Tron Industry Weekly Report: High interest rate expectations continue, BTC/ETH show fluctuating divergence, PAYY and Midas financing reflect the warming of on-chain payment and yield infrastructure

FirstMark led the investment in PAYY, with DBA and Ventures participating, as well as Midas, which was led by RRE Ventures and Creandum, with participation from Coinbase, GSR, Oasis, and Framework.

FirstMark led the investment in PAYY, with DBA and Ventures participating, as well as Midas, which was led by RRE Ventures and Creandum, with participation from Coinbase, GSR, Oasis, and Framework.I. Outlook

1. Macroeconomic Summary and Future Predictions

From May 4 to 11, the macroeconomic theme can be summarized as "growth remains stable, inflation persists, and policy is relatively tight." The U.S. Federal Reserve maintained interest rates at the end of April and emphasized inflation pressures with a more hawkish tone, particularly regarding the spillover risks from rising energy prices. Meanwhile, the non-farm payroll data for April, released on May 8, exceeded expectations, and the unemployment rate remained stable at 4.3%, indicating that the labor market still has resilience, but it also pushed market expectations for short-term interest rate cuts further out. Coupled with U.S.-China tariff and trade frictions, as well as the situation in the Middle East driving up oil prices, market sentiment has been oscillating between "no economic recession" and "inflation is difficult to decline quickly."

In the coming week, macro trading may still be characterized by "high rates maintained for longer," with risk appetite continuing to be highly sensitive to inflation, oil prices, and trade news. If subsequent U.S. inflation data continues to be hot, the market will further reinforce the pricing of "limited room for interest rate cuts this year." Conversely, if inflation shows signs of cooling, the dollar and long-term rates may have significant room to decline. Overall, economic data is likely to continue supporting the growth narrative, but uncertainties in policy and geopolitics will suppress valuation expansion, with equity markets more likely to exhibit high-level fluctuations and sector rotations rather than a unilateral upward trend.

2. Market Changes and Warnings in the Crypto Industry

From May 4 to 11, the overall crypto market remained in a "high volatility, oscillating" structure. In terms of price, Bitcoin fluctuated around the $80,000 to $82,000 range, currently at about $81,300, indicating that while bulls have not lost key support, selling pressure above is also quite evident. Ethereum is weaker, currently around $2,310, with intraday highs and lows roughly between $2,300 and $2,344, reflecting that the recovery of altcoins is still lagging behind BTC. Overall, funds are leaning towards mainstream coins with better liquidity, as the market continues to digest macro interest rate expectations, changes in risk appetite, and the tug-of-war between mid-to-long-term narratives post-halving and short-term profit-taking pressures.

In the coming week, the market's directional warning remains "first watch if BTC can hold around $80,000, then see if it can effectively break above the $82,000 upper limit." If BTC falls below $80,000 and does so with volume, altcoins usually accelerate their declines; if it can stabilize above $81,000 and initiate an effective breakthrough towards $82,000 to $83,000, short-term sentiment will improve significantly, but it is more likely to first manifest as a structural rebound rather than a broad-based rally. The key observation point for ETH can initially be set at $2,300; if it falls below this level, weakness will continue, while if it can stabilize above $2,350, it may drive some high-beta altcoins to recover.

3. Industry and Sector Hotspots

FirstMark led the investment in PAYY, with DBA and Ventures participating, while Midas was led by RRE Ventures and Creandum, with Coinbase, GSR, Oasis, and Framework also participating. These represent two clear main lines in crypto infrastructure: the former focuses on creating a low-cost, high-efficiency on-chain payment network, while the latter aims to connect off-chain government bond yields with on-chain liquidity. Both indicate that the current market focus is gradually shifting from pure trading and speculation to more fundamental aspects of payment efficiency, capital turnover, and yield distribution capabilities.

II. Market Hotspot Sectors and Potential Projects for the Week

1. Overview of Potential Projects

1.1. Analysis of PAYY, led by FirstMark, with DBA and Ventures participating—building low-cost, high-efficiency on-chain payment infrastructure

Introduction

Payy is a privacy-centric stablecoin platform that achieves default private transactions through zero-knowledge technology (ZK). It provides self-custody wallets and Visa cards, allowing users to seamlessly use USDC for payments while maintaining the privacy of on-chain activities.

Payy is also building the Payy Network, a layer-2 Rollup based on Ethereum that hides transaction data through zero-knowledge proofs, including sender, receiver, and transaction amount.

Currently, Payy has launched its wallet product, the network is about to go live, and it plans to issue tokens, aiming to promote the mainstream application of privacy stablecoin payments.

Protocol Framework Overview

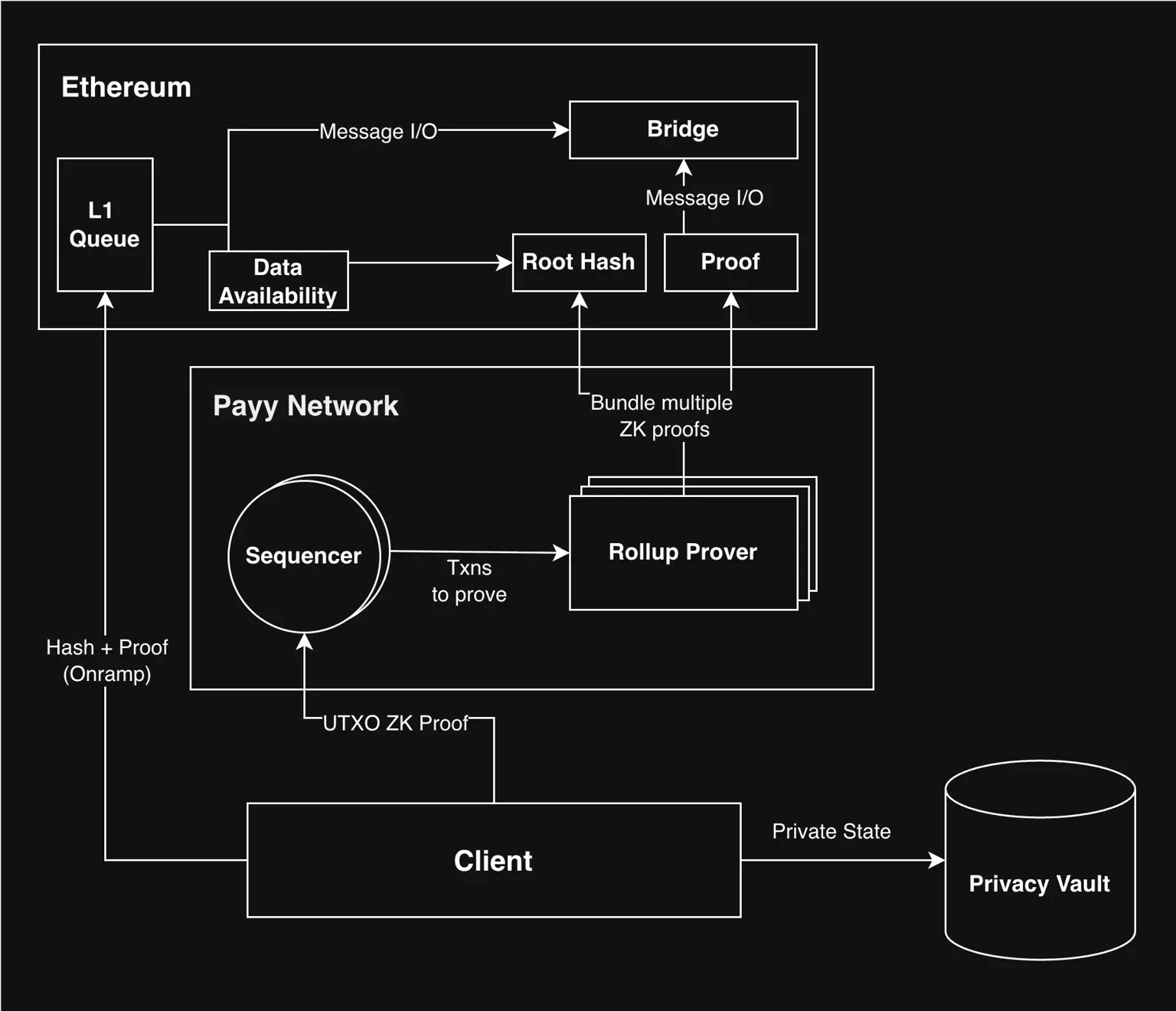

- Payy Network Architecture

Payy Network is a layer-2 zero-knowledge Rollup based on Ethereum, with the following roles in its architecture:

- Sequencer: submits blocks to L1 for verification and ensures the determinism of transaction order.

- Rollup Prover: provides validity proofs for sorted blocks, verifying their correctness or errors.

- Client: responsible for generating valid UTXO transaction proofs.

- Encrypted Registries (optional): used to store transaction data, allowing users to participate in transactions even while offline.

- Ethereum: provides security and data availability for the entire network.

Core Logic: Achieves privacy protection and efficient scaling on the secure foundation of Ethereum through ZK proofs + Rollup architecture.

- Privacy Architecture

Payy achieves privacy protection through zero-knowledge proofs (ZK) while maintaining compatibility with EVM. Its privacy system includes three core mechanisms:

- Private Transfers: supports fully private transfers of ERC-20 and native tokens.

- Stealth Transactions: achieves anonymous transactions at the EVM layer through one-time addresses.

- Native ZK: provides low-cost ZK verification capabilities, supporting custom privacy applications.

Core Architecture Components

- Privacy Layer: high-performance privacy Rollup, creating independent privacy pools for each ERC-20.

- PrivacyBridge: a bridging component connecting the EVM layer with the privacy layer.

- Privacy Vault: stores private data and converts regular transactions into private transactions through ZK proofs.

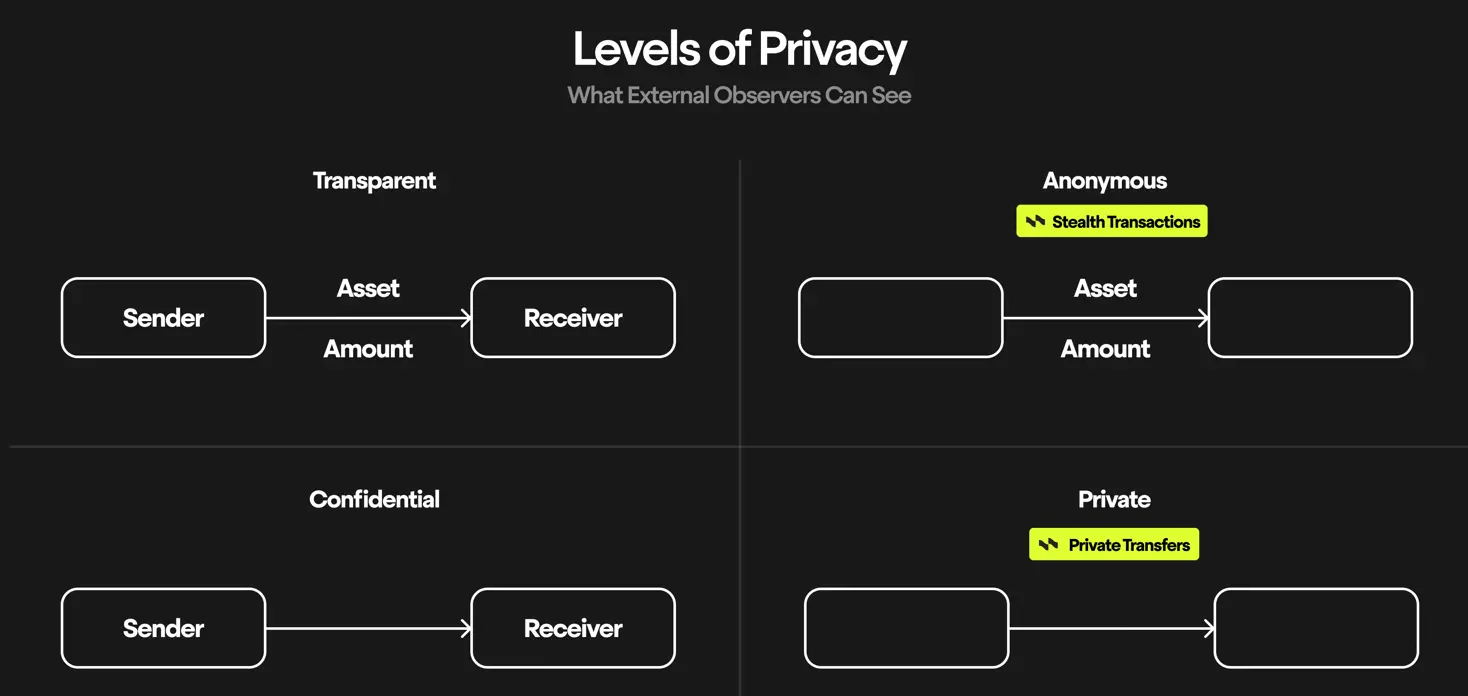

Privacy Levels

- Private Transfers (Complete Privacy)

Executed within the privacy layer, hiding the sender, receiver, amount, and assets, with high throughput and no additional EVM overhead. - Stealth Transactions (Semi-Privacy)

Executed at the EVM layer, but the funds originate from the privacy layer, making it impossible to trace the true identity. - Native ZK

Depends on the specific application scenario.

Encrypted Lineage

Payy uses a nullifier mechanism to prevent transaction paths from being traced, ensuring that funds do not expose their source when flowing between the privacy layer and the EVM layer.

In special circumstances (such as preventing malicious fund flows), the encrypted lineage can be decrypted through on-chain governance proposals, balancing privacy and compliance.

Private Transfer Mechanism

In Payy, private transfers can be implemented in two ways:

- Directly calling PrivacyBridge: authorizing fund transfers through ZK proofs.

- Using the "transparent upgrade" method of Privacy Vault (no need to change wallets).

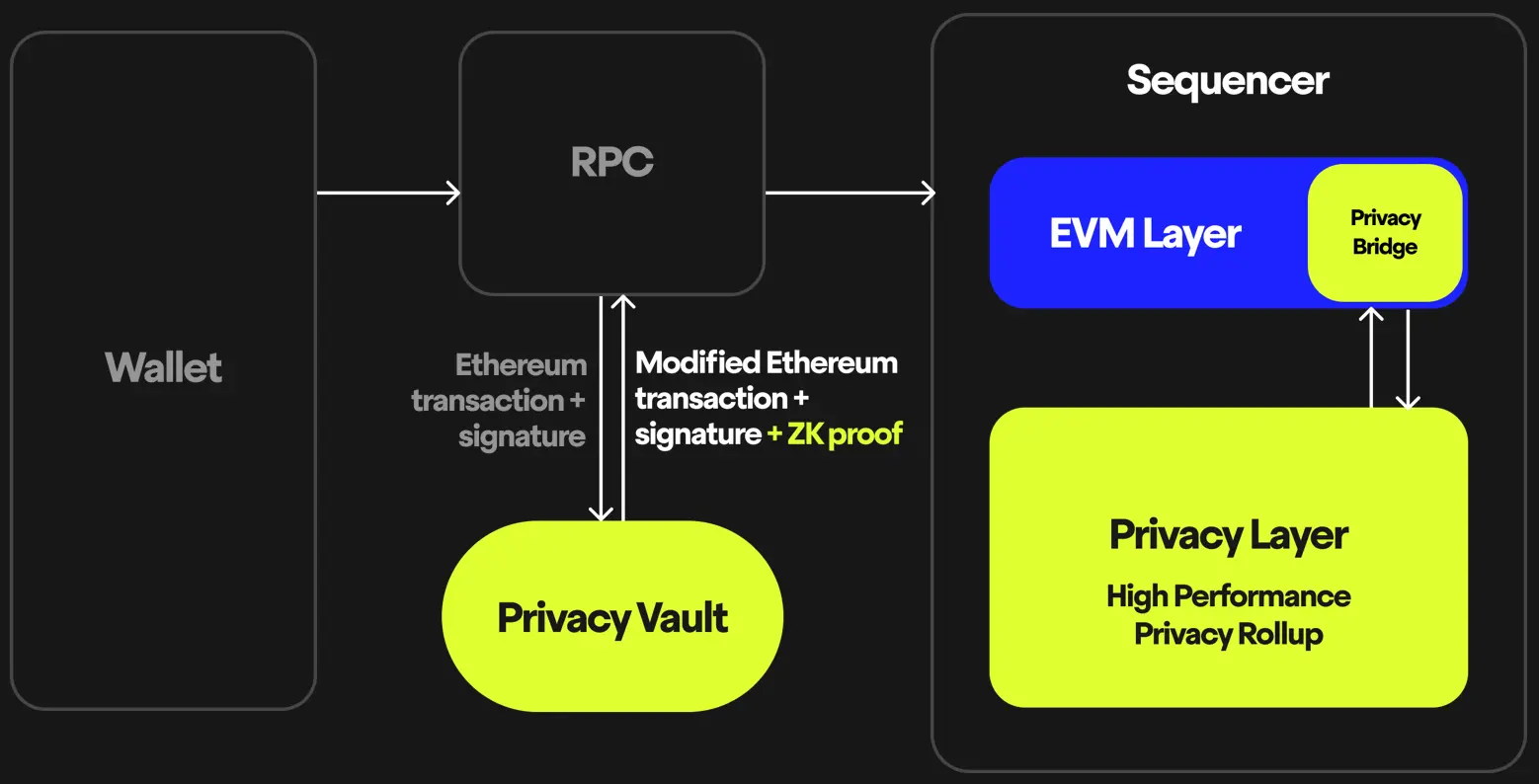

Transparent Upgrade (Core Mechanism)

Payy supports "seamless privacy upgrades" for existing wallets:

- Users still use standard ERC-20 transfers (transfer(address, uint256)) or native transfers.

- Transactions are sent normally through eth_submitRawTransaction().

- No need to modify wallets or operational habits.

When the system detects a transfer transaction (such as function selector 0xa9059cbb):

- RPC automatically calls Privacy Vault to request ZK proofs.

- Privacy Vault verifies the signature and generates a private transaction proof.

- Finally, the transaction is submitted to PrivacyBridge to complete the private transfer.

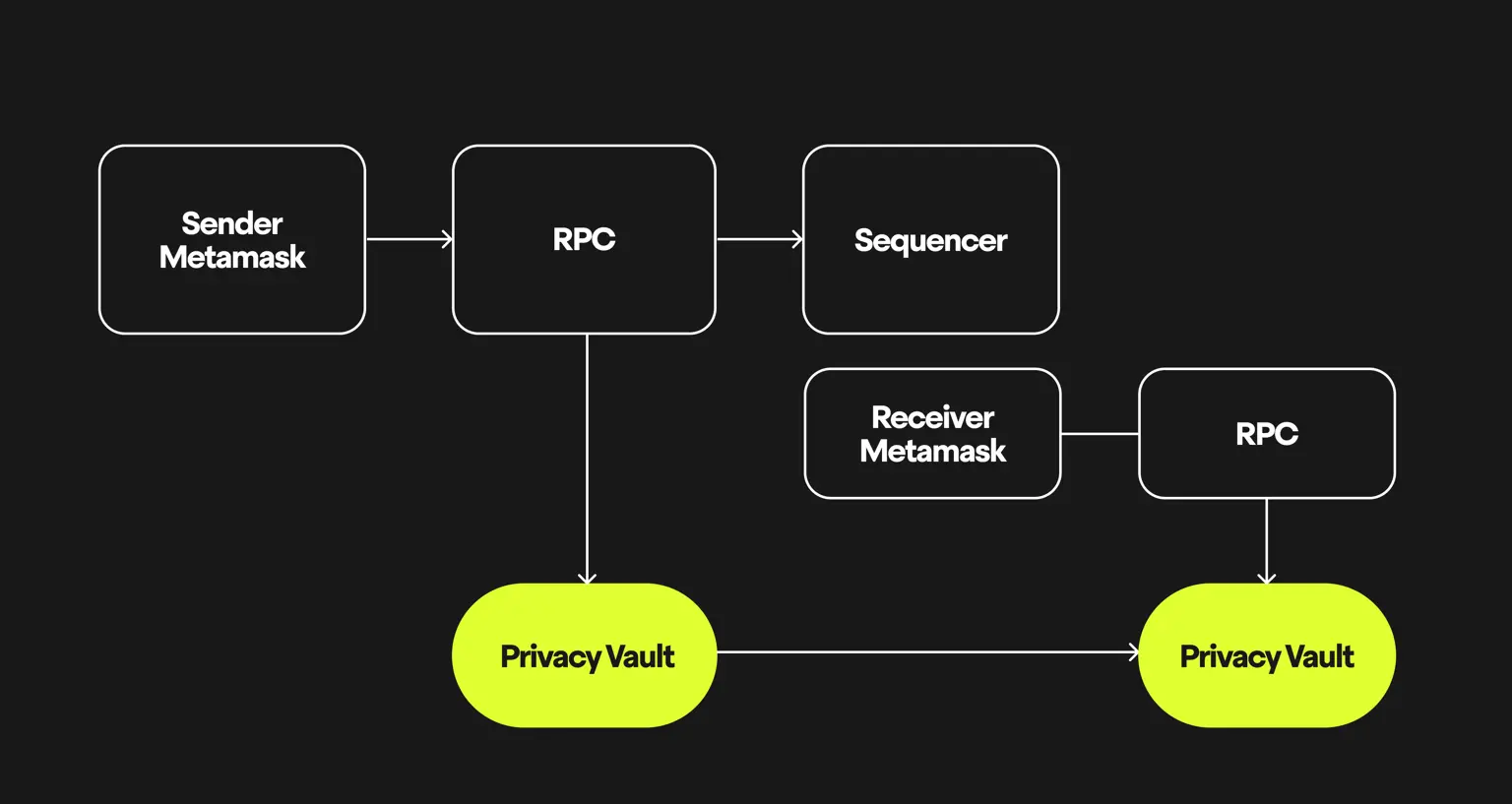

Receiving Mechanism

Since transaction data is encrypted:

- The receiver needs to obtain the corresponding Note (credential data) to withdraw funds.

- Privacy Vault determines the receiving address through the Privacy Vault Registry.

- The receiver's Privacy Vault will return a signed confirmation, completing the fund reception.

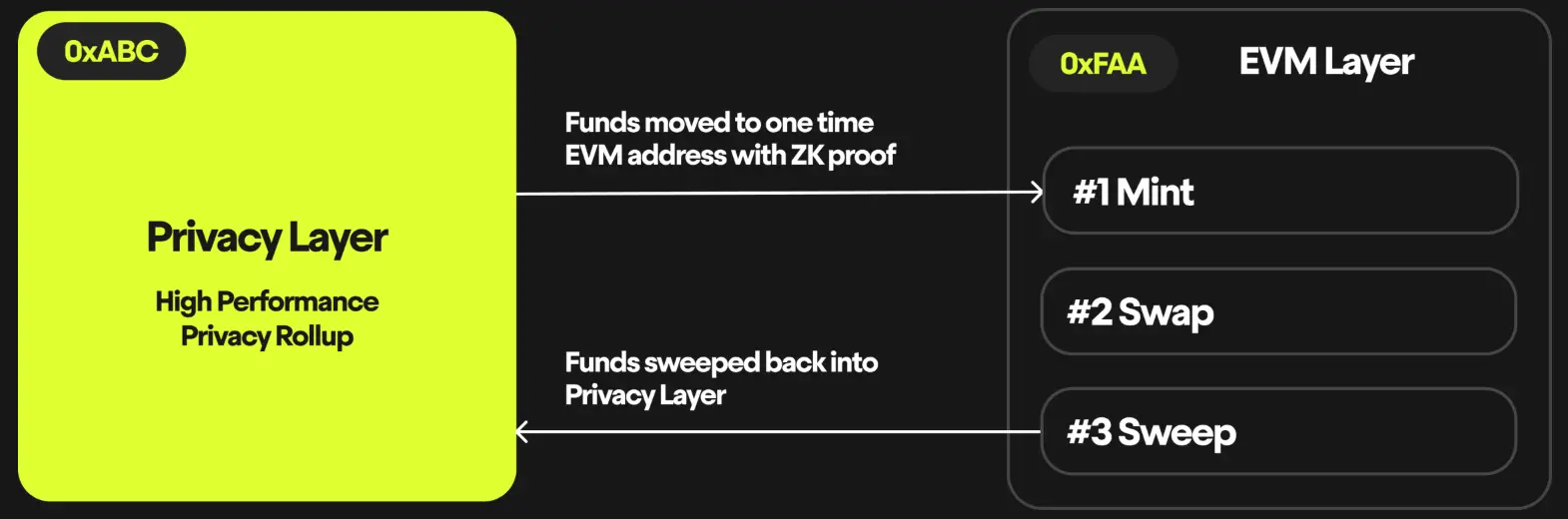

Stealth Transactions

Payy achieves privacy transaction capabilities by introducing a one-time address mechanism at the EVM layer. The core lies in the seamless transfer of funds between the privacy layer and the EVM layer, generating a brand-new temporary address for each transaction.

For example, when a user makes a private exchange from PUSD to PAYY:

- Funds are first withdrawn from the privacy layer to a newly generated one-time address.

- The exchange operation is completed at the EVM layer.

- The exchanged PAYY tokens return to the liquidity pool of the privacy layer.

Since each transaction uses a different one-time address, external observers cannot associate the flow of funds, thus achieving transaction privacy protection.

Native ZK

Payy natively supports zero-knowledge proofs (ZK), enabling developers to build privacy applications directly on its network while balancing performance and cost efficiency.

On traditional blockchains, the verification cost of ZK proofs is extremely high, potentially consuming over 5 million gas (about 10% of block space), making it difficult for most privacy applications to verify transactions one by one, relying instead on Rollup solutions.

In Payy:

- Native ZK verification capabilities are provided, significantly reducing costs.

- Developers can directly call ZK proofs in EVM smart contracts.

- Achieves trustless validation of off-chain transactions.

Tron Commentary

Payy's core advantage lies in its construction of a privacy stablecoin payment system based on zero-knowledge technology, achieving default private transactions through "privacy layer + stealth addresses + native ZK verification," while being compatible with EVM and supporting seamless upgrades for existing wallets, significantly lowering the user entry barrier. Coupled with self-custody wallets and Visa cards, it closes the loop between "on-chain privacy assets and real-world payments," and enhances performance and reduces costs through the L2 Rollup architecture.

Its potential disadvantage is a strong reliance on ZK infrastructure and privacy liquidity, high system complexity, and higher thresholds for development and auditing. Additionally, privacy features may face compliance uncertainties in different regulatory environments. Overall, Payy is a cutting-edge stablecoin infrastructure that balances privacy, payments, and scalability, but it is still in the early stages of technical and ecological development.

2. Detailed Explanation of Key Projects for the Week

2.1. Detailed Analysis of Midas, which raised a total of $63.75 million, led by RRE Ventures and CREANDUM, with participation from Coinbase, GSR, OASIS, and Framework—connecting off-chain government bond yields with on-chain liquidity

Introduction

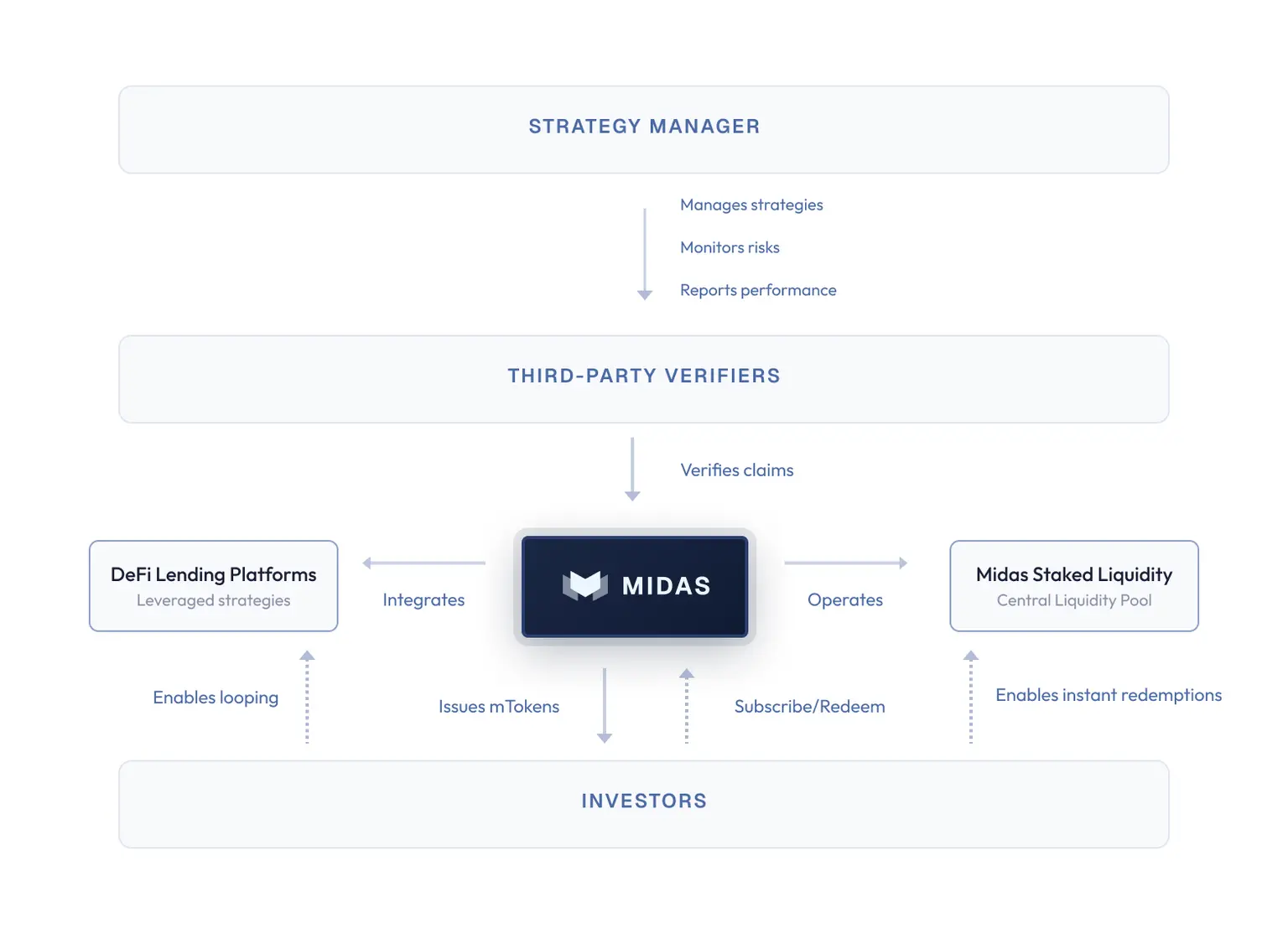

Midas is a platform for composable on-chain investment products. It allows strategy managers to tokenize institutional-level investment strategies, enabling investors to gain complete transparency, instant redemption capabilities, and native composability within the DeFi ecosystem.

Midas is positioned at the core of the on-chain financial market, connecting institutional-level strategy managers, DeFi protocols, and investors through the provision of on-chain investment products, building a unified financial ecosystem.

Core System Architecture Analysis

- Open Liquidity Architecture

Midas provides investors with high liquidity, composable on-chain investment products through its Open Liquidity Architecture, addressing the efficiency issues between continuous on-chain settlement and traditional financial settlement delays, achieving instant access and efficient capital utilization.

Core Mechanisms

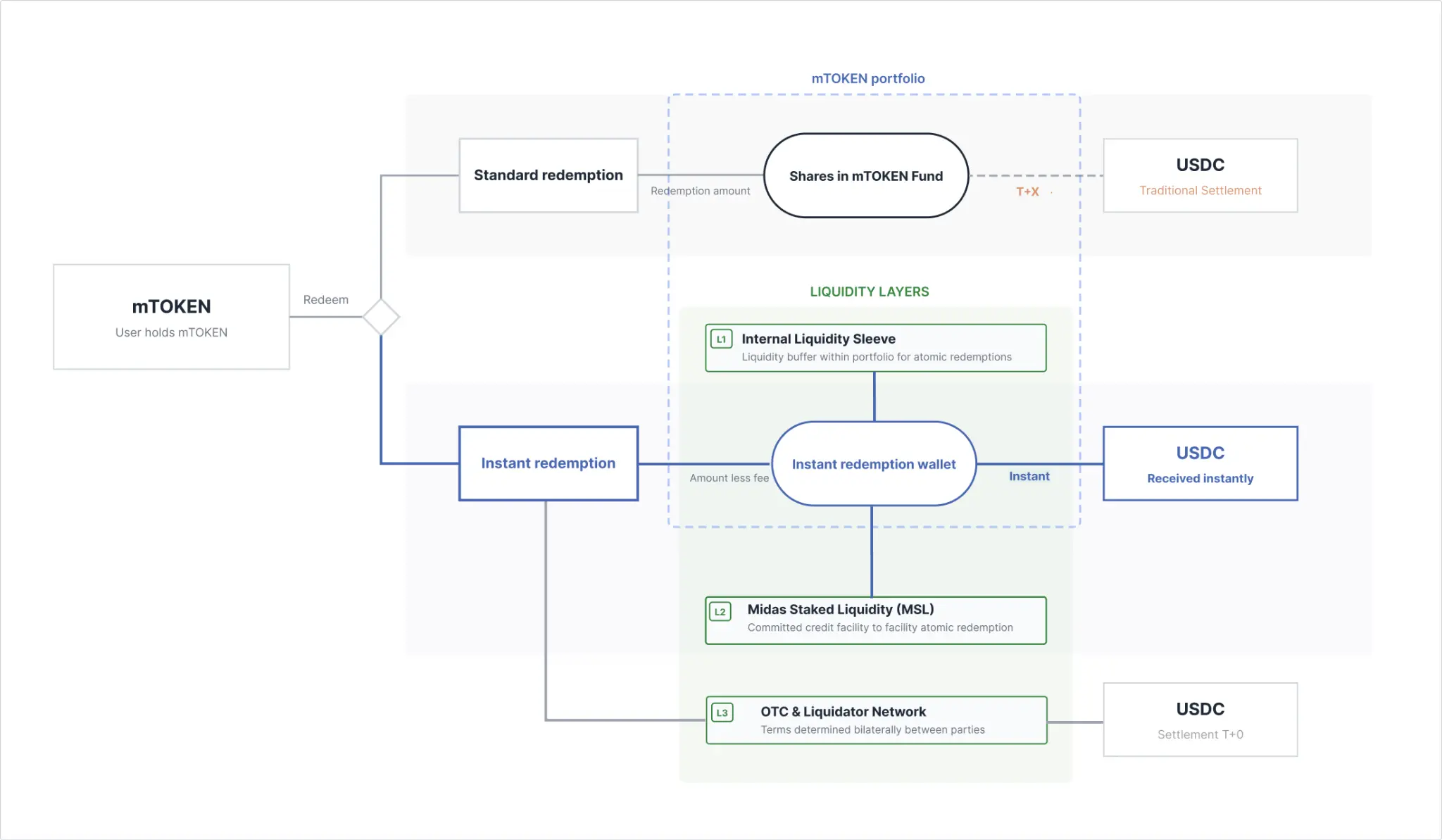

This architecture introduces flexible redemption methods to compensate for liquidity and settlement lag issues in traditional finance:

- Standard Redemption

- No fees

- Executed according to the natural settlement cycle of the underlying assets (which may take days or weeks)

- Calculated based on the NAV (Net Asset Value) at the final settlement.

- Instant Redemption

- Provides on-demand liquidity without waiting.

- Immediately exchanged for stablecoins (such as USDC).

- Relies on dedicated liquidity pools.

- Charges a fixed fee.

- Smart contracts execute automatically:

- Reads the current NAV.

- Destroys mToken.

- Immediately returns stablecoins.

- Midas Staked Liquidity (MSL)

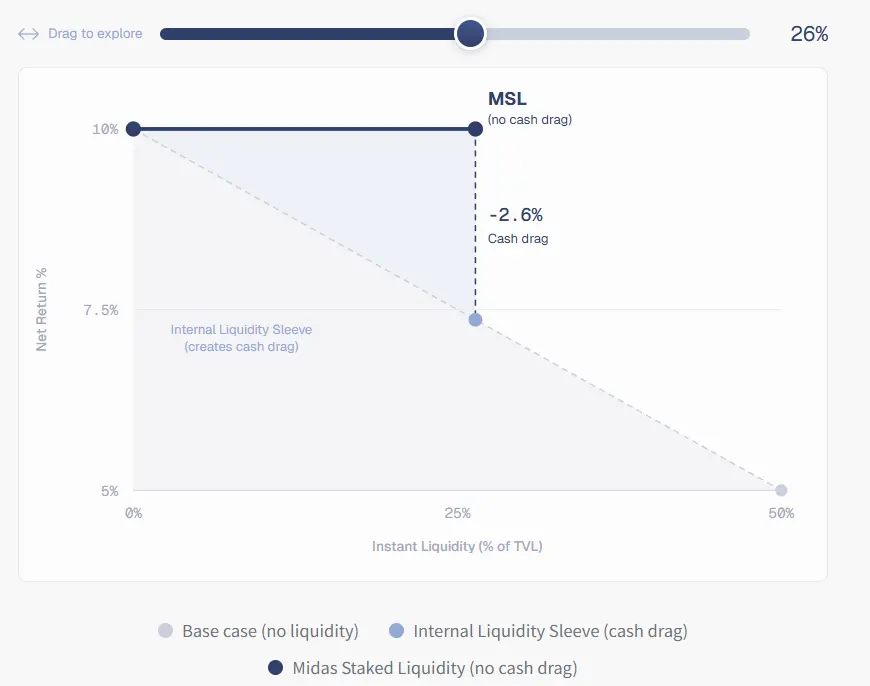

Midas Staked Liquidity (MSL) is a set of on-chain liquidity infrastructure designed to achieve instant redemption (atomic settlement), aiming to solve the "cash drag" problem in traditional portfolios—holding idle cash to respond to redemptions, thereby lowering overall returns.

When a user initiates an instant redemption, the MSL pool provides USDC to the user (after deducting a fixed redemption fee) while destroying the corresponding mToken; subsequently, the asset manager repays MSL through smart contracts after settling off-chain assets, forming an on-chain auditable short-term liquidity lending relationship.

For liquidity providers (LPs), MSL offers a risk-isolated income opportunity: without bearing the risks of underlying assets, they earn redemption fee income by providing short-term liquidity, and their funds have priority repayment rights in the structure. Overall, MSL is essentially a "high-frequency liquidity supply layer with no market risk," serving the time difference between on-chain assets and real asset settlements.

- Transparency Mechanism

The core of Midas's transparency system is:

Upgrading the "disclosure" of traditional asset management to "on-chain verifiable real-time transparency."

Core Mechanisms

On-chain Attestation Engine

- Maps off-chain asset data (such as government bonds, funds) to on-chain states through the Midas Attestation Engine.

- Regularly generates on-chain "checkpoints."

- Used to verify:

- NAV (Net Asset Value)

- Scale of collateral assets

- Reserve status

Third-party Validation

- Introduces third-party institutions (such as oracle/risk control agencies) for independent verification.

- Reduces single-point trust risks.

- Enhances data credibility and institutional acceptability.

Full-Link Data Transparency

Disclosure dimensions include:

- Composition of underlying assets (such as T-Bills, MMFs, etc.)

- Position structure and distribution

- Changes in net value

- Fund flows

Essentially:

From "black box asset pool" → "visualized, traceable asset structure."

High-Frequency Updates and Historical Tracking

- Data is continuously updated on a cycle (close to real-time).

- Provides historical records and time series.

- Supports auditing and backtracking.

Key Limitations

- Disclosure ≠ legal ownership.

- Users do not directly hold underlying assets.

- Essentially still a structured financial product.

- Investment Risk Management

Midas's risk management core lies in:

Achieving a "traditional asset management-like" risk control framework through asset selection, structural isolation, and operational constraints.

Core Mechanisms

High-Quality Asset Screening (RWA Priority)

- Primarily allocates low-risk assets:

- Short-term government bonds (T-Bills)

- Money market funds (MMFs)

- Emphasizes stable returns rather than high-volatility returns.

Essentially:

Returns come from "assets with extremely low credit risk."

Asset Isolation

- Each mToken corresponds to an independent asset pool.

- Risks do not transmit between different products.

Avoids:

- Systemic risk diffusion.

- Single asset collapse affecting the whole.

Liquidity Management (Core Focus)

- Solves redemption issues through MSL (liquidity layer).

- Avoids traditional "cash drag."

- Ensures instant redemption capability.

Achieves:

High yield + high liquidity balance.

Counterparty and Operational Risk Control

- Uses compliant custodial institutions.

- Introduces professional fund managers.

- Limits strategy scope.

Essentially:

Reduces human operation and credit risks.

Interest Rate and Market Risk Management

- Primarily exposed to:

- Interest rate fluctuations.

- Macro market changes.

- Reduces volatility through short-duration assets.

Technical and Structural Risks

- Smart contract risks.

- Oracle risks.

- On-chain/off-chain synchronization risks.

Through:

- Auditing.

- Multi-party validation.

- Modular design

Reduces risks.

Key Risk Points (Implied)

- Still relies on off-chain assets and custodial institutions.

- Not fully decentralized.

- Liquidity pressure may still arise under extreme market conditions.

Tron Commentary

Midas's core advantage lies in its combination of traditional institutional-level asset management (such as government bonds, MMFs) with on-chain transparency mechanisms, achieving near real-time asset visualization and auditability through on-chain proofs, multi-party validation, and high-frequency disclosures. At the same time, it leverages the MSL liquidity layer to solve redemption and "cash drag" issues, enhancing yield efficiency while ensuring liquidity; its risk control system is also relatively robust, emphasizing low-risk asset allocation and asset isolation.

However, its potential disadvantage lies in its reliance on off-chain assets and custodial institutions, fundamentally remaining a structured product rather than fully decentralized, with users not directly holding legal rights to the underlying assets. Additionally, factors such as oracles, settlement cycles, and extreme market liquidity pressures may still pose systemic risks under special circumstances.

III. Industry Data Analysis

1. Overall Market Performance

1.1. Spot BTC vs ETH Price Trends

BTC

ETH

2. Summary of Hot Sectors

- ZK / Privacy Computing

- Multiple projects are advancing ZK recursive proofs and cross-chain verification capabilities, focusing on enhancing multi-chain asset aggregation and low-cost verification (in conjunction with EIP-1108 / 4844).

- Privacy Identity (DID + ZK) is beginning to expand from single-chain to unified multi-chain data verification, evolving towards a "on-chain identity layer."

- RWA (Real World Assets)

- RWA protocols are starting to strengthen the on-chain compliance execution layer (rule engine + custody + order book).

- The technical focus is shifting from "asset on-chain" to settlement, liquidity, and DeFi composability.

- AI + Crypto

- AI Agents are gradually transitioning from tools to on-chain execution entities.

- Infrastructure combinations of "AI services + on-chain payment/account systems" are emerging (such as LLM Service-type architectures).

- Technical directions are concentrated on: automated trading, on-chain calls, and payment loops.

- DeFi / Derivatives

- DEXs are continuously evolving into multi-functional platforms (trading + lending + prediction markets).

- Derivatives protocols are strengthening on-chain matching and risk engine modularization.

- Infrastructure (Multi-VM / Execution Layer)

- "Blended Execution (Unified Execution across Multiple VMs)" is becoming a new trend (EVM + WASM + SVM).

- Technical focuses include: unified state, cross-language contract interaction, and zk proof optimization.

IV. Macroeconomic Data Review and Key Data Release Nodes for Next Week

Last week, the macroeconomic landscape overall presented a pattern of "repeated inflation expectations + high interest rate maintenance expectations":

- In the U.S., employment and consumption-related data remained resilient overall, with no significant cooling signals, causing market expectations for short-term interest rate cuts to continue to be postponed.

- U.S. Treasury yields maintained high-level fluctuations, with the 10Y yield fluctuating but not effectively declining, exerting pressure on risk assets.

- Gold experienced a phase correction, indicating a marginal retreat in market risk aversion.

- The U.S. dollar index operated overall strongly, with funds still leaning towards dollar assets.

Next week, three types of data will be key to watch (directly affecting market direction):

- U.S. Inflation Data (CPI / PPI)

- Impact: Determines the market's judgment on the Federal Reserve's policy path.

- Key Points:

- If inflation exceeds expectations → rates maintained longer → bearish for risk assets.

- If there is a significant decline → interest rate cut expectations rise → bullish for the market.

- Retail Sales

- Impact: Reflects whether consumption is starting to weaken.

- Key Points:

- Strong → strong economic resilience → delayed rate cuts.

- Weak → economic cooling → bullish for liquidity expectations.

- Initial Jobless Claims / Marginal Employment Data

- Impact: Observes whether employment is starting to weaken.

- Key Points:

- If it continues to rise → supports interest rate cut expectations.

- If it remains low → rates continue to stay high.

V. Regulatory Policies

United States

May 5: U.S. stablecoin regulation enters the implementation detail phase.

Discussions around the regulatory details of the GENIUS Act continue to advance, with institutions like BlackRock submitting opinions to the OCC, focusing on the scope of stablecoin reserve assets, custody requirements, and the compliant use of tokenized government bond assets. Market focus has shifted from "whether to regulate" to "how to implement."

May 6: CFTC continues discussions on the responsibility boundaries of non-custodial wallets.

U.S. regulators continue to discuss the division of responsibilities between non-custodial wallets and neutral software developers, focusing on clarifying which behaviors fall under "financial intermediaries" and which merely belong to technical interface provision. This direction significantly impacts the DeFi and on-chain wallet ecosystem.

European Union / Italy

May 6: The EU continues to advance preparations for the comprehensive implementation of MiCA.

EU regulatory bodies and member states continue to coordinate around the final implementation of MiCA, focusing on stablecoin reserves, information disclosure, CASP (Crypto Asset Service Provider) licenses, and operational resilience requirements.

May 7: The Bank of Italy promotes discussions on "tokenized SEPA."

The Bank of Italy publicly calls for an assessment of extending the SEPA payment system to tokenized financial scenarios, hoping that the EU payment system can adapt to on-chain settlements and digital asset circulation.

Hong Kong

May 8: Hong Kong's stablecoin regulatory framework enters a substantive advancement phase.

After the passage of the Hong Kong Stablecoin Bill, the HKMA continues to advance subsequent licensing and implementation rules, emphasizing AML, reserve transparency, and issuer governance requirements. Hong Kong is further strengthening its positioning as "Asia's compliant crypto center."

South Korea

May 8: South Korea continues discussions on the issuance entities of the Korean won stablecoin.

The Bank of Korea (BOK) and financial regulatory agencies (FSC) continue to have differences over whether to "allow only banks to issue stablecoins" or "allow tech companies to participate." This topic has become one of the key focuses of South Korea's crypto policy.

Japan

May 9: Japan continues to advance the implementation of FIEA crypto asset reforms.

Japanese regulators continue to promote the reform of crypto asset financial products, including exchange responsibility reserve requirements, stablecoin rules, and tax adjustments, reinforcing the institutionalized and compliant structure of the digital asset market in Japan.

United Arab Emirates (UAE)

May 10: Abu Dhabi's stablecoin plan continues to advance.

Abu Dhabi sovereign fund ADQ, First Abu Dhabi Bank, and other institutions are promoting the dirham stablecoin project, with the UAE continuing to strengthen its layout in the Middle East's digital asset and payment settlement fields.

Singapore

May 10: MAS continues to strengthen stablecoin and payment license regulation.

The Monetary Authority of Singapore (MAS) continues to advance the stablecoin and payment service license framework, focusing on reserve assets, fund segregation, and consumer protection, maintaining an "open but high compliance threshold" regulatory path.

Risk warning

Risk warning

Popular articles