Tiger Research Bitcoin Valuation Report: Q4 Target Price $200,000

Short-term pullbacks may stem from signs of overheating, but this is part of a healthy consolidation rather than a shift in trend or market perception.

Short-term pullbacks may stem from signs of overheating, but this is part of a healthy consolidation rather than a shift in trend or market perception.This report is authored by Tiger Research, which proposes a target price of $200,000 for Bitcoin in the fourth quarter of 2025 based on factors such as institutional buying during volatility, the Federal Reserve's interest rate cuts, and the confirmation of an institutionally dominated market pattern following the October crash.

Key Points

Institutional investors continue to accumulate during volatility ------ Net inflows into ETFs remained stable in the third quarter, with MSTR increasing its holdings by 388 Bitcoins in a single month, reinforcing long-term investment beliefs;

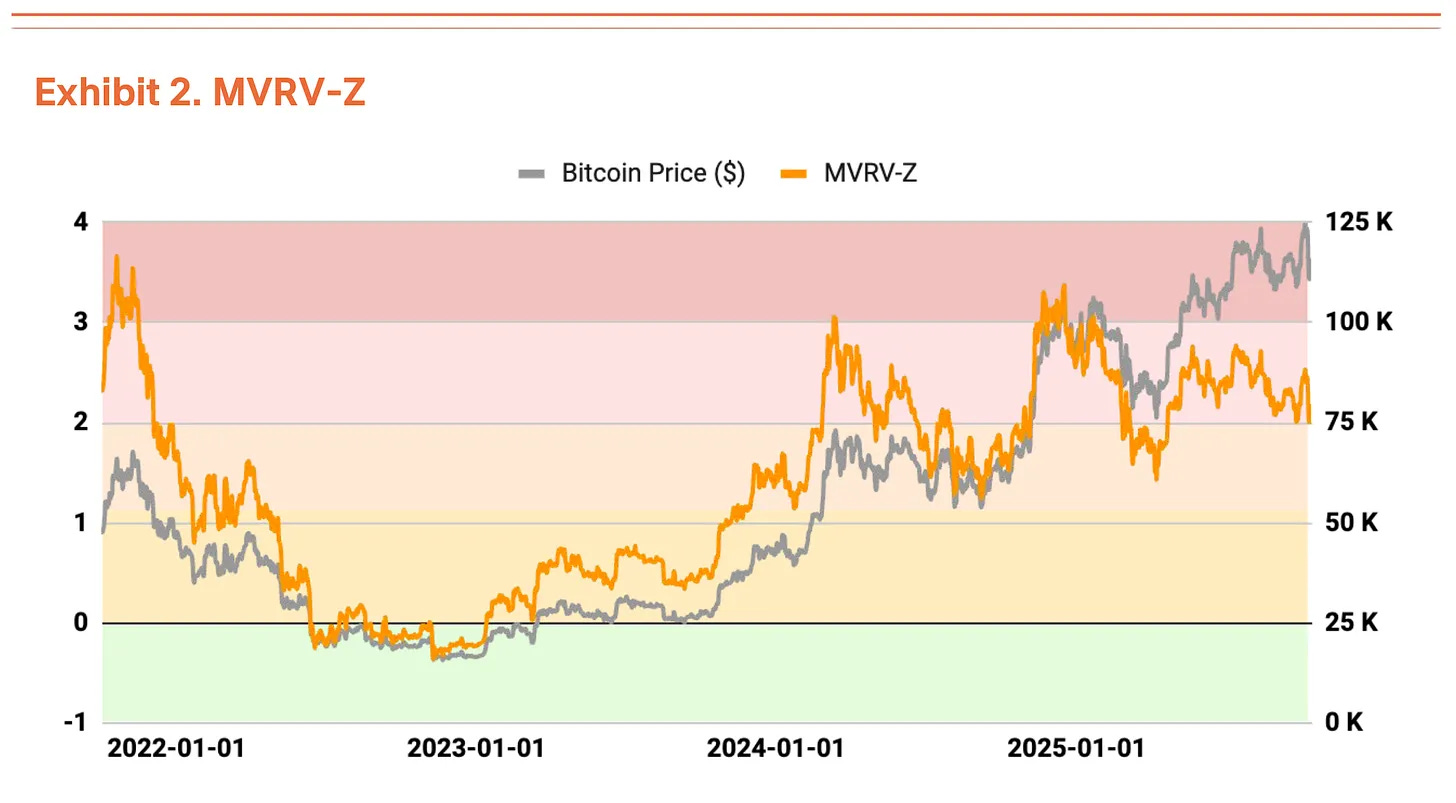

Overheated but not extreme ------ The MVRV-Z index is at 2.31, indicating that valuations are high but not at extreme levels. The clearing of leveraged funds has eliminated short-term traders, creating space for the next wave of increases;

Global liquidity environment continues to improve ------ The broad money supply (M2) has surpassed $96 trillion, reaching a historic high, and expectations for interest rate cuts by the Federal Reserve have increased, with 1-2 more cuts anticipated within the year.

Institutional Investors Buy Amid U.S.-China Trade Uncertainty

In the third quarter of 2025, the Bitcoin market slowed from a strong growth of 28% in the second quarter to a volatile sideways phase (1% growth).

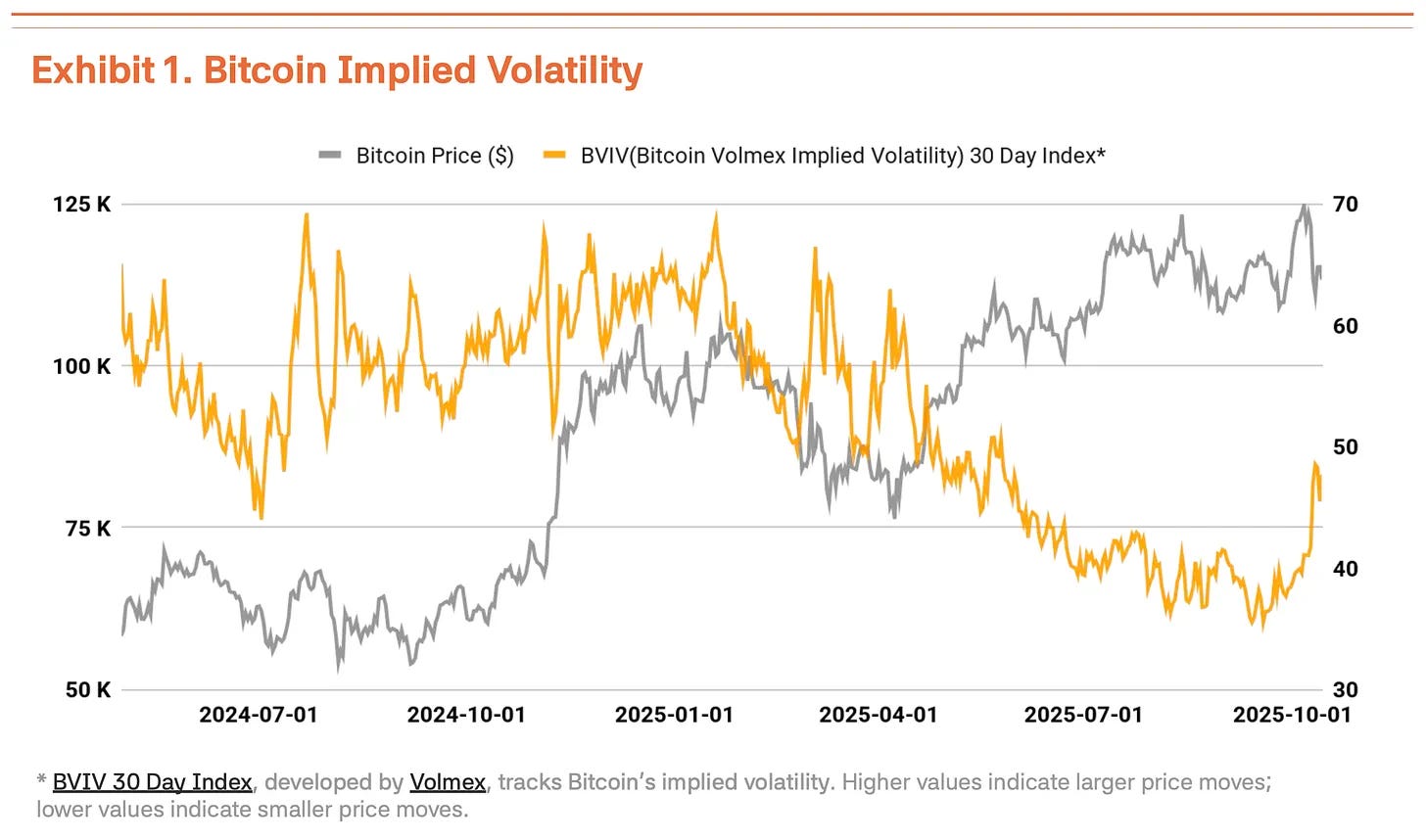

On October 6, Bitcoin reached an all-time high of $126,210, but the Trump administration once again exerted trade pressure on China, causing Bitcoin's price to pull back 18% to $104,000, significantly increasing volatility. According to Volmex Finance’s Bitcoin Volatility Index (BVIV), Bitcoin's volatility narrowed from March to September as institutional investors steadily accumulated, but soared 41% after September, exacerbating market uncertainty (Chart 1).

Driven by the resurgence of U.S.-China trade frictions and Trump's tough rhetoric, this pullback appears temporary. The strategic accumulation led by Strategy Inc. (MSTR) is actually accelerating. The macro environment has also played a supportive role. The global broad money supply (M2) has surpassed $96 trillion, reaching a historic high, while the Federal Reserve lowered interest rates by 25 basis points to 4.00%-4.25% on September 17. The Fed hinted at 1-2 more rate cuts this year, with a stable labor market and economic recovery creating favorable conditions for risk assets.

Institutional capital inflows remain strong. In the third quarter, net inflows into Bitcoin spot ETFs reached $7.8 billion. Although this is lower than the $12.4 billion in the second quarter, the net inflow throughout the third quarter confirms the stable buying by institutional investors. This momentum continued into the fourth quarter—recording $3.2 billion in just the first week of October, setting a new weekly inflow record for 2025. This indicates that institutional investors view price pullbacks as strategic entry opportunities. Strategy continued to buy during the market pullback, purchasing 220 Bitcoins on October 13 and 168 Bitcoins on October 20, totaling 388 Bitcoins in one week. This shows that regardless of short-term volatility, institutional investors firmly believe in Bitcoin's long-term value.

On-chain Data Signals Overheating, Fundamentals Unchanged

On-chain analysis reveals some signs of overheating, but valuations are not yet concerning. The MVRV-Z metric (market cap to realized value ratio) is currently in the overheated zone at 2.31, but has stabilized compared to the extreme valuation range approached in July-August (Chart 2).

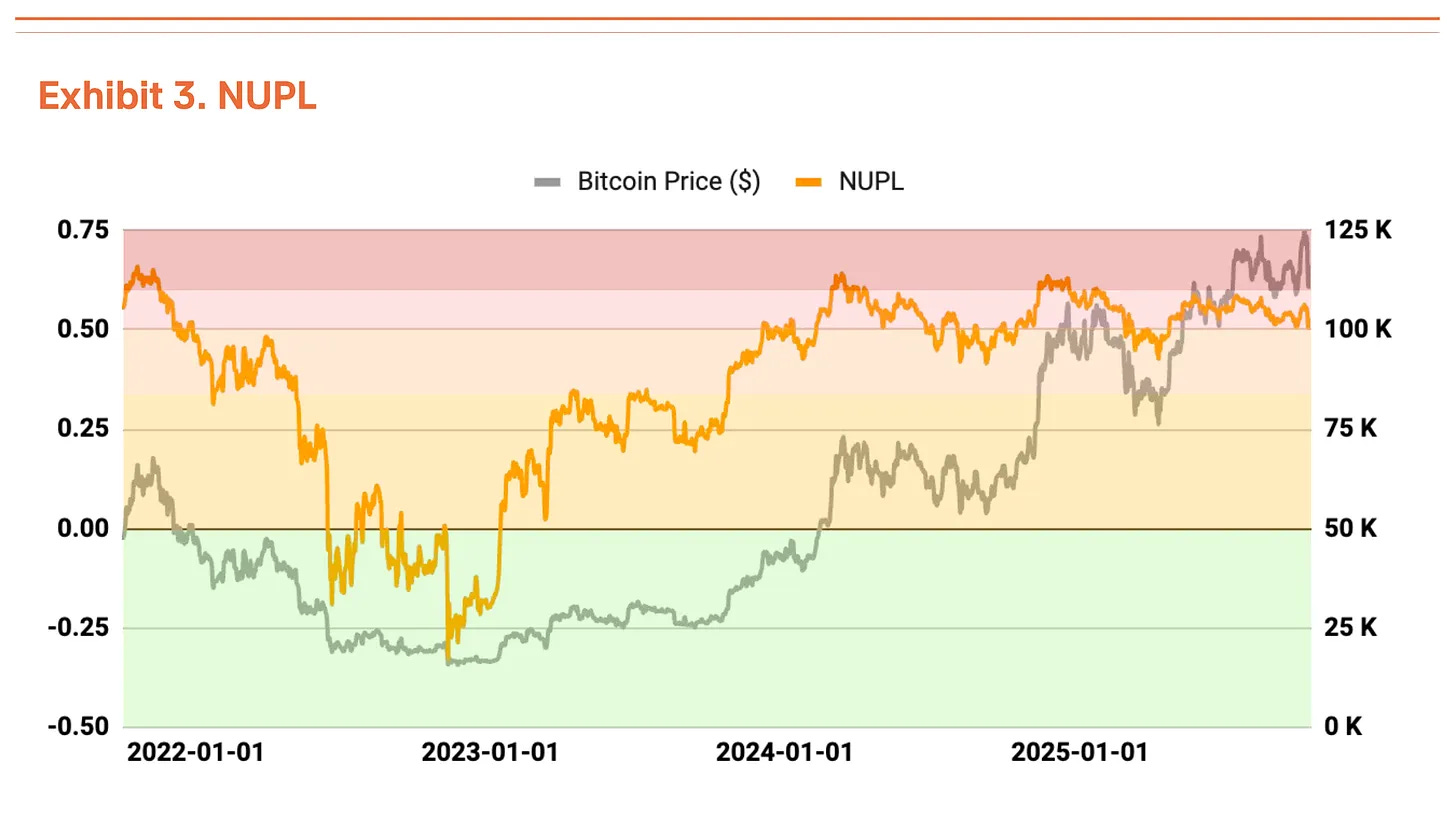

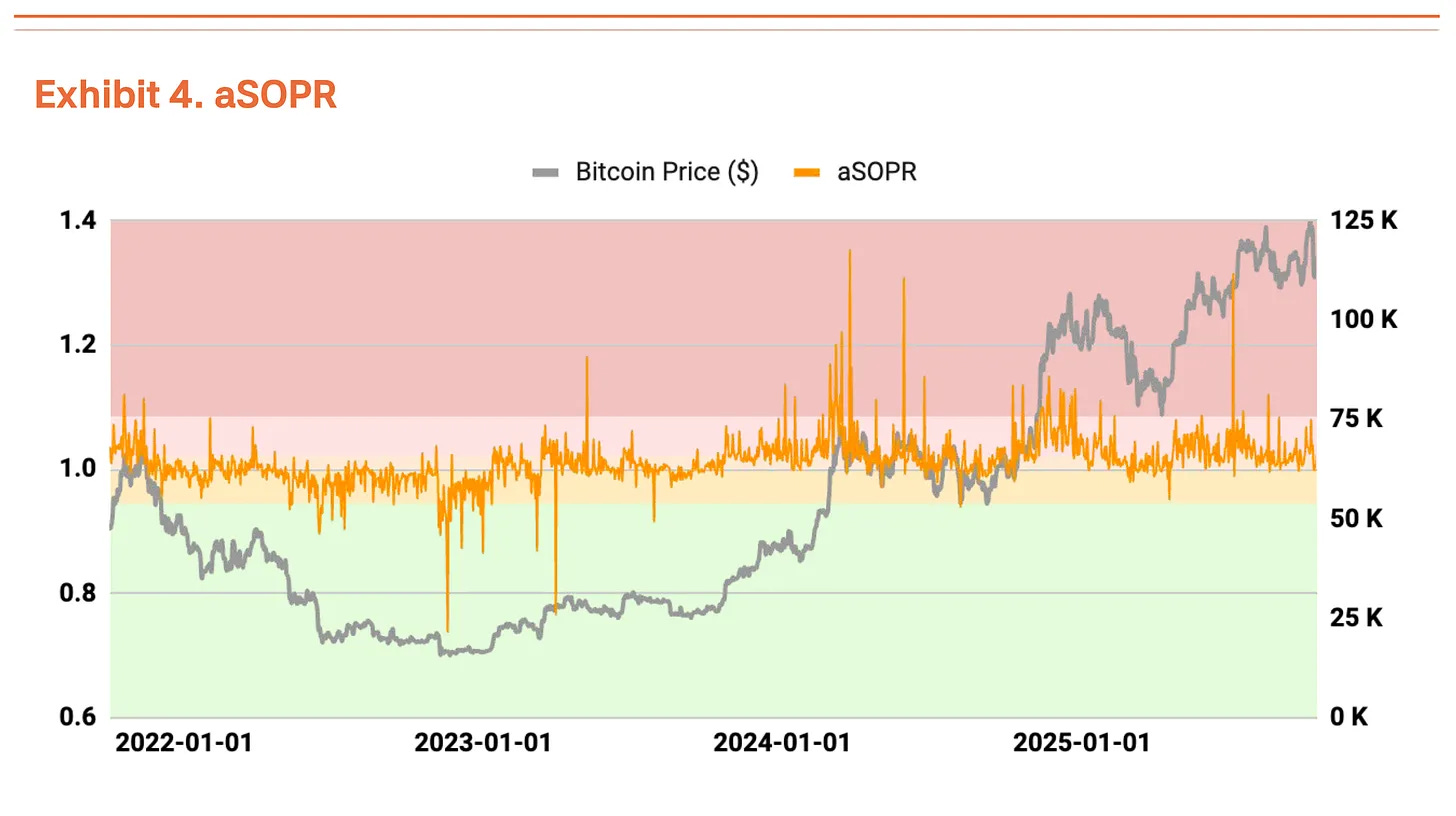

The Net Unrealized Profit and Loss (NUPL) also shows signs of overheating, but has eased from the high unrealized profit situation in the second quarter (Chart 3). The Adjusted Spent Output Profit Ratio (aSOPR) reflects the realized profit and loss of investors, and this ratio is very close to the equilibrium value of 1.03, indicating no cause for concern (Chart 4).

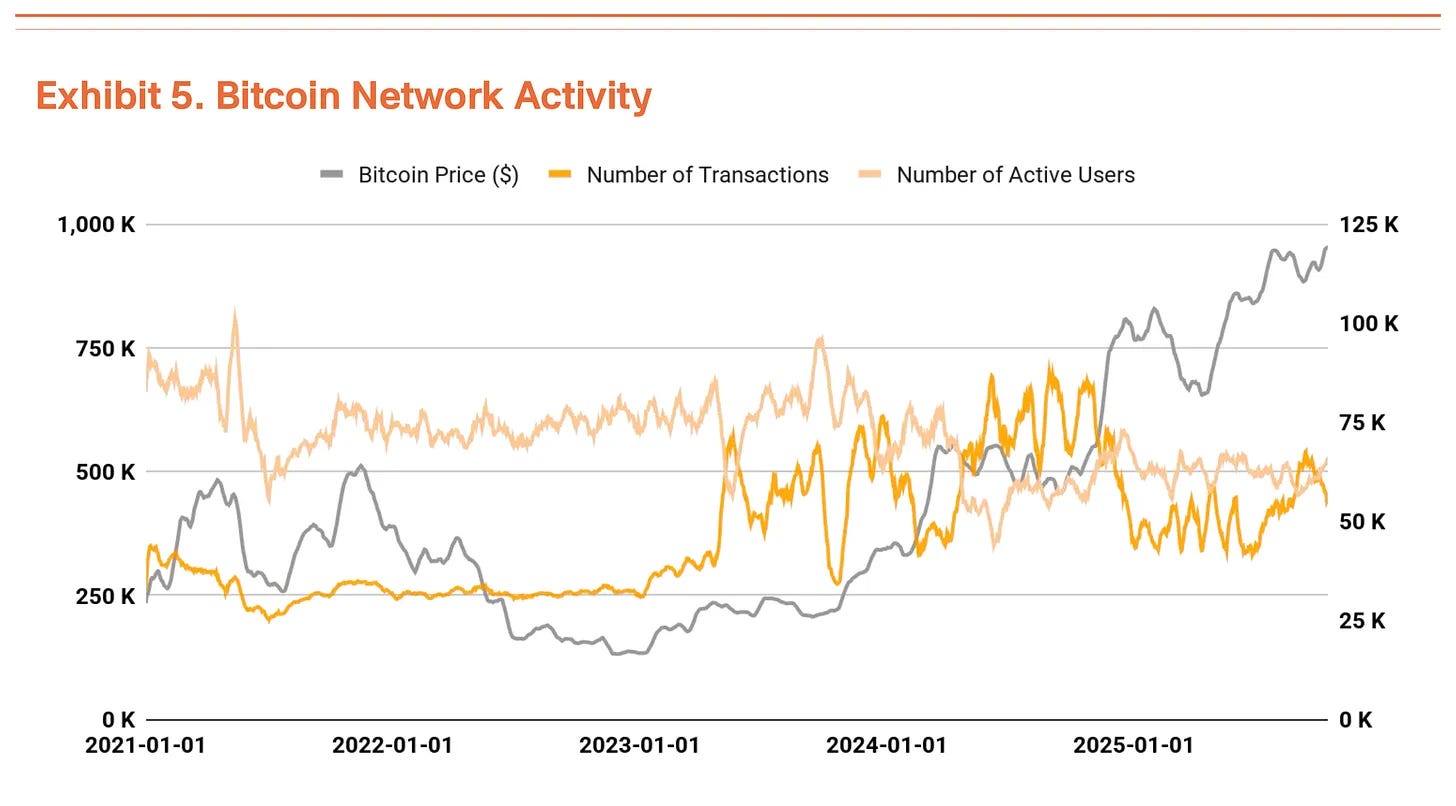

The number of Bitcoin transactions and active users remains at similar levels to the previous quarter, indicating a temporary slowdown in network growth (Chart 5). Meanwhile, total transaction volume is on the rise. A decrease in transaction count but an increase in transaction volume means larger amounts are being transferred in fewer transactions, indicating an increase in large capital flows.

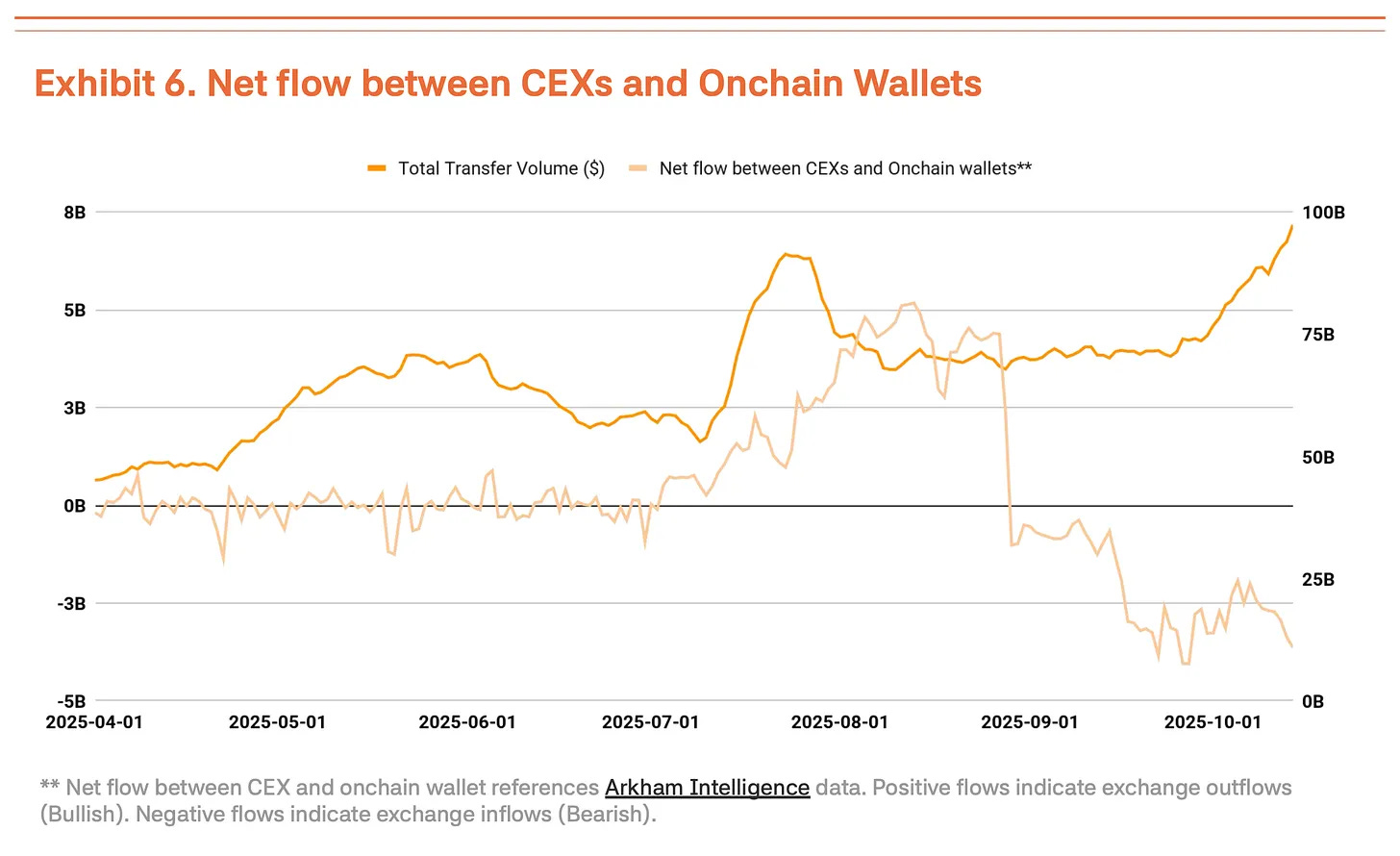

However, we cannot simply view the increase in transaction volume as a positive signal. Recently, there has been an increase in funds flowing into centralized exchanges, which typically indicates that holders are preparing to sell (Chart 6). In the absence of improvements in fundamental indicators such as transaction count and active users, the rise in transaction volume more reflects the flow of short-term capital and selling pressure in a high-volatility environment, rather than a genuine expansion of demand.

October 11 Crash Proves Market Has Shifted to Institutional Dominance

The crash on centralized exchanges on October 11 (down 14%) proves that the Bitcoin market has shifted from retail dominance to institutional dominance.

The key point is that the market's reaction is markedly different from before. In a similar environment at the end of 2021, panic among retail-dominated markets spread, leading to a crash. This time, the pullback was limited. After massive liquidations, institutional investors continued to buy, indicating that they are firmly defending the market's downside. Furthermore, institutions seem to view this as a healthy consolidation, helping to eliminate excessive speculative demand.

In the short term, the chain reaction of selling may lower the average purchase price for retail investors and increase psychological pressure, potentially exacerbating volatility due to frustrated market sentiment. However, if institutional investors continue to enter during the sideways consolidation, this pullback may lay the groundwork for the next round of increases.

Target Price Raised to $200,000

Using our TVM method for third-quarter analysis, we derive a neutral benchmark price of $154,000, a 14% increase from the $135,000 in the second quarter. Based on this, we applied a -2% fundamental adjustment and a +35% macro adjustment, resulting in a target price of $200,000.

The -2% fundamental adjustment reflects a temporary slowdown in network activity and an increase in deposits to centralized exchanges, indicating short-term weakness. The macro adjustment remains at 35%. The global liquidity expansion and continued institutional capital inflows, along with the Federal Reserve's stance on interest rate cuts, provide a strong catalyst for increases in the fourth quarter.

Short-term pullbacks may stem from signs of overheating, but this represents a healthy consolidation rather than a trend or shift in market perception. The continuous rise in benchmark prices indicates that Bitcoin's intrinsic value is steadily increasing. Despite temporary weakness, the medium to long-term upward outlook remains solid.

Risk warning Risk warning

Risk warning Risk warning