SignalPlus Volatility Column (20240909): Another Macro Week

Last Friday's worse-than-expected non-farm payroll data and a downward revision of previous values once again raised concerns about an economic recession, leading to the worst weekly performance of U.S. stocks since March 2023. The negative risk sentiment also dragged down the performance of digital currencies, reaffirming the curse from seasonal statistical data. Meanwhile, U.S. Treasury bonds showed a steepening trend, and the 2/10 spread finally ended its inversion.

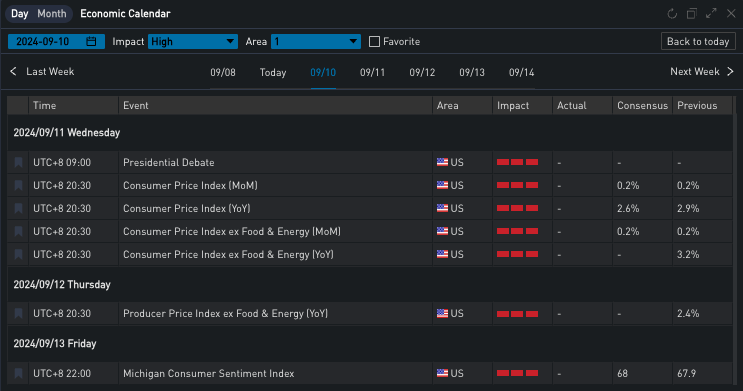

Source: SignalPlus, Economic Calendar

Source: SignalPlus, Economic Calendar

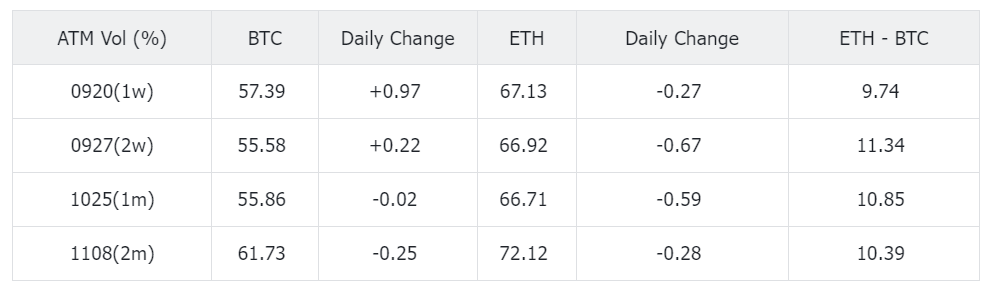

This week, the crypto community's focus remains on macro events. After a calm weekend, options market makers have quietly raised the front-end implied volatility (IV). Although the term structure of BTC and ETH is quite similar, there are slight differences in the details. First, it is noted that the peak for BTC is on September 11, while for ETH it is on September 12, with both expiration dates pricing in very high volatility premiums.

The uncertainty for September 12 mainly comes from the CPI data. Although the impact of inflation data has receded behind employment data, it has once again become the top priority for financial traders this week and may become a decisive factor in determining whether the Federal Reserve will significantly cut interest rates by 50 basis points at the FOMC meeting in late September.

For traders buying on September 11, their main focus is still on the presidential campaign speech scheduled for 9 AM Beijing time. This confrontation is the first, and perhaps the only, opportunity for Trump and Harris to face off directly, with less than two months until the official election day, forcing them to seize every opportunity to persuade voters. The topic of digital currencies is bound to arise in the dialogue between the two sides, and the market has assigned a higher correlation to BTC, which is also reflected in the term structure.

Source: SignalPlus

Source: SignalPlus  Source: SignalPlus

Source: SignalPlus

The mid-section of the term structure has formed a trough with October 25 as the lowest point, with uncertainty allocated to the days before the FOMC meeting and the presidential election. The two currencies show slight differences in the structure of forward IV, and the low point for ETH from September 12 to September 13 has a chance to be adjusted. The flat slope of ETH at the end of the month and the volatility premium that is 10% higher than BTC may also attract cross-currency volatility trading.

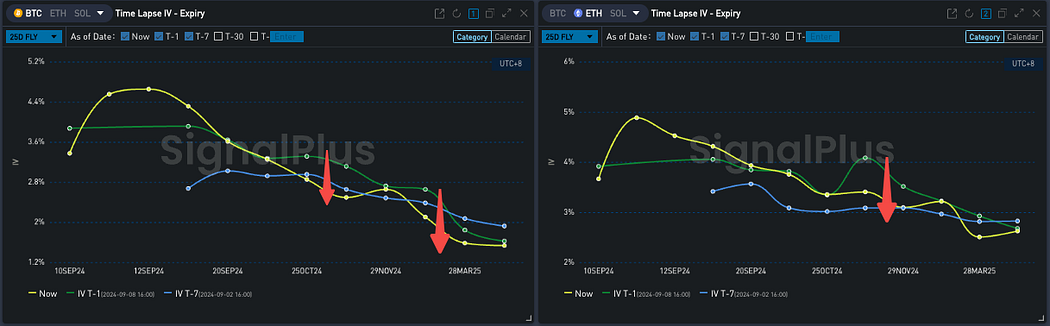

From the curvature of the volatility smile, the far-end fly has experienced a brief rise before retracing back to levels close to a week ago.

Source: Deribit (as of September 9, 16:00 UTC+8)

Source: Deribit (as of September 9, 16:00 UTC+8)  Source: SignalPlus

Source: SignalPlus

Risk warning Risk warning

Risk warning Risk warning