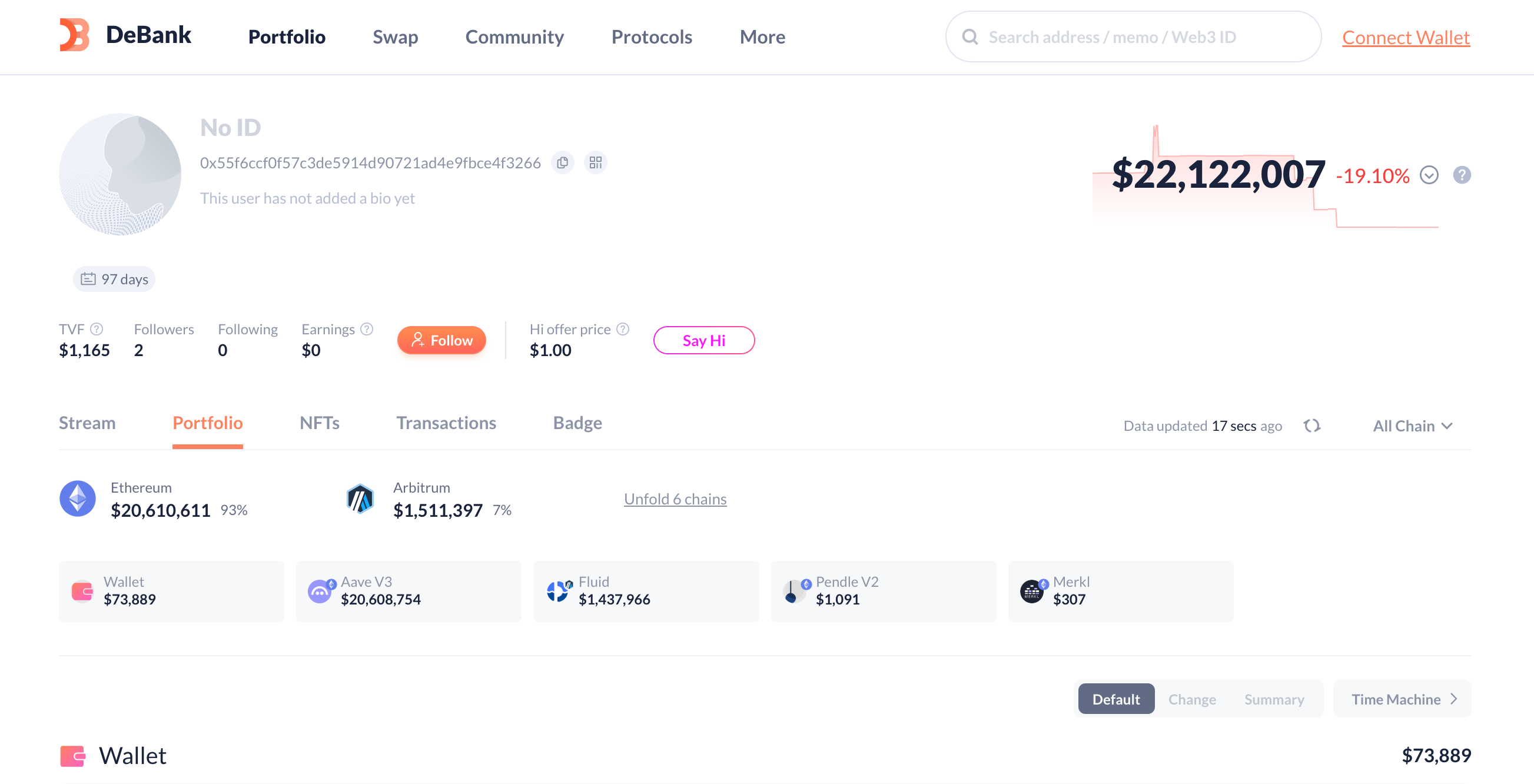

We choose the largest DeFi whale in terms of collateral size in this market, 0x55F6CCf0f57C3De5914d90721AD4E9FBcE4f3266, to analyze its capital allocation and potential yield. This account has a total asset size of $22M, but most of it is used to allocate the aforementioned strategy.

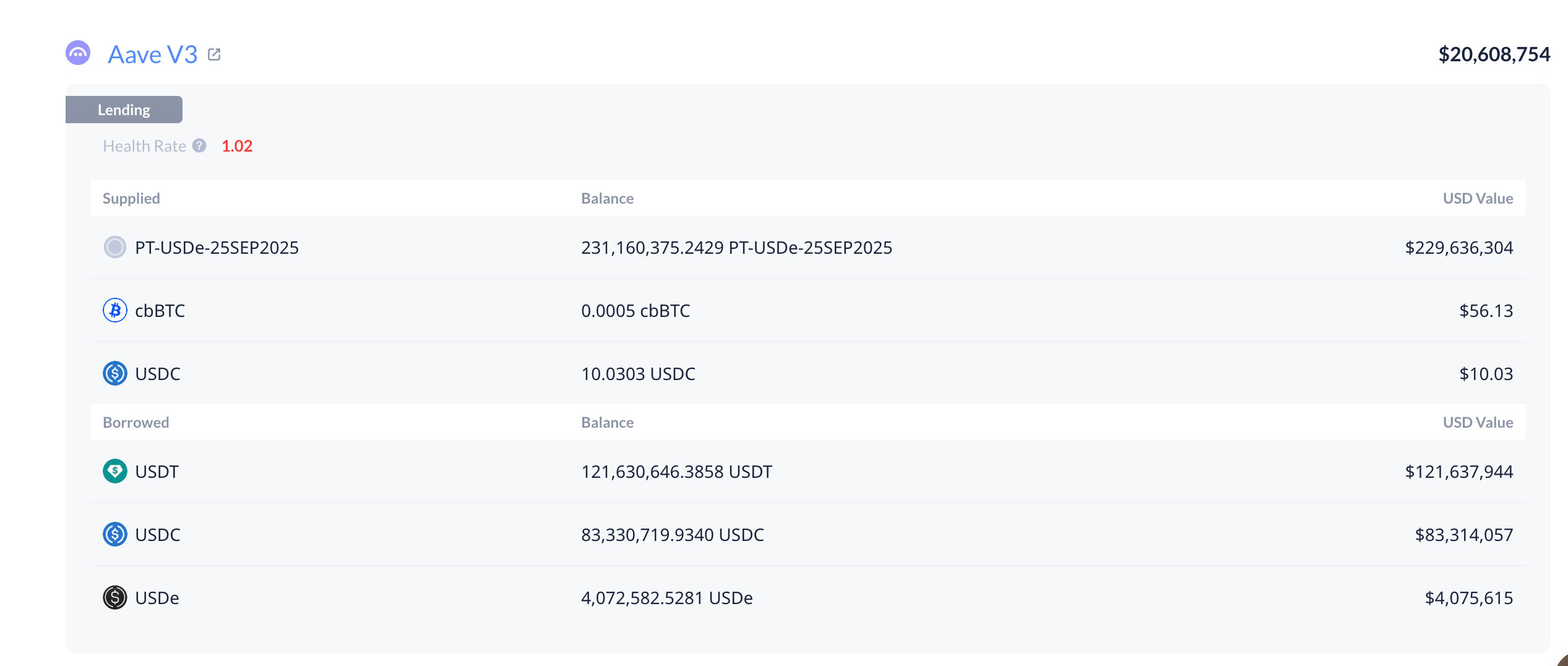

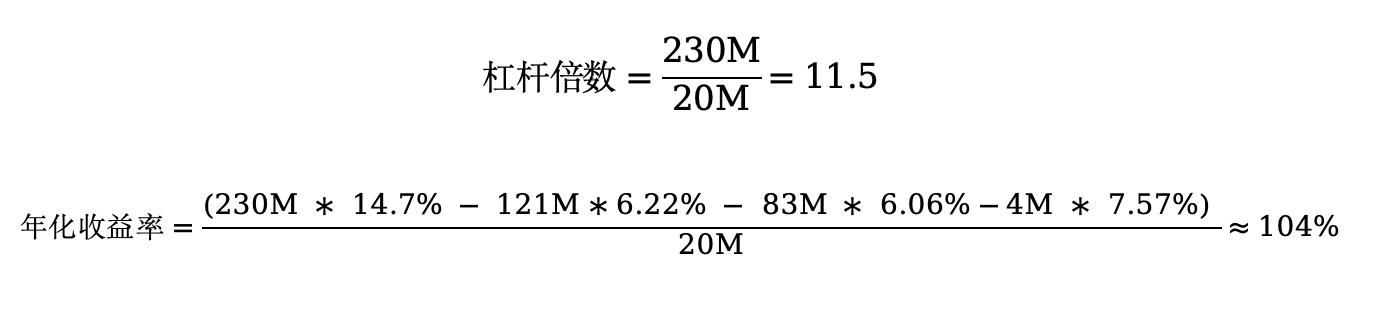

It can be seen that this account has allocated funds through two lending markets, with $20.6M allocated in the AAVE ecosystem and $1.4M allocated in Fluid. As shown in the figure, this account has leveraged approximately $230M of PT-USDe assets using $20M of principal in AAVE, with the corresponding borrowing distribution being $121M USDT, $83M USDC, and $4M USDe. Next, let's calculate its APR and leverage ratio.

Based on the PT-USDe interest rate at the time of its position establishment, the main locking interest rate occurred on August 15 at 20:24, which means the account's position establishment interest rate was 14.7%.

Currently, the borrowing interest rates in AAVE are 6.22% for USDT, 6.06% for USDC, and 7.57% for USDe. We can calculate its leverage ratio and total yield to be 11.5 times and 104%. What attractive numbers!

How DeFi Newbies Can Replicate Big Players' Strategies

In fact, for DeFi newbies, replicating such interest rate arbitrage strategies is not difficult. There are already many automated interest rate arbitrage protocols in the market that can help ordinary users avoid the complex logic of circular loans and open positions with one click. Here, since the author is standing from the buyer's market perspective, specific project names will not be introduced; everyone can collect them in the market.

However, the author needs to remind you of the risks of this strategy, which mainly fall into three aspects:

Exchange Rate Risk: In previous articles, the design logic of AAVE's official community regarding PT asset Oracles has been introduced. Simply put, when the oracle is upgraded to capture changes in PT assets in the secondary market, this strategy needs to control the leverage ratio to avoid liquidation risks when the maturity date is far away and market prices fluctuate significantly.

Interest Rate Risk: Users need to continuously monitor changes in interest rate spreads and adjust positions when the spread converges or even turns negative to avoid losses.

Liquidity Risk: This mainly depends on the fundamentals of the target yield-bearing asset project. If a major trust crisis occurs, liquidity will quickly dry up, and the slippage losses incurred when exiting the strategy will be significant. Users should also maintain a certain level of vigilance and keep an eye on project developments.

Risk warning

Risk warning Risk warning

Risk warning